Clarification on APRA's data on average housing loan figures

The Quarterly Authorised Deposit-taking Institution Property Exposures (QPEX) statistical publication provides bank, credit union and building society aggregate statistics on commercial property exposures, residential property exposures and new residential loan approvals. The QPEX publication is published each quarter on APRA’s website.

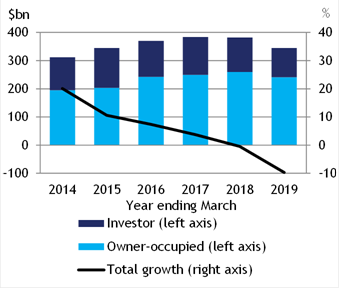

In the most recent QPEX publication – March 2019 (issued in June 2019), APRA’s data (as seen in Chart 1) highlighted negative growth in housing lending over 2018. Between the year ending 31 March 2019 and 31 March 2018, there was a decrease of:

- 7.2 per cent in owner-occupied new housing loan approvals, and

- 14.9 per cent in new housing investment loans.

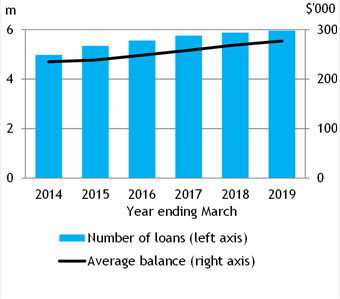

While there has been a decrease in housing loan approvals, the average loan size has continued to grow (as seen in Chart 2).

Since the last QPEX (December 2018) was published, some commentators have misinterpreted APRA’s data in their analysis of the average balance of housing loans. They have assumed that an increase in the number of housing loans (as seen in Chart 2) meant an increase in the number of borrowers with a housing loan. This misinterpretation has resulted in a suggestion that the average balance of housing loans represents the level of indebtedness of Australian households. This conclusion cannot be drawn from the data.

The QPEX publication reports data from the ADI’s perspective (e.g. the value of loans and number of loan accounts on the ADI’s books) rather than the borrower’s perspective. The data is a simple average calculated as the total balance of all housing loans divided by the total number of housing loans extended by ADIs. In practice, a customer may have multiple housing loans, which means that the average balance of housing loans cannot be used to determine the average housing debt of each borrower. When APRA supervises an ADI, we do not consider the average loan size to be a reliable indicator of risk; rather the data is just one of many inputs to identify potential changes to the overall structure and size of loans.

APRA requires ADIs’ to maintain high lending standards to ensure they are effectively managing risk when issuing new housing loans to borrowers. When a borrower applies for a housing loan, APRA requires the ADI to assess the borrower’s ability to repay the loan, taking into account the borrower’s other debt commitments and everyday expenses. We set out our expectations for ADIs on lending standards in Prudential Practice Guide APG 223 Residential Mortgage Lending.

The article was first published in APRA Insight - Issue 1 2019.