Superannuation in Australia: a timeline

1980s | Superannuation at the start of this decade is far from widespread and isn’t transferable between different employers. As a result, until the mid-1980's superannuation was generally limited to public servants and white collar employees of large corporations. |

1987 | Superannuation assets are estimated to be $41.1bn, with 32 per cent of private sector employees covered. Following the 1986 National Wage Case guidelines, contributions start to be added to some industrial awards, which increases the coverage of private sector employees to 68 per cent by 1991. |

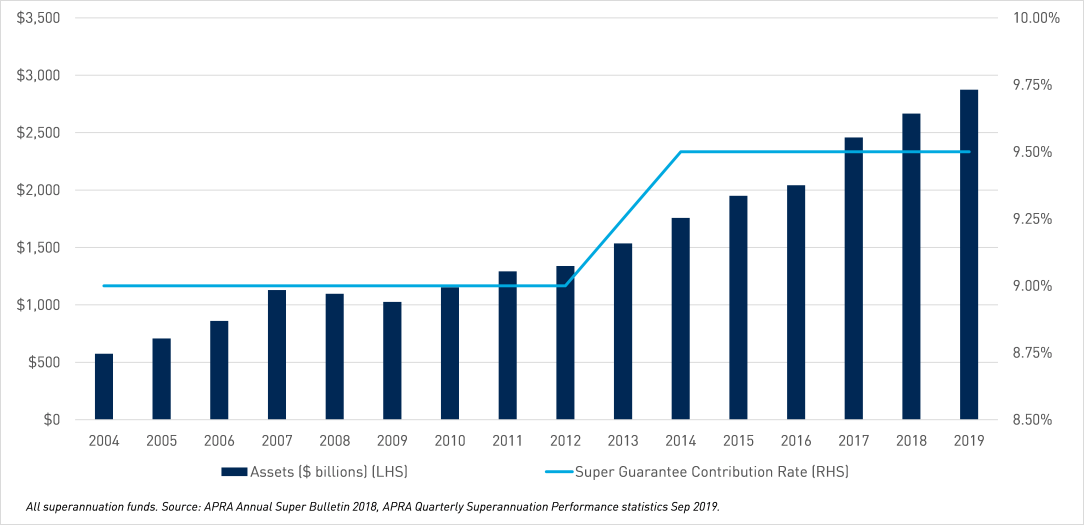

1992 | The Superannuation Guarantee (SG) is introduced with a mandatory 3 per cent contribution rate (or 4 per cent for employers with an annual payroll above $1 million), requiring employers to make a contribution into a super fund on their employees’ behalf. Superannuation assets at the time are estimated to be $148bn. This mandatory rate gradually increases to 9 per cent by 2002, and to the current rate of 9.5 per cent in 2014. |

1993 | The World Bank endorses Australia’s ‘three pillar’ system: compulsory superannuation, the age pension, and voluntary retirement savings, as world’s best practice for the provision of retirement income. |

1996 | Total superannuation assets are estimated to have reached $245.3bn. |

1998 | On the recommendation of the 1997 Wallis Financial System Inquiry, APRA is established as the prudential regulator of ‘authorised deposit-taking institutions’ (ADIs), insurers and superannuation licensees. APRA’s vision is to deliver a sound and resilient financial system, founded on excellence in prudential supervision. |

1999 | Also following the Wallis Inquiry, self-managed super funds (SMSFs) are established to allow small businesses and the self-employed to establish and manage their own superannuation accounts. |

2003 | Provisions come into force allowing the splitting of superannuation between divorcing or separating spouses, either by agreement or by court order. |

2005 | Employees become able to select their super fund for SG contributions. Transition to Retirement Pensions become available, which don’t require employment to be terminated before a pension commences, and allow recipients to continue working part-time. |

2007 | Superannuation assets are estimated to be above $1 trillion, which for the first time is greater than Australia’s gross domestic product (GDP). |

2007-2009 | The global financial crisis creates investment losses for Australian superannuation funds of more than $200 billion, with total superannuation assets only returning to the pre-GFC level in 2010.

|

2008 | Amendments begin to be introduced removing same-sex discrimination from Acts governing superannuation schemes, such as payment of death benefits. |

2011 | Following a review into the operation and efficiency of the superannuation system in Australia, the Stronger Super reforms are announced, including the MySuper product, which has the goal of creating an easily comparable default funds system. |

2013 | Also following these reforms, APRA’s prudential framework for superannuation is established and focuses on fund governance and risk management. A 2018 post-implementation review of this framework finds improved practices and processes in many areas across the superannuation industry, as well as opportunities for further enhancement. |

2014 | Australian workers who haven’t nominated a preferred superannuation fund begin receiving their SG contributions into a MySuper fund, as chosen by their employer. |

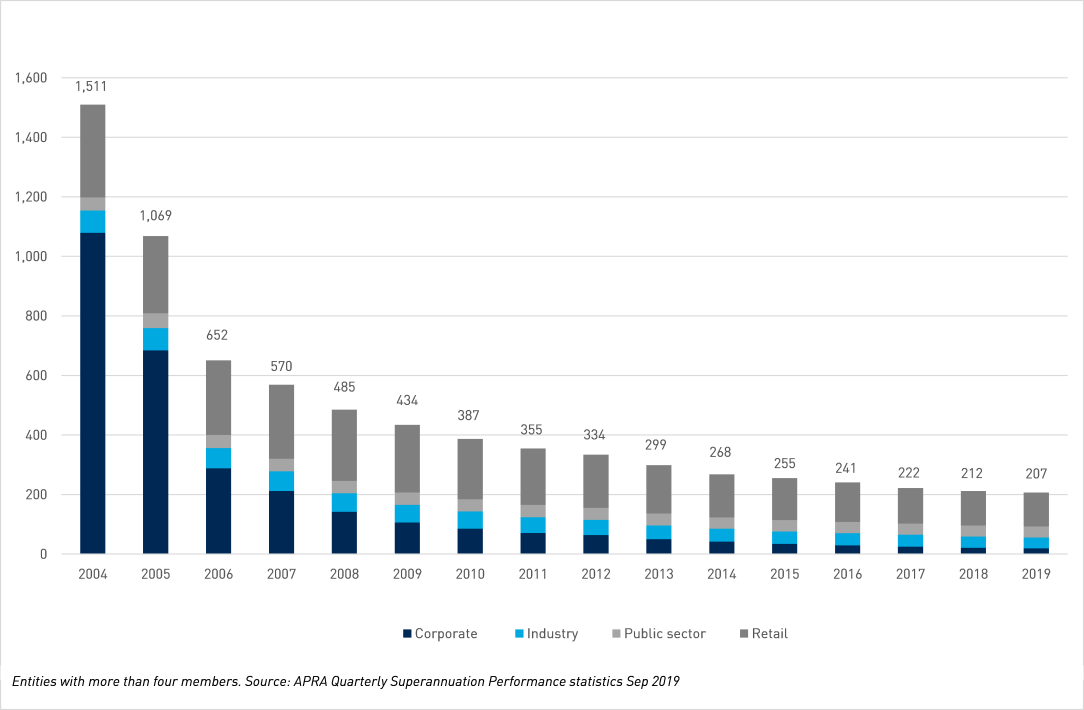

2015-2019 | By 2019, the number of superannuation entities decreases to 207 from 1,511 in 2004: a marked consolidation to less than one-seventh (or 14%) of the original number.

The Federal Government asks the Productivity Commission (PC) to undertake a review of the efficiency and competitiveness of the Australian superannuation system, and in late 2017 establishes the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. The final PC report, handed to the Government in December 2018 and publicly released in January 2019, recommends appointing an expert panel to select ten default super funds, based upon value-for-money and quality benchmarks. By 2019, the pooled value of funds under management has soared to $2.9 trillion, one of the largest in the world, and 1.5 times Australia’s GDP. Australia’s proportion of the population with superannuation reaches 78% – one of the highest levels of coverage in the world.

|

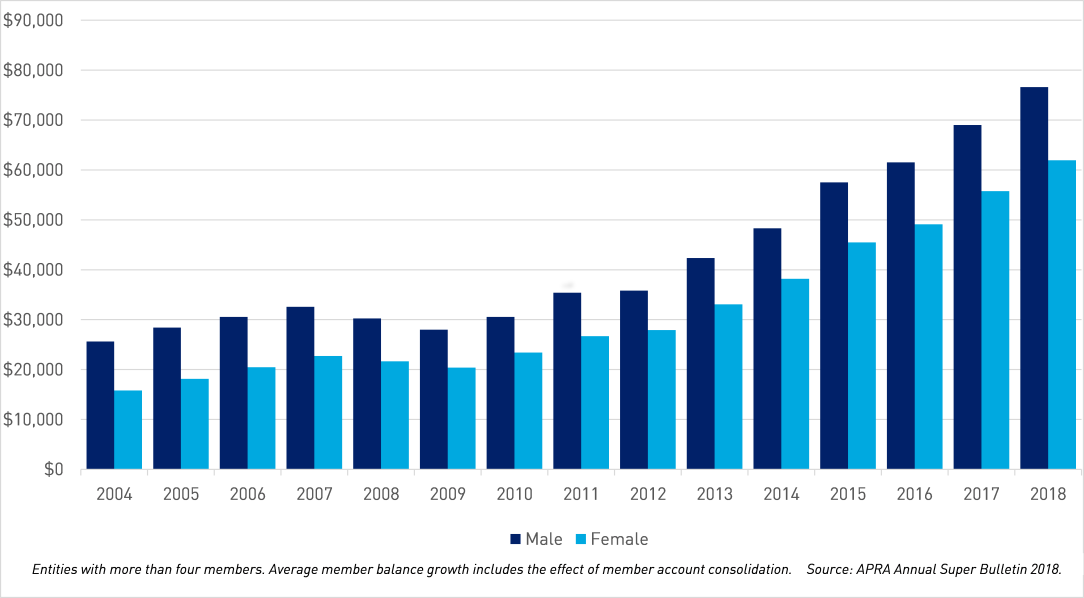

The future | While Australians have reason to feel proud of the success of Australia’s superannuation system in providing for retirement income, the need for review, refinement and reform continues. An example is the retirement savings of Australian women. The chart below indicates that average female account balances have grown over the past 14 years and caught up as a proportion of average male account balances (81% in 2018 compared to 62% in 2004). However a substantial gender gap remains with average female account balances around $15,000 below that of males.

Various stakeholders have proposed ways of addressing this, includingremoving the SG exemption from employees who earn less than $450 a month, or adding super contributions to parental leave pay. Following the PC’s recommendations at the end of last year, the Federal Government announced a retirement income review which will evaluate: how the retirement income system supports Australians in retirement; the role of each pillar in supporting Australians through retirement; distributional impacts across the population and over time; and the impact of current policy settings on public finances. The Government appointed review panel released a consultation paper on 22 November 20191. 1 Retirement Income Review - https://www.treasury.gov.au/review/retirement-income-review |