Introduction

APRA’s role as prudential regulator is to maintain the safety and soundness of financial institutions. Its purpose is to ensure Australians' financial interests are protected and that the financial system is stable, competitive and efficient.

APRA collects data under the Financial Sector (Collection of Data) Act 2001 to, among other purposes, assist it to perform its functions and exercise its powers, and to enable it to publish information given by financial sector entities.

Note

In this discussion paper, references to a ‘bank branch’ or ‘bank branches’ refer to a branch of any authorised deposit-taking institution (ADI), which includes banks, building societies, credit unions, and other ADIs.

The Points of Presence data collection and publication

APRA’s authorised deposit-taking institutions' (ADI) Points of Presence data collection and publication is a detailed listing of the physical banking service channels provided across Australia by ADIs.

The data collection was first published by APRA in 2002, reflecting data as at June 2001, after a Parliamentary Inquiry identified there was no uniform collection of data on the delivery of banking services in Australia. APRA’s role to publish consistent data on banking points of presence has increased transparency on this matter.

APRA’s Points of Presence data collection and publication is used to provide information on, and identify trends in, the number and location of bank branches and other physical banking services across Australia. As the number of bank branches continues to decline, APRA’s Points of Presence data collection and publication has become more widely used.

Declines in the number of bank branches

As availability and use of digital banking has increased, the number of bank branches has continued to decline. In the five years from June 2017 to June 2022, APRA’s Points of Presence data shows a 30 per cent decline in the number of bank branches in major cities, and a 29 per cent decline in the number of bank branches in regional and remote areas.

APRA is aware that bank branch closures can have a significant effect on consumers and businesses in regional and remote areas, where the nearest branch may be a significant distance away.

APRA is also aware that bank branch services are important to those who may find it difficult to access or use digital banking services, including some older Australians, those without internet access, and those who use cash to make payments.

APRA’s role to provide transparency

APRA collects and publishes points of presence data to provide transparency on trends in the number of physical banking service channels in Australia.

A decision to open or close a branch is ultimately a commercial decision for individual banks. The banks operating in Australia have a range of business models, including fully digital banks. APRA’s prudential regulation does not define the number of bank branches in Australia, nor impose particular business models on banks.

However, as digital banking technology advances and the availability of bank branch services declines, APRA wants to continue to improve transparency on this matter, and to ensure the Points of Presence data collection and publication remains useful and relevant.

Chapter 1 - Objectives and scope

1.1 Objectives

APRA has released this discussion paper as part of its review of the Points of Presence data collection and publication.

APRA’s review implements Recommendation 7 of the Regional Banking Taskforce (‘the Taskforce’), which recommended APRA review its Points of Presence collection to better capture indicators on how banking services are accessed (see Chapter 2 for details).

The previous review of the Points of Presence data collection and publication commenced in 2015, and was completed in 2016. Given the ongoing shift in the delivery of banking services to digital channels, it is timely that the Points of Presence data collection and publication should once again be reviewed.

APRA’s review of its Points of Presence data collection and publication aims to determine:

- who uses the Points of Presence data;

- what users expect and need from the Points of Presence data; and

- how information could best be provided to meet the needs of users.

This discussion paper seeks views from interested parties on what aspects of the Points of Presence data collection and publication users value and would like to maintain, and suggestions to improve the data collection and publication.

The current Points of Presence data collection and publication helps identify trends in the provision of physical banking service channels across Australia. The publication is not designed to assist individual consumers to find the specific location of a banking service, or when a banking service may be available. It is more appropriate for consumers to seek this information from individual providers.

Instead, the Points of Presence data can help identify:

- whether particular banking services (such as a bank branch or an ATM) are available within a geographical area, as defined by the Australian Bureau of Statistics (ABS);

- the number of banking services available in that area, and the number of alternatives to bank branches, such as the location of ATMs, EFTPOS or Bank Post facilities; and

- how the availability of those services has changed over time.

1.2 Scope of this consultation

Consultation on the Points of Presence data collection and publication will occur in two parts.

1. Scope user needs

This first discussion paper seeks stakeholder feedback on what users value about the Points of Presence data collection and publication, and how the current data collection and publication could be improved.

2. Propose solutions

Based on the outcomes of the first consultation, APRA will then seek feedback on proposed changes to the Points of Presence data collection and publication in a second discussion paper.

This first discussion paper is intended to be broad, giving stakeholders the opportunity to provide feedback on aspects of the data collection and publication they value, raise issues they have encountered with the data collection and publication, and propose improvements.

APRA intends to take the following categories of issues into consideration.

a. User needs: who are the users of the publication, what do users consider to be the primary purpose of the data collection and publication, and what do users want and expect from the data collection and publication?

b. Definitions and categories: are the current definitions and categories used in the data collection and publication appropriate to meet user needs?

c. Coverage of services: APRA collects data on face-to-face points of presence, ATMs and EFTPOS machines. Are there other services that should be covered in the data collection and publication to meet user needs?

d. Coverage of service providers: APRA collects data on points of presence provided by ADIs and Bank@Post providers. Is this coverage sufficient to meet user needs?

e. Accessibility and other matters: are there other matters, including in relation to access and accessibility, that are not covered in the above four categories and should be considered?

APRA will consult with other government agencies and with both industry and consumer representative groups as the review progresses.

APRA will also consider requests from interested parties for targeted online forums, providing an additional platform for community and consumer groups to ask questions and provide feedback (see Chapter 3 for details).

1.3 Further information

The latest ADI Points of Presence publication for June 2022 can be found on the APRA website. Annual data is provided from June 2017 (when APRA first began collecting data under the latest reporting standard) to June 2022.

Publications from prior years can be found in the Australian Government Web Archive, at the following links. These archived publications reflect the reporting requirements, and the data submitted to APRA, at the time the respective publications were finalised.

| Year and web link | How to access |

|---|---|

| Archived data from 2001 to 2010 | Links are provided on the archived page for each year of data. |

| Archived data from 2011 to 2016 | Calendar can be used to access data from different years. |

| Archived data from 2017 to 2018 | Calendar can be used to access data from different years. |

| Archived data from 2019 to present | Calendar can be used to access data from different years. |

Information on the latest Points of Presence publication for June 2022 can be found in the following documents on the APRA website:

- Excel spreadsheets (containing both aggregate and detailed data);

- Explanatory Notes; and

- Glossary, which includes the definitions used in the publication.

APRA Reporting Standard ARS 796.0 Points of Presence (ARS 796.0) provides full details on the information ADIs are required to report to APRA, including definitions of points of presence categories.

Chapter 2 - Points of Presence data collection and publication

2.1 What is the Points of Presence data collection and publication?

ADI Points of Presence data is released annually by APRA. It is a detailed listing of the physical banking service channels provided across Australia by ADIs.

APRA collects Points of Presence data within the framework established by the Financial Sector (Collection of Data) Act 2001 (the Act). The Act enables APRA to collect certain data from financial sector entities and authorises APRA to make reporting standards specifying the data to be reported by those entities.

The Points of Presence publication provides detailed information at a sector, institution, location and service channel type level. The individual points of banking presence are categorised using the Australian Statistical Geography Standard (ASGS), which classifies the locations according to remoteness. The latitude and longitude of each location is provided for use within third party mapping software.

Data for the Points of Presence publication is collected under ARS 796.0, which also provides definitions of the different points of presence categories.

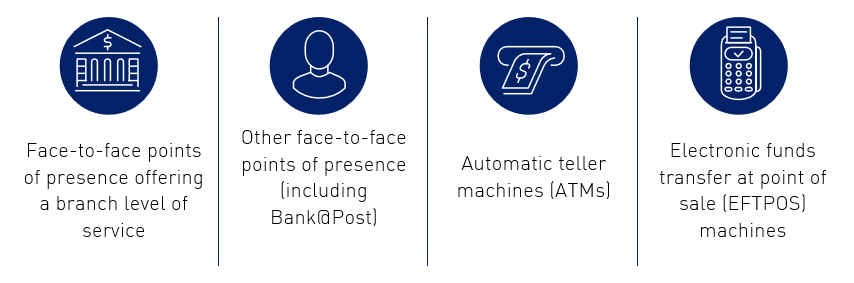

The Points of Presence publication currently covers four types of service channels:

The publication does not include information on the following:

- which banking services are provided at a physical point of presence;

- services without a fixed location, such as mobile bankers and travelling employees;

- non face-to-face banking services, such as online or via mobile banking applications;

- services provided by entities that are not ADIs or Bank@Post providers, such as ATMs and funds transfer facilities operated by other service providers; and

- services outsourced by ADIs to other service providers, such as ATMs operated by a service provider under agreement with an ADI.

2.2 Origins of the data collection and publication

The Points of Presence data collection and publication stemmed from the Commonwealth Government’s response to the recommendations of the October 2000 House of Representatives Standing Committee on Economics, Finance and Public Administration 'Review of the Australian Prudential Regulation Authority: Who will Guard the Guardians?'. Recommendation 2 of this report stated:

"That APRA provide yearly statistics which include the location and level of face-to-face banking in Australia."

The recommendation was based on an earlier report from the same Committee, 'Regional Banking Services: Money too far away', published in March 1999. This report highlighted the gap in information on the delivery of banking services:

"…the statistical information that is readily and officially available is of limited use in compiling a picture of the delivery of financial services through branches and agencies … it is essential that information is collected on all institutions in a uniform manner."

As a result of these recommendations, APRA began collecting and publishing information on ADI points of presence. The data were first published in March 2002, reflecting data as at June 2001.

The database began as a list of the number of bank branches provided by ADIs in each State and Territory, but eventually expanded into a large database listing the number of bank branches and other face-to-face points of presence by remoteness, the number of non-face-to-face points of presence, and the location of banking services provided at Australia Post outlets (originally giroPost, now Bank@Post).

2.3 2015 - 2016 APRA review

During 2015 and 2016, APRA reviewed the Points of Presence data collection and publication to ensure it remained relevant and useful. The review sought feedback on whether APRA should streamline, or cease, the Points of Presence publication to ease the reporting burden, consistent with the Government’s deregulation agenda.

APRA proposed to streamline the types of service channels, so they were more easily identifiable, measurable and comparable, as well as easily understood by users.

The review found the costs to the banking industry of the Points of Presence publication were small. APRA therefore continued to collect and publish points of presence data, but in a modified form. APRA implemented the following revisions to the publication:

- established a tighter definition of other face-to-face points of presence (excluding points of presence without a fixed location, such as mobile lenders and travelling employees);

- removed the requirement to report non-face-to-face points of presence (such as unmanned branches, telephone banking, internet banking and call centres);

- collected more accurate locational data of the points of presence (latitude and longitude); and

- captured additional information about the remoteness of these locations using the ASGS.

The revised format of the publication commenced in 2017.

2.4 Regional Banking Taskforce

On 22 October 2021, the Taskforce was established by the Government to analyse the trends in bank branch closures in regional and remote Australia, assess the impacts of branch closures, assess how banks transition their services and delivery models and identify alternatives to bank branch models. The Taskforce found that more could be done to support consumers to transition to other banking alternatives when bank branches close.

The Taskforce also found that there were gaps in the current Points of Presence data collection and reporting arrangements. In particular, the Taskforce noted that the Points of Presence publication:

"…does not include data on banking services provided online or via mobile banking applications, a key issue in an increasingly digital world."

The Taskforce recommended APRA review its Points of Presence collection:

"...the Taskforce recommends APRA review its Points of Presence collection to better capture indicators of how banking services are accessed, including through digital channels. This should be undertaken in consultation with industry and data users and include consideration of how to assess how banking services are accessed in different ways.”

Recommendation 7 of the Taskforce Final Report is provided below:

"Australian Prudential Regulation Authority (APRA) to commence in 2022 a review of its Authorised Deposit-taking Institutions (ADI) Points of Presence collection to better capture indicators on how banking services are accessed, with public consultation in early 2023."

APRA’s review implements Recommendation 7 of the Taskforce Final Report.

2.5 2023 Inquiry into Bank Closures in Regional Australia

On 8 February 2023, the Rural and Regional Affairs and Transport References Committee of the Senate Standing Committee on Rural and Regional Affairs and Transport began an inquiry into bank closures in regional Australia (‘the Senate Inquiry’). The Senate Inquiry will, among other matters, examine APRA’s Points of Presence data collection:

"…the effectiveness of government banking statistics capturing and reporting regional service levels, including the Australian Prudential Regulation Authority's authorised deposit-taking institutions points of presence data".

APRA looks forward to supporting the work of the Senate Inquiry through its review of the Points of Presence data collection and publication.

Chapter 3 - Consultation

3.1 Request for submissions

APRA welcomes feedback on all aspects of the matters raised in this discussion paper. The following questions are intended to identify specific areas for feedback that would assist APRA in determining improvements to the Points of Presence data collection and publication. They are intended to support, but not limit, responses.

APRA seeks perspectives regarding:

- the purpose and usefulness of the Points of Presence publication;

- aspects of the Points of Presence publication users value and wish to retain;

- suggestions to improve the usefulness of the publication; and

- ADIs’ ability to provide more detailed information on banking services.

When responding to the questions, APRA would appreciate submissions addressing the questions separately, in question-and-answer format.

Written submissions should be addressed to: Manager, ADI Strategic Insights and sent by Friday, 23 June 2023 to:

OR

Australian Prudential Regulation Authority

GPO Box 9836

SYDNEY NSW 2001

Australia

Questions on the consultation process can be directed to pointsofpresence@apra.gov.au.

To the extent possible, in addition to requesting written submissions, APRA will undertake targeted consultation with both industry and consumer representative groups.

3.2 Discussion questions

3.2.1 User needs in an increasingly digital world

As noted by the Taskforce, ADIs have been consolidating their branch networks and providing alternative modes of service delivery, such as online and telephone banking. The closure of local bank branches can affect the accessibility of banking services, particularly in regional communities.

The Taskforce considered it important to know what banking options are available and where (including virtual options). APRA is seeking feedback on how stakeholders use the Points of Presence data, and what types of services are important to identify. APRA is also seeking information on the design of the publication and how it could be improved.

| Discussion questions |

|---|

1. What do you consider to be the primary purpose of the Points of Presence publication? For what purpose(s) do you use the publication? 2. What information do you need from the publication, and how does this compare to the information received? How does your location (e.g. living in a regional or remote area) affect what you need from the publication? |

3.2.2 Definitions and categories

The current definitions and categories in the Points of Presence publication are broad. APRA seeks feedback on whether the current categories provide sufficient detail on the availability of banking services in particular locations. Examples of current categories are ‘branch’ and ‘other face-to-face’ points of presence (see below).

Definitions of ‘branch’ and ‘other face-to-face’ points of presence

ARS 796.0 provides definitions of the categories of ‘branch’ and ‘other face-to-face’ points of presence.

A face-to-face point of presence must satisfy the following criteria:

a) provide face-to-face services; and

b) maintain a fixed address.

Face to face points of presence are categorised as either a branch or another face to face point of presence, based on whether or not the point of presence meets APRA’s minimum branch requirements.

For a face to face point of presence to be categorised as a branch, the following minimum face to face services must all be provided.

A branch:

a) accepts cash and other deposits (including business deposits) and provides change;

b) facilitates the keeping of accounts for customer access, including the provision of account balances;

c) opens and closes accounts;

d) can facilitate or arrange the assessment of the credit risk of existing and potential customers; and

e) offers additional services in the one establishment such as financial services, business banking and specialist lending, if these are generally available from the ADI.

Paragraph e) above does not necessarily mean that a financial adviser or business credit manager is to be available at the branch – the staff of the branch may simply act as a referral point for customers interested in these kinds of services.

A point of presence that satisfies the criteria to be a face-to-face point of presence but does not provide all of the minimum face-to-face services to be categorised as a branch will fall into the category of other face-to-face point of presence.

Examples of other face-to-face points of presence include but are not limited to agencies, head offices, mini-branches etc. This category includes Bank@Post points of presence.

The Taskforce identified several alternatives to traditional bank branches, listed in the table below, which may be classified either as a ‘branch level of service’ or ‘other face-to-face’ point of presence, depending on the type of services provided.

| Alternative service | Description |

|---|---|

| Co-location | Banking services are co-located with other businesses |

| Co-branding | Different bank brands are co-located |

| Community bank | Franchise or joint venture relationship between a bank and a local company |

| Banking hub | Several banks use a common space to provide in-person services |

| Advisory hub | Space where banks provide information |

| Smart ATM | Provide more services than a ‘standard’ ATM, including accepting deposits |

Other types of banking services tailored to the needs of individual communities, such as mobile banking services in remote communities, are also becoming more prevalent.

| Discussion questions |

|---|

7. What categories of banking services are important to identify? 8. Do the definitions and categories used to distinguish points of presence (branches, other face-to-face including Bank@Post, ATMs, EFTPOS machines) meet user needs? What improvements could be made? 9. Does location identification (e.g. latitude and longitude, statistical area, suburb or town, remoteness area) meet user needs? What improvements could be made? 10. If you are a provider of information (an ADI), would it be feasible for you to provide more detailed information to APRA on individual points of presence(for example, more specific descriptions of banking services)? What are the costs to your business of reporting more detailed information to APRA? 11. Should the Points of Presence publication capture trends and innovatons in the delivery of banking services (such as deposit-taking ATMs, Business Centres, mobile bankers)? |

3.2.3 Coverage of services

The Taskforce noted in its final report that “[to] better understand and plan the transition away from branches, it is important to know what banking options are available and where (including virtual options)”.

Digital, online and mobile banker services do not have a fixed location, so these services would need to be measured by other means; for example, the availability and/or accessibility of a service in a particular location, or the frequency of use of a service in a particular location.

| Discussion questions |

|---|

12. What services, if any, would you consider to be appropriate substitutes for branch-level services? 13. What banking services are currently included in the Points of Presence publication that should be retained? |

3.2.4 Coverage of service providers

Some services provided by ADIs are also provided by entities that are not ADIs. Services include:

- payment services and payment platforms;

- lending services; and

- ATMs.

Currently, APRA collects data on ADI and Bank@Post points of presence only. The publication does not include information on services provided by other third-party service providers and non-ADI providers, which could potentially be considered substitutes for branch-level services.

| Discussion questions |

|---|

16. Do you consider services by non-ADI providers to be substitutes for branch-level banking services? 17. Does a publication that covers banking services only provided by ADIs and Bank@Post providers meet user needs? |

3.2.5 Accessibility and other issues

APRA welcomes any other suggestions and feedback on the Points of Presence publication. This can include any feedback relating to information on access to, and accessibility of, points of presence.

Examples could include access for consumers with disability, hours of access, or reliance on third-party assistance to access banking services. This will provide APRA with additional context on other matters users may consider when accessing banking services.

| Discussion questions |

|---|

18. Are there any issues in relation to access to and/or accessibility of ADI points of presence you wish to raise? 19. Are there any other issues with, or improvements to, the publication you wish to raise? |

3.3 Disclosure requirements – publication of submissions

All information in submissions will be made available to the public on the APRA website unless a respondent expressly requests that all or part of the submission is to remain in confidence. Automatically generated confidentiality statements in emails do not suffice for this purpose. Respondents who would like part of their submission to remain in confidence should provide this information marked as confidential in a separate attachment.

Submissions may be the subject of a request for access made under the Freedom of Information Act 1982 (FOIA). APRA will determine such requests, if any, in accordance with the provisions of the FOIA.

Information in the submission relating to the affairs of any financial sector entity that is not in the public domain and that is identified as confidential will be protected information under section 56 of the Australian Prudential Regulation Authority Act 1998. Protected information is exempt from production under the FOIA.