The Australian Prudential Regulation Authority (APRA) is Australia’s financial safety regulator. APRA is an independent statutory authority that is accountable to the Australian Parliament.

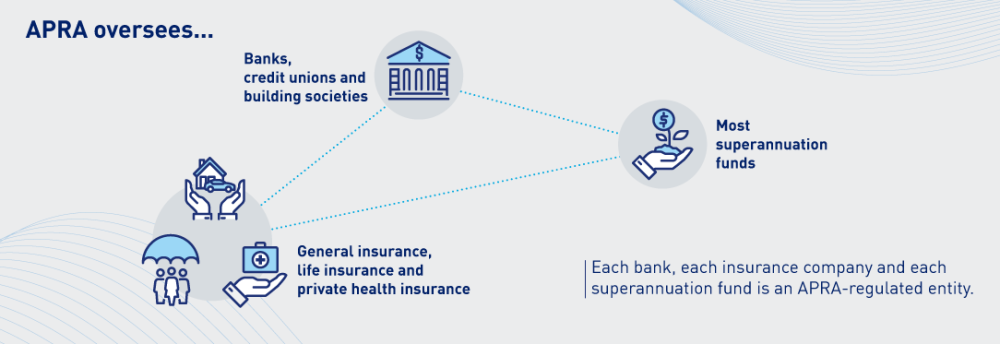

APRA oversees banks, credit unions, building societies, general insurance and reinsurance companies, life insurers, private health insurers, friendly societies, and a large part of the superannuation industry. Each of these financial institutions is an APRA-regulated entity.

APRA’s role is to protect the Australian community by establishing and enforcing legally binding standards that apply to APRA-regulated entities. In supervising these institutions, APRA seeks to ensure these entities carefully (or prudently) manage their businesses in order to protect the interests, in particular, of bank depositors, insurance policyholders and superannuation members.

APRA’s primary mandate is to ensure that APRA-regulated entities have sufficient financial means to meet their obligations to customers: that deposits are safe; that insurers have sufficient funds to pay claims; and that superannuation trustees are managing people’s money well. APRA does this by focusing – as much as possible – on preventing harm before it occurs, and by taking pre-emptive action when potential problems are identified.

While APRA’s overarching objective is to deliver a safe, stable and resilient financial system, APRA’s mandate is not to seek safety at all costs. Nor does APRA guarantee a zero failure rate for regulated entities, as that would put severe limitations on these entities’ ability to take risks, such as lending or investing money.

Instead, APRA balances its primary goal of safety with considerations of competition, efficiency, contestability (making barriers to entry high enough to protect consumers but not so high that they unnecessarily hinder competition) and competitive neutrality (ensuring that private and public sector businesses compete on a level playing field.) As such, APRA’s mandate is best described as stability-at-least-cost.

Given APRA’s end-goal is to protect depositors, policyholders and superannuation fund members as a group, and the stability of the financial system as a whole, APRA’s focus is generally not on individual consumers. Rather, APRA is a systems regulator: its key focus is to build and maintain the safety, stability and resilience of Australia’s financial system. APRA deals with systemic matters at an institutional level, rather than pursuing individual complaints about products and services.

APRA will typically only investigate individual complaints if they pose a threat to the safety and stability of an APRA-regulated financial institution. Other regulators, such as the Australian Securities and Investments Commission (ASIC) and the Australian Financial Complaints Authority (AFCA) have been established by the Australian Government as the primary regulators to deal with issues related to the treatment of individual consumers.

Wherever possible, APRA avoids overly prescriptive regulation, and doesn’t dictate a financial institution’s business model, products or business lines. Instead, APRA allows financial institutions to design their own structure, products and services, as long as they have the corresponding governance, risk management, internal controls and financial strength to mitigate the risks involved. In this way, APRA seeks to allow competitive and efficient outcomes for the Australian people, while also providing them with an appropriate level of protection.