Opening Statement to Senate Economics Legislation Committee - October 2020

Wayne Byres, Chairman – Senate Economics Legislation Committee, Canberra

Thank you for the opportunity to appear today. The last time we were before this Committee to discuss APRA’s activities was in March. It would be no understatement to say the world has changed a great deal since then.

As it did for all societies, businesses and governments, the COVID-19 pandemic significantly and suddenly changed APRA’s operating environment. The health crisis brought with it an economic crisis and subsequent economic contraction that has been more severe than anything seen since the Great Depression. This had, and will continue to have, a material and ongoing impact on all of the industries that APRA oversees.

As I’ve said on every available occasion, Australia went into this crisis with a financial system in a strong, stable position. That has been a critical factor in allowing the financial sector to play its natural role in absorbing risk and acting as a shock absorber for the rest of the economy.

Nevertheless, the onset of COVID-19 required APRA to quickly reset and reshape its priorities. APRA had a wide-ranging and ambitious agenda for 2019/20 and beyond, responding to the many reviews and inquiries into the financial system in earlier years. COVID-19 meant that there had to be a rapid reassessment of those priorities, and a redeployment of resources to focus on the core operational and financial resilience of the sector.

To recap on the past seven months, the COVID-19 response measures APRA has undertaken include:

- providing timely and targeted regulatory concessions designed to enable financial institutions to support their customers in a period of crisis (such as through the substantial program of loan deferrals);

- reducing regulatory burden (for example, by suspending major policy and supervisory initiatives) at a time when industry participants needed to devote all of their time and attention to maintaining their operations and helping the Australian community;

- supporting broader Government stimulus measures and policy responses, such as the early release of superannuation;

- collecting and publishing additional data to enable a transparent and objective view of the impact and success of various measures (including comprehensive weekly data on superannuation early release, and monthly bank-by-bank data on loan deferrals); and

- stressing the importance of the continued flow of credit, and making clear that the capital strength that has been built up in good times is available to be used in times such as these.

In providing regulatory relief and reducing burden, I do want to stress that we have sought to do this in a way that did not materially weaken the fundamental strength of the financial system. A stable and resilient financial system remains a critical foundation for Australia’s economic recovery, and we have been careful to make sure that our measures do not undermine this. It is with that in mind that we also issued two rounds of guidance to industry on dividend payments at a time of heightened uncertainty.

As we said at our appearance at the Senate Select Committee on COVID-19 in May, on the whole, the Australian financial system has responded well to the impact of the virus. Investments in financial resilience, risk management, cyber security and contingency planning, while never perfect, have stood up well thus far. However, we know there are still many challenges to come.

APRA’s updated priorities

Looking ahead, the immediate challenge of maintaining financial and operational resilience during a period of considerable stress and disruption remains front and centre for APRA. In particular, APRA’s priority over the next 12-18 months is to maintain financial system resilience by: protecting the safety and soundness of APRA-regulated institutions; fostering their operational resilience during a period of significant disruption and risk; and enhancing contingency plans for adverse events.

But we have not lost sight of the four key community outcomes that we set out to achieve in a 2019-2023 Corporate Plan. Those outcomes were:

- maintaining financial system resilience;

- improving outcomes for superannuation members;

- transforming governance, culture, remuneration and accountability across all regulated institutions; and

- improving cyber resilience across the financial system.

These outcomes were reaffirmed as our longer-term objectives in APRA’s 2020-2024 Corporate Plan, which we published in August.

We have also not lost sight of the need to address the recommendations arising from the various reviews and inquiries that took place during 2018-19, including those of the Royal Commission and APRA’s Capability Review. We expect many of these to be completed during the current financial year.

For the Committee’s information I have included with this statement three attachments:

- a list of regulatory measures taken by APRA over the past year in response to COVID 19;

- summary data on the outcome of the superannuation early release initiative, and the volume of loans subject to repayment deferral; and

- a summary of our strategy and plans for each of the industries we regulate, as well as our cross-industry strategy.

I hope you will find that information useful.

My colleagues and I would now be happy to take your questions.

Attachments

Attachment 1 - APRA COVID-19 Initiatives

Date (2020) | Industries Affected | Action |

19 March | ADI | Regulatory concessions: APRA advised temporary changes to its expectations regarding bank capital ratios, to ensure banks are well positioned to continue to provide credit to the economy in the current challenging environment. |

23 March | ADI | Regulatory concessions: APRA advised temporary concessions to facilitate the COVID-19 support packages being offered by banks and other lenders to their borrowers in the current environment. |

23 March | ADI, LI, GI, PHI, Super | Reduce burden: APRA suspended the majority of its planned policy and supervision initiatives in response to the impact of COVID-19. |

24 March | ADI, LI, GI, PHI, Super | Reduce burden: APRA announced the temporary suspension of its program to replace APRA’s Direct to APRA (D2A) data collection tool with APRA Connect. |

25 March | LI | Regulatory concessions: APRA postponed an upward capital adjustment in relation to Individual Disability Income Insurance (IDII), which applied to many LI entities. |

30 March | ADI | Facilitate public sector support: APRA confirmed its regulatory approach to the Term Funding Facility (TFF) announced by the Reserve Bank of Australia (RBA) on 19 March 2020. |

30 March | ADI | Reduce burden: APRA announced it would defer its scheduled implementation of the Basel III reforms in Australia by one year, from 2022 to 2023. |

31 March | PHI | Reduce burden: APRA postponed implementation of reporting standard on private health insurance reforms data collection. |

1 April | ADI (and RFCs) | Reduce burden: APRA, along with ABS and RBA, announced a range of adjusted reporting requirements. |

1 April | Super | Regulatory guidance: APRA and ASIC issued guidance to help trustees manage the financial and operational challenges associated with COVID-19, while continuing to meet their obligations to look after members’ best interests. |

7 April | ADI, LI, GI, PHI | Regulatory guidance: APRA wrote to all ADIs and insurers to provide guidance on capital management during the period of significant disruption caused by COVID-19. Amongst other things, the guidance recommended deferring dividend decision for the next couple of months. |

8 April | ADI, LI, GI, PHI, Super | Regulatory guidance: APRA wrote to applicants for new banking or insurance and superannuation licences to advise that it is temporarily suspending issuing new licenses for at least six months in response to the economic uncertainty created by COVID-19. |

16 April | Super | Facilitate public sector support: APRA published expectations on the release of benefits under the COVID-19 temporary early access to superannuation provisions. |

16 April | ADI, LI, GI, PHI, Super | Reduce burden: APRA announced delayed start dates for six prudential and reporting standards that have been finalised but are yet to come into effect. |

17 April | ADI | Facilitate public sector support: APRA released new reporting standard to enable data collection in relation to the Government’s SME Guarantee Scheme. |

21 April | Super | Facilitate public sector support: APRA launched new data collection to assess progress and impact of the Government’s temporary early release of superannuation scheme. |

4 May | Super | Transparency: APRA publishes data on amount, value and timeliness of aggregate payments under the Government’s temporary early release of superannuation scheme. |

7 May | ADI | Regulatory concessions: APRA published additional guidance to assist ADIs in relation to the regulatory treatment of loan repayment deferrals and expectations in relation to mortgage serviceability assessments. |

11 May (and weekly thereafter) | Super | Transparency: APRA published fund-level data on amount, value and timeliness of payments under the Government’s temporary early release of superannuation scheme. |

19 May | ADI | Regulatory guidance: APRA published additional guidance to assist ADIs in relation to their market risk capital requirements. |

17 June | ADI | Regulatory concessions: APRA published frequently asked questions (FAQs) on expectations in relation to residential property valuations. |

24 June | Super | Transparency: APRA launched a new COVID-19 Pandemic Data Collection to enable assessment of the impact of COVID-19 on the superannuation industry and the outcomes being delivered to members. |

7 July | ADI | Regulatory guidance: APRA published additional guidance to assist ADIs in relation to the capital treatment of securitisation schemes. |

8 July | ADI | Regulatory concessions: APRA announced an extension of its temporary capital treatment for bank loans with repayment deferrals, as well as temporarily adjusting the capital treatment of loans where terms are modified or renegotiated (‘restructured’). |

9 July (and monthly thereafter) | ADI | Transparency: APRA released the aggregate industry data on the amount, type and risk profile of loan repayment deferrals. |

22 July | Super | Regulatory guidance: APRA published frequently asked questions (FAQs) providing guidance to superannuation trustees on the COVID-19 Pandemic Data Collection requirements. |

24 July | ADI | Regulatory concessions: APRA published frequently asked questions (FAQs) on expectations in relation to commercial property valuations. |

29 July | ADI, LI, GI, PHI | Regulatory guidance: APRA updates its guidance on capital management for banks and insurers, emphasising the importance of keeping dividend payments to moderate levels (ADIs encouraging to retain at least half their earnings). |

10 August | ADI, LI, GI, PHI, Super | Resumption of activities: APRA announced recommencement of its prudential policy program and a phased resumption of the issuing of new licences. |

13 August | ADI | Regulatory consultation: APRA issued a letter to ADIs regarding consultation on treatment of loans impacted by COVID-19. |

9 September | ADI | Regulatory concessions: APRA formalised the temporary concessions in relation to the regulatory treatment of loans subject to repayment deferrals, and the concessional treatment for loans being restructured. |

22 September | ADI | Regulatory guidance: APRA issued a letter to ADIs in relation to the outcomes from its review of ADIs’ plans for the assessment and management of loans with repayment deferrals. |

1 October | Super | Regulatory guidance: APRA published guidance on the interaction between JobKeeper payments and ‘work test’ contributions. |

21 October | Super | Reduce burden: APRA announces updates to the Early Release Initiative (ERI) data collection and COVID-19 Pandemic Data Collection (PDC), with some data items to be discontinued. |

Attachment 2 - Summary data

- Summary data on the outcome of the superannuation early release initiative

- Summary data on the volume of loans subject to repayment deferral

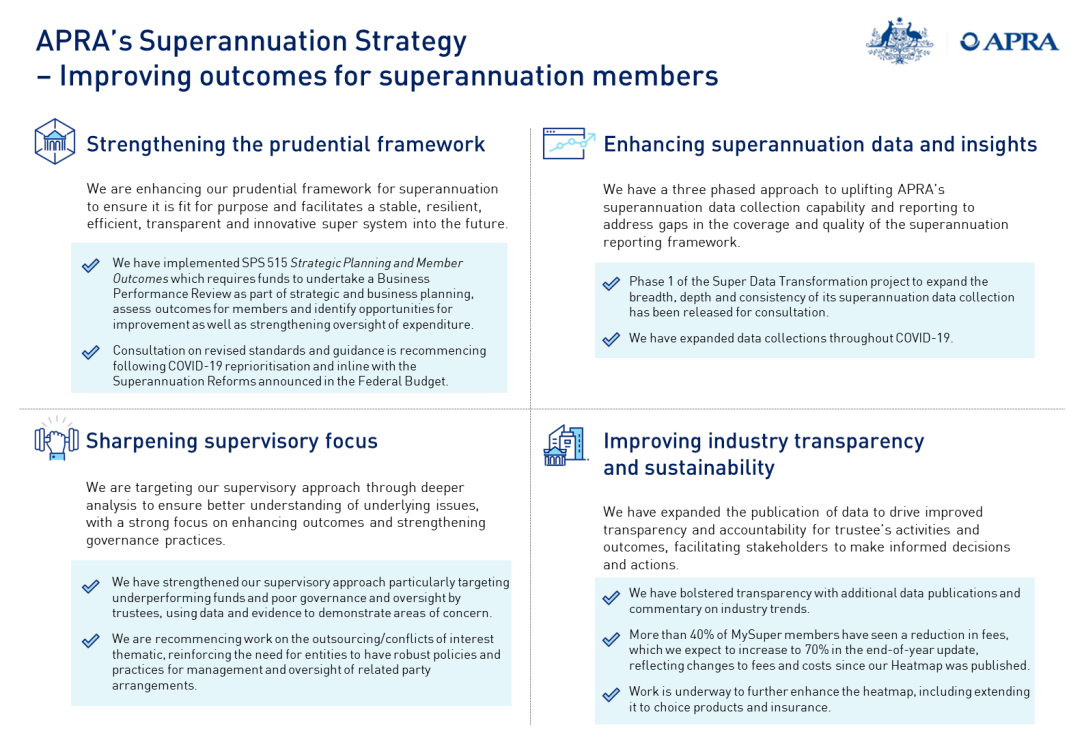

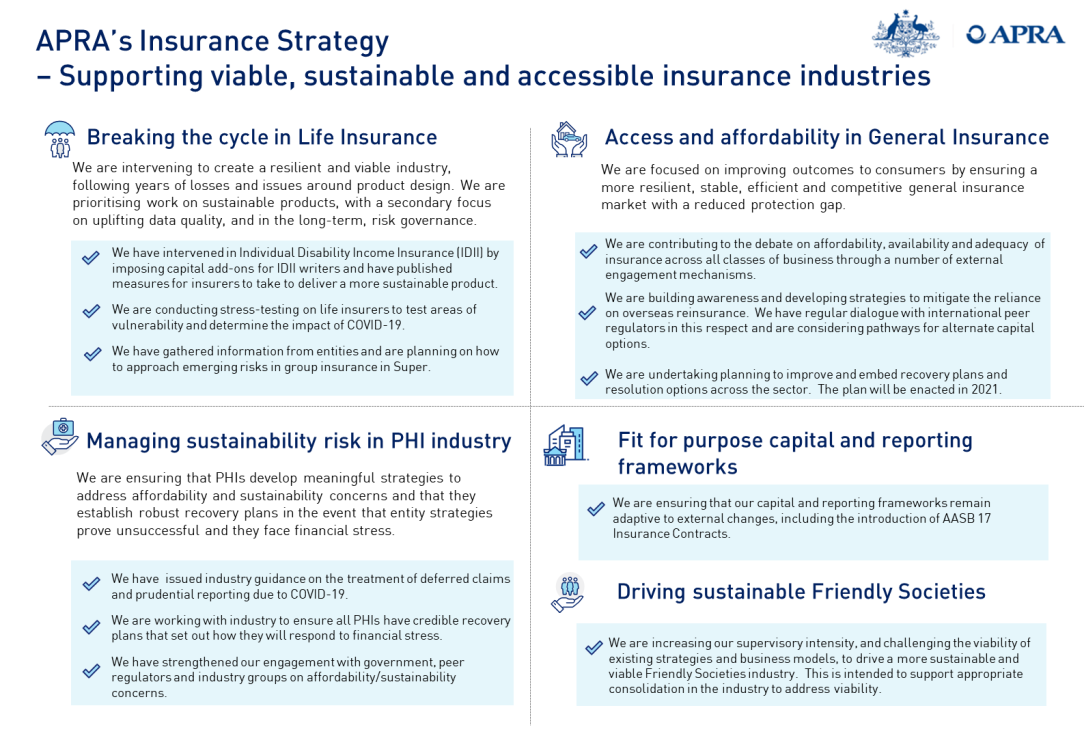

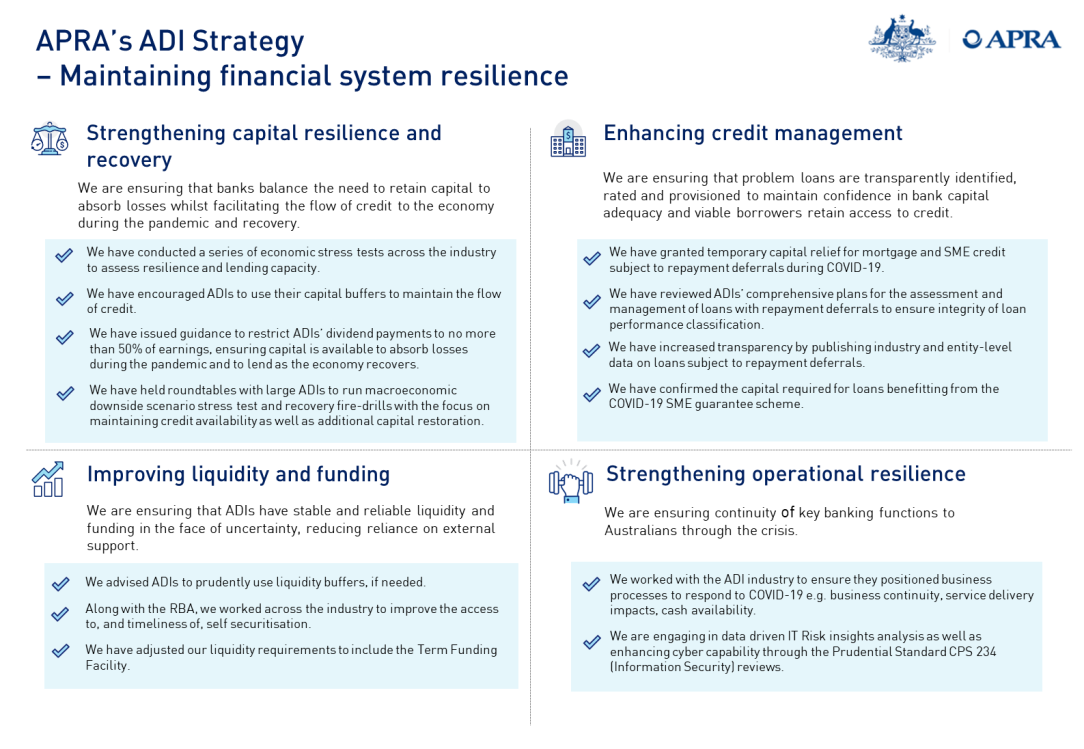

Attachment 3 - Summary of APRA's strategy and plans

Media enquiries

Contact APRA Media Unit, on +61 2 9210 3636

All other enquiries

For more information contact APRA on 1300 558 849.

The Australian Prudential Regulation Authority (APRA) is the prudential regulator of the financial services industry. It oversees banks, mutuals, general insurance and reinsurance companies, life insurance, private health insurers, friendly societies, and most members of the superannuation industry. APRA currently supervises institutions holding $9.8 trillion in assets for Australian depositors, policyholders and superannuation fund members.