Superannuation in Australia: planning for change, sustainability and resilience

On 1 January 2020, superannuation trustees will become subject to the requirements of APRA’s new prudential standard SPS 515 Strategic Planning and Member Outcomes. This new standard requires trustees to undertake a Business Performance Review (BPR), which includes results of the new legislative outcomes assessment.

The outcomes assessment and the BPR required by SPS 515 are intended to complement each other; where the outcomes assessment provides a point-in-time picture, the BPR is intentionally more forward-looking. Trustees are expected to assess whether they will continue to deliver quality, value-for-money member outcomes into the future. In other words, the BPR is about sustainability.

Along with fees and costs and investment performance, sustainability is one of the three areas assessed in the MySuper heatmap that APRA has recently released.

Although providing like-for-like comparisons of returns or fees between products is challenging, the concepts themselves are simple enough to grasp. The notion of sustainability is a less well defined concept, but it is a crucial consideration when assessing fund and product performance.

From APRA’s perspective, "sustainability” is not a direct measure of current performance or outcomes; instead it is an indicator of a trustee’s likely ability to continue delivering sound member outcomes into the future, and address areas requiring improvement. In an industry where retirement outcomes are delivered over decades, rather than months or years, funds must be able to deliver sound outcomes over the long-term if they are to truly safeguard their members’ best interests.

Sizing up sustainability

With respect to trustees’ ability to deliver member outcomes into the future and address any areas of concern, APRA’s MySuper heatmap harnesses two scale measures that provide the baseline for considering fund sustainability: the net assets available for members' benefits and the total number of member accounts.

The likely future direction of these scale measures is illustrated in the heatmap using three trend metrics:

- Adjusted Total Accounts Growth Rate

- Net Cash Flow Ratio

- Net Rollover Ratio

These metrics provide an indication of member retention, the amount that the fund is paying out to members for every dollar that is paid in, and the overall growth in assets. In other words, they indicate whether the fund is likely to grow or contract over coming years.

Scale is important in superannuation: to put it bluntly, size matters. While it is not a guarantee of good performance, nor an insurmountable barrier to it, larger funds are typically better able to, for example, negotiate scale discounts with service providers, access investment markets, and spread the cost of operations over their membership base. All of these are ultimately indicators of a fund’s ability to provide good outcomes for its members now and into the future.

APRA expects trustees to consider their heatmap outcomes for the three sustainability metrics, gain an understanding of factors that have driven those outcomes, and develop a plan to promptly address any sustainability concerns.

The bigger picture

Treasurer Josh Frydenberg recently referred to Australia’s ageing population as an “economic time bomb”1, with the budget expected to come under increasing pressure as a proportionally smaller workforce supports a growing number of retirees. Compared to 40 years ago, the typical Australian is not just older, but will be older for longer as well. In addition to the impact this change will have for the country’s tax base, it will also pose challenges to the superannuation industry.

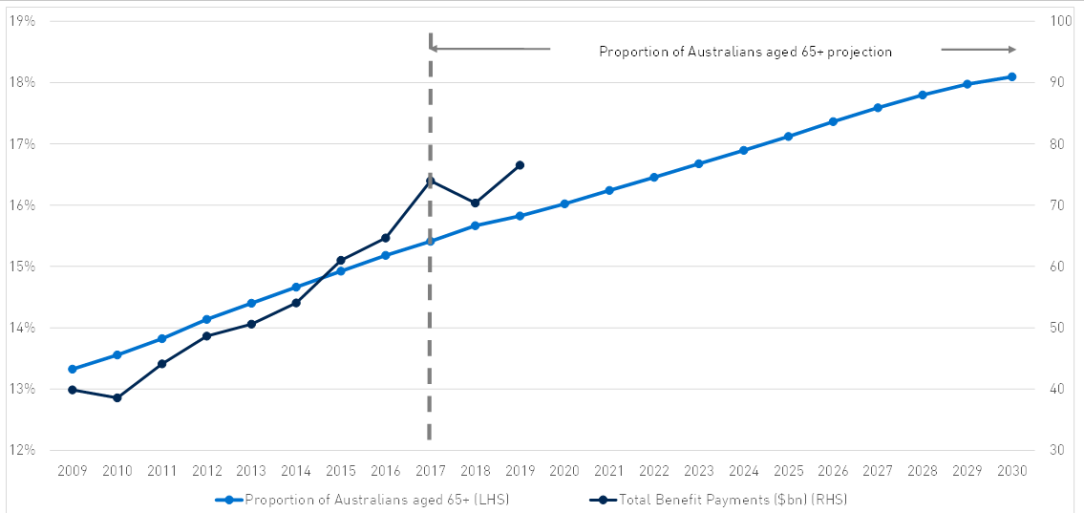

Already, an increasing proportion of Australians are transitioning from the accumulation phase to the retirement phase of super. The number of Australians aged 65 or older will rise by around a third to reach an estimated 18 per cent of the population by 2030 (see Chart 1). This will drive further increases in total superannuation benefit payments, which have nearly doubled over the past 10 years, and present headwinds for the scale and sustainability of superannuation funds. While this shift in member payments is the sign of a mature pension system, it presents a number of challenges for superannuation trustees, from managing a changing liquidity profile, to a shifting focus on attracting and retaining members in the pension phase with different types of products and services. For funds which do not attract new members and retain existing members, these challenges will be compounded.

Chart 1: Proportion of Australians aged 65+ and Total Benefit Payments

With change of this scale on the horizon, sustainability measures aren’t just a “nice to have”, but an essential mechanism for gauging capacity within a fund to meet future challenges and deliver for members over the longer-term.

Member choice

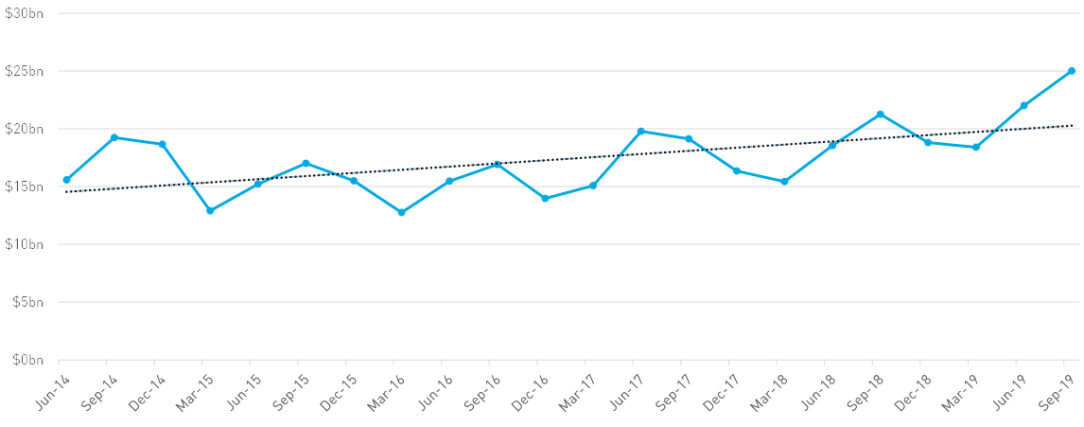

The introduction of superannuation choice legislation in 2005 for many employees introduced a new level of competition into the superannuation industry. Members could also choose to have their contributions paid into a self-managed superannuation fund. Over the past five years, the amount of superannuation monies rolled over by members choosing new funds or consolidating accounts has increased (see Chart 2), though this growth has not outstripped the asset growth of the industry. While superannuation members have traditionally been thought of as disengaged, the sharp jump in outward rollovers since the Royal Commission indicates that active members are prepared to vote with their feet and change providers where they feel it is in their best interests.

Chart 2: Superannuation outward rollovers (by quarter)

Multiple accounts

According to Australian Tax Office (ATO) data2 as at 30 June 2018, around six million Australians hold more than one account and therefore pay multiple fees and, potentially, multiple insurance premiums. This can have a significant impact on the retirement outcomes for these members.

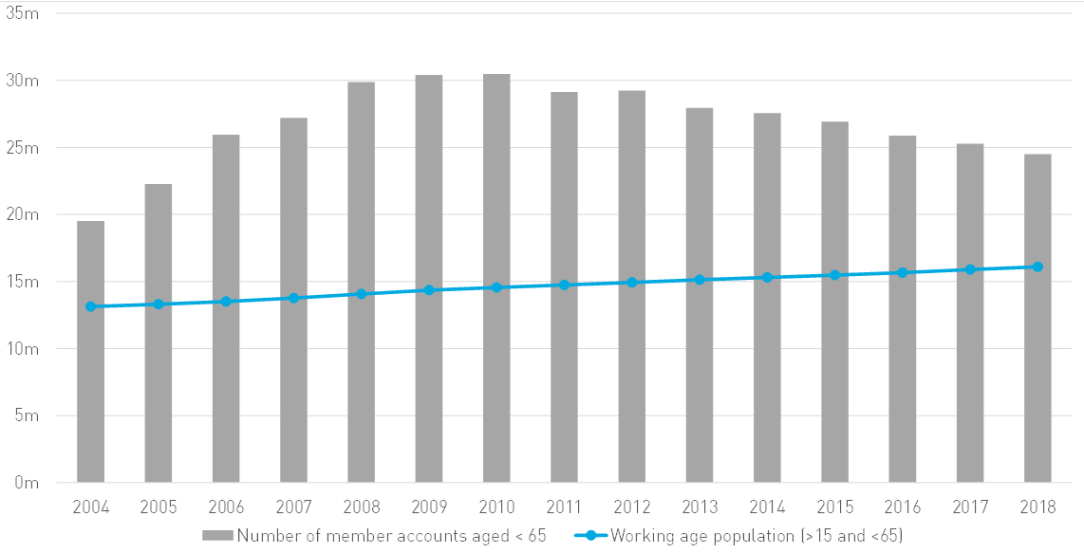

While some members deliberately have multiple accounts, for a large component this is unintentional. Members have become more aware of the additional costs of holding more than one superannuation account and the process to consolidate accounts has been simplified over time. This has led to some progress on consolidation at the member account level in recent years (see Chart 3).

The percentage of individuals covered by superannuation with more than one account has decreased over time from 43 per cent in 2015 to 36 per cent in 2018 (see Table 1). The number of member accounts for individuals under 65 has decreased over the past decade from a peak of 30.5 million in 2010 to 24.5 million in 2018 even as the working age population has increased (see Chart 3).

Recent reforms3 should drive a continuation of these trends, while other recent reforms4 have been implemented to address the proliferation of multiple accounts by requiring inactive low balance accounts to be swept out of funds to the ATO.5

Table 1: Individual Members by number of accounts held

Number of Accounts Held | Percentage of Individuals |

| 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|

1 account | 57 | 60 | 61 | 64 |

2 accounts | 25 | 25 | 24 | 23 |

3 accounts | 10 | 9 | 10 | 8 |

4 or more accounts | 8 | 6 | 5 | 5 |

More than one account | 43 | 40 | 39 | 36 |

Source: ATO based on member data reported by funds to the ATO for the year ending 30 June 2018. Percentages have been rounded.

Chart 3: Number of Member Accounts and Working Age Population

For funds with a large number of inactive accounts, the sweep of accounts to the ATO is likely to substantially reduce their membership base, reducing the number of accounts that their operating costs can be spread across, and potentially leading to remaining members being faced with increased fees. In these circumstances, trustees need to challenge themselves to consider whether they can provide value for money services to their members in future.

Fund consolidation

As trustees continue to face increased expectations on what is needed to continue to operate a fund, a number of them have made the decision to seek a merger partner or otherwise exit the industry. This is evidenced in the consolidation in the number of APRA-regulated superannuation funds over the last decade, which has previously been highlighted by APRA Insight.

Fund consolidation, with fewer, larger funds remaining in the industry, has and will continue to provide an offset to some of the sustainability challenges outlined above, with the ability of small to medium funds to attract (or enter into arrangements with) merger partners a strategic consideration.

Keys to resilience

The sustainability of funds is affected as much by the combination of account consolidations and members’ choice of fund as the flows that result from an ageing membership base. Funds that provide a compelling product to members in terms of net investment returns, fees, and insurance arrangements are likely to be better able to retain and grow their membership base and weather these challenges.

APRA expects trustees to clearly articulate and measure their performance across a range of areas including, but not limited to, investment performance. Trustees should therefore take a holistic approach to sustainability by assessing the overall outcomes provided to members based on the products, options and services offered.

Funds that are losing members will face greater competitive challenges than those that continue to access scale and maintain healthy inflows. Trustees must actively address strategic challenges and where necessary define tipping points or exit strategies, rather than adopt a passive or business as usual posture.

While the Superannuation Guarantee and tax incentives have historically driven the increase in Australia’s retirement savings, a process of review, refinement and reform has played an equal part in the industry’s ongoing expansion. As APRA Deputy Chair Helen Rowell noted in October, many improvements in trustees’ ability to safeguard their members’ money have come about precisely because the industry has been challenged.

In this sense, the challenge of remaining sustainable represents an opportunity for trustees to improve their business practices and deliver better quality outcomes for their members. This is consistent with the industry’s evolution over the last 40 years, as set out in this timeline.

Footnotes

1 ‘Ageing population is 'economic time bomb': Frydenberg’ Australian Financial Review November 19, 2019 (accessed November 29 2019)

2 Super data: multiple accounts, lost and unclaimed super, ATO website (accessed 16 December 2019)

3Treasury Laws Amendment (Putting Members’ Interests First) Act 2019

4Treasury Laws Amendment (Protecting Your Superannuation Package) Act 2019

5 This is in addition to the inactive account sweep mechanism that was introduced in 1999 where a superannuation provider is unable to ensure unclaimed money is received by a person entitled to receive it. Superannuation (Unclaimed Money and Lost Members) Act 1999.

The Australian Prudential Regulation Authority (APRA) is the prudential regulator of the financial services industry. It oversees banks, mutuals, general insurance and reinsurance companies, life insurance, private health insurers, friendly societies, and most members of the superannuation industry. APRA currently supervises institutions holding around $9.8 trillion in assets for Australian depositors, policyholders and superannuation fund members.