Many authorised deposit-taking institutions (ADIs) have granted temporary relief to borrowers impacted by COVID-19, allowing them to defer loan repayments for a period of time. To provide greater transparency of loan repayment deferrals at the industry level, APRA is publishing the aggregated data obtained from Australia's 20 largest ADIs.

*the number of facilities does not necessarily indicate the number of borrowers as individual facilities with more than one repayment type may be reported more than once.

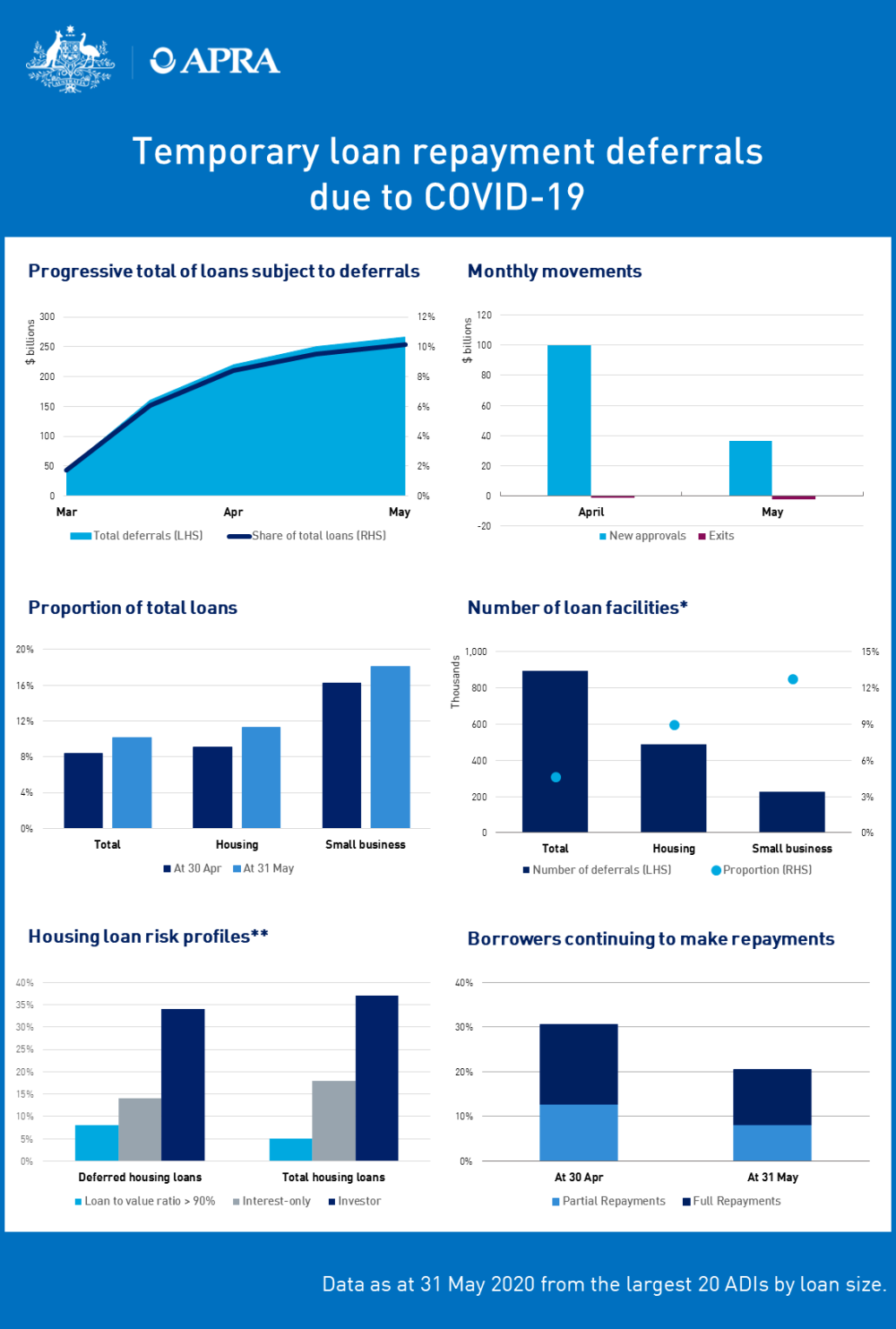

**to give an indicator of potential elevated risk in loans subject to deferral this chart compares loans subject to deferral to total loans across three key cohorts - loan to value ratio of greater than 90 per cent, investor loans and interest only loans.

An accessible version of the dashboard, with data labels, is available here.

Additional commentary

| Deferred loans | Total loans | Deferred loans, share of total loans | |

|---|---|---|---|

| Total | $266 billion | $2.6 trillion | 10% |

| Housing | $192 billion | $1.7 trillion | 11% |

| Small business | $56 billion | $311 billion | 18% |

As at 31 May, data submitted by the 20 largest ADIs indicates that $266 billion worth of loans have been granted temporary repayment deferrals, which is close to 10 per cent of total loans outstanding. Housing loans make up the majority of total loans granted repayment deferrals, although small business loans have a higher incidence of repayment deferral with 18 per cent of small business loans subject to repayment deferral, compared with 11 per cent of housing loans.

The rate of increase in loans now subject to repayment deferrals between April and May has slowed as applications reduced in May and some ADIs continue to work through processing high volumes of applications received in April. The pace at which loans become subject to repayment deferrals will be dependent upon a number of factors. The reduction from April to May does not necessarily indicate a trend.

The temporary repayment deferral programs were implemented within tight timeframes and the data has been submitted to APRA on a best endeavours basis. As ADIs improve their ability to capture these data items, resubmissions are expected. APRA will continue to publish this aggregate information on a monthly basis until loans subject to repayment deferrals are no longer a notable component of the ADI industry’s total loan portfolio.