Creating Strong Competitors

Thank you for inviting me to again be part of COBA’s annual conference.

In the time I have this morning, I want to reflect on a number of issues impacting the competitive landscape facing mutual banks. Given our own influence on your operating environment, I will start today by talking about how we think about competition within our mandate. I then want to make some observations about the current competitive position of smaller banks in what is an increasing difficult operating environment. And before I conclude I’ll wrap up with some comments on the way in which we are thinking about competitive impacts as we go about the important task of finalising the revisions to the capital adequacy framework.

In doing so, COBA’s theme for this event – ‘Stronger Together’ – is very apt. From APRA’s perspective, there are no doubt opportunities for you in the current environment. But there are also plenty of challenges and headwinds. Regardless of whether it is taking advantage of the opportunities, or overcoming the challenges, working together will be an essential foundation of a prosperous and competitive mutual bank sector.

APRA’s mandate

As you all know well, our goals when it comes to banking are, very simply, to protect bank depositors and promote financial stability.

That said, in banking and in the other industries we are responsible for, we are not tasked with ensuring nothing can go wrong. To attempt to provide the community with an iron clad guarantee that nothing can go wrong would require a zero risk financial system. A zero risk system will have zero activity, and therefore generate zero value. At the other extreme, it’s pretty clear a financial system with no constraints would inevitably lead to significant instability – well beyond the tolerance of the community to bear. The ideal balance for regulators is obviously somewhere in-between, balancing the financial safety that we desire for the community with the trade-offs needed to achieve that safety.

Our mandate under the APRA Act reflects this, and is therefore quite nuanced. The Act tasks us with pursuing our primary safety objective, but also says we should balance that with considerations of efficiency, competition, contestability and competitive neutrality. In other words, the Australian Parliament has said we should not pursue a ‘safety-at-all-costs’ strategy. Nonetheless, the Parliament has also said that in whatever trade-offs we make, our decisions and actions should always be directed towards promoting financial stability. You might call this a ‘stability-at-least-cost’ mandate.

Our objectives are therefore interlinked. Sometimes they are mutually reinforcing; at other times, a balance between competing objectives is needed. We also try think beyond the particular circumstances of the day so as to maintain a sustainable balance over the longer run. To help explain how we go about this balancing act, we are today publishing an information paper that sets out how we interpret the various components of our mandate, and how we go about searching for the right balance.

Recent initiatives to support competition

For today’s purposes, I want to focus my remarks on the consideration of competition in particular.

It is sometimes asserted that the goals of stability and competition in the financial system are mutually exclusive – one must always be traded off against the other. That has not been our view.1 As we discuss in the paper, competition in the financial sector brings welcome innovation and enhanced outcomes for customers, and good regulatory settings deliver financially strong competitors, creating both financial stability and a dynamic and innovative marketplace for financial services. APRA’s prudential framework and supervision activities are designed to deliver sustainable competition from strong competitors: that is, competitors who will be there both in good times and bad. One only has to look at the out-workings of the 2008 financial crisis to see examples of business models that only worked in good times. The long-term outcome has unfortunately been a more concentrated system that is taking a long time to unwind.

That is not to say the issues of competition and stability do not sometimes involve a trade-off. Moreover, not all competition is unambiguously positive. For example, our interventions in housing over the past few years, with which you are all very familiar, had the explicit and unambiguous goal of dampening competitive spirits. These were playing out in a manner – through poor lending standards – that was likely to be damaging to the community in the long run. As the Productivity Commission concluded: “Competition and stability in the financial system can — and should — coexist. But … [a]lthough the legislation that requires APRA to give weight to competition is valuable, its remit quite reasonably must favour system stability.”2 Similarly, the recent APRA Capability Review noted: “APRA’s role is not to actively promote competition.3 … APRA’s philosophical approach [to not unduly hinder competition] and its application is reasonable.”4

Nevertheless, we are at times accused of neglecting competition in our zest for stability. Those comments sometimes overlook a number of steps we have taken in recent years with a competition perspective firmly in mind. These broadly fall into four categories:

- Facilitative measures: promoting more active competition by, for example:

i. providing for the issuance of mutual equity interests that allow mutuals to raise CET1 capital to fund their growth; and

ii. making our licensing regime easier to navigate for new entrants. As a result there were more new ADIs authorised in the past year than in any year in the past decade-and-a-half, including five domestically owned banks.

- Graduated approaches: avoiding undue costs on smaller competitors, including by:

i. setting differential targets for ‘unquestionably strong’ capital, with IRB banks facing a 150 basis point increase in capital and standardised banks only 50 basis points;

ii. imposing additional loss absorbing capital requirements only on the largest ADIs, rather than all ADIs as recommended by the FSI;5 and

iii. tailoring our proposed new remuneration requirements to impose more stringent requirements on the significant financial institutions, with more modest requirements for smaller ADIs.

- Simplification efforts: lifting the burden on smaller ADIs by measures such as:

i. proposing a new simplified capital adequacy framework for ADIs with assets under $15 billion (a threshold sufficient to capture the entire population of mutuals);

ii. managing the BEAR transition to provide smaller ADIs a longer time, and more guidance; and

iii. proposing changes to reporting requirements that will provide for longer reporting timeframes for smaller ADIs – in some cases almost doubling the time period that small ADIs will have to submit their returns to APRA.

- Lower supervisory intensity: ensuring supervisory intensity is applied where it is most needed from a systemic risk perspective by, for example:

i. targeting our housing interventions with respect to investor and interest-only lending first and foremost at the largest ADIs – as a result, notwithstanding the constraints at which everyone chaffed, smaller ADIs grew their market share throughout this period; and

ii. generally avoiding the inclusion of smaller, mutual ADIs in many thematic and industry-wide supervision activities where possible, so as to limit the costs we impose.

Each of these steps should, at the margin, improve the capacity of smaller players to compete against the largest banks. Collectively, they demonstrate that we have been quite mindful in thinking about where and how we can make sure our regulatory requirements are applied proportionately. No doubt you will think of other ideas, and amongst your list will probably be risk weights. I’ll come back to those shortly. But in the meantime I just want to emphasise that considerations of competition are increasingly embedded – in an increasingly structured manner – in the way in which we develop, refine and maintain the prudential framework. The extensive consultation process we go through whenever we make changes to the framework also ensures the issue cannot be forgotten – and I can attest the COBA team certainly plays its role in that regard quite actively.

Competitive position of smaller banks

Any discussion on competition in the Australian banking system inevitably focuses on the market dominance of the four major Australian banks. Their sheer scale and brand recognition, coupled with significant customer inertia, is difficult for smaller banks to overcome. This is despite the fact that, in many cases, their product offerings are superior in pricing to the big four.

| 1999 | 2004 | 2009 | 2014 | 2019 | |

|---|---|---|---|---|---|

| Major Banks | 4 | 4 | 4 | 4 | 4 |

| Other Domestic ADIs | 256 | 204 | 146 | 117 | 89 |

| of which: mutuals | 242 | 187 | 126 | 99 | 69 |

| Foreign bank subsidiaries | 11 | 11 | 9 | 8 | 7 |

| Foreign bank branches | 25 | 28 | 34 | 40 | 47 |

| Restricted ADIs | 0 | 0 | 0 | 0 | 1 |

| Total ADIs | 296 | 247 | 193 | 169 | 148 |

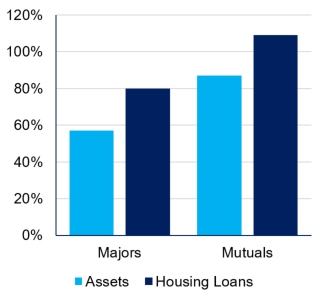

The seemingly ever-present dominance of the majors is in contrast to the dynamic nature of the mutual sector. Over the past decade, the number of mutual ADIs has almost halved as the industry has seen substantial consolidation (Table 1). Yet that consolidation has not hampered growth. Over the decade, mutual ADIs have grown their collective assets by 87 per cent; by comparison, the corresponding figure for the majors is 57 per cent (Chart 1). A similar story is told in the core business of lending for housing.

Moreover, I would contend that in recent times, smaller ADIs have developed some competitive advantages – the most critical of which is a far better reputation among consumers after the Royal Commission and other revelations of poor customer outcomes. This is contributing to the slow but steady erosion in the dominance of the majors. At the same time, the long-term decline in the share of mutuals appears to have definitely ceased and, albeit slowly, mutuals are starting to win back market share. For example, the share of housing loan approvals generated by the mutual sector is the highest it has been since the GFC, and broadly double that of a decade ago.

There is undoubtedly a real opportunity for the mutual sector to take collective advantage of its favourable perception. Working together is also important from a defensive perspective. There are many headwinds – economic, political and technological – facing the banking sector. Some are real and present dangers that must be faced today; others pose material threats to financial system if they were to play out adversely. And at least some of them will be felt by smaller firms most forcefully.

One issue is the current low interest rate environment. Margins across the industry are squeezed, adding to the headwinds from slow lending growth. Profitability, and therefore capital generation, will come under more pressure. As I have highlighted previously, these trends may well impact smaller banks more so than larger ones given different funding profiles6. Mutuals continue to generate higher income on their asset portfolios than the majors, but are more exposed to margin compression, given their reliance on low-rate transactional deposit accounts and higher margins to offset their materially higher cost base (Table 2).

| Majors | Mutuals | |

| Net interest income | 1.7% | 2.1% |

| Other income | 0.5% | 0.5% |

| Total income | 2.3% | 2.6% |

| Operating costs | 1.1% | 2.0% |

| Bad debt expense | 0.1% | 0.0% |

| Profit before tax | 1.1% | 0.5% |

| Tax | 0.3% | 0.2% |

| Profit after tax | 0.7% | 0.4% |

The low-for-long interest rate environment seems here to stay and will be part of the operating environment for a while yet. It means credit will continue to be very cheap, and while that may lead to some pick-up in credit growth, it is also likely that new competitors and business models – buy-now-pay-later being a current case in point – will emerge.

One way to respond is to look at costs – a traditional bugbear for smaller banks with relatively high-cost operating models. As I pointed out last time I was here, tackling costs is critical to being a stronger and sustainable competitive force in the Australian banking system. The large banks are relentless in driving costs out of the system. And new players are entering the marketplace – some as ADIs and some not – with low-cost models as a core of their value proposition.

Applying the theme for this event – ‘Stronger Together’ – in practice will be an important means for mutuals to do likewise. Looked at collectively, the mutual sector has $120 billion of assets and would rank as the sixth largest ADI in Australia – behind only the majors and Macquarie Bank. Given the increasing importance of scale as a means to offset a range of competitive headwinds – including the need to invest in new technology to meet changing consumer demands, boost operational resilience and head off cyber threats – collective initiatives that promote and support the mutual sector as a whole have the potential to generate the scale efficiencies that are needed to genuinely alter the competitive landscape. They are not necessarily easy, but they are likely to be essential.

Building resilience

Let me now quickly turn to capital. Although the GFC occurred more than 10 years ago, the remediation and strengthening of the financial system globally continues today. In fact, this process will never technically be complete. Even though Australia came through the crisis in better shape than most countries, we have never rested on our laurels and are continuing to work to build strength and resilience in regulated firms, and the system overall.

As you all would be aware, in February 2018, APRA released a broad package of proposed changes to the capital framework for ADIs flowing from the finalised Basel III reforms, as well as the 2014 Financial System Inquiry recommendation for the capital ratios of Australian ADIs to be ‘unquestionably strong’.

There is a lot of detail, but at a headline level the main components of the package for mutual banks are:

- a more granular approach to mortgage risk weights to better reflect risks in this core portfolio;

- reduced risk weights for SME lending; and

- more granular risk weights for other retail exposures.

In 2017, we set out what we thought was needed to achieve ‘unquestionably strong’ ratios in aggregate. Broadly speaking, it meant raising minimum capital requirements by 150 basis points for banks utilising the IRB approaches, and a 50 basis point increase for banks using the standardised approaches. That has required a build-up of capital for the larger banks; for the mutual bank sector, which currently operates with a CET1 ratio of 15.6 per cent, it is a hurdle that could be cleared without breaking stride.

The goal of the 2018 and subsequent papers has therefore been to determine how this capital is allocated across different business lines and products. I do not propose to go through the detail of the proposals today, but I want to make some general observations as to how our thinking is developing.

First, our objective has not changed. The targets we set in 2017 remain. We are not looking for further increases in capital in the system. So banks that meet these targets today can be reasonably comfortable they will meet whatever new framework is established.

That is not to say the increase for every standardised bank will be exactly 50 basis points, or 150 basis points for every IRB bank. These benchmarks represent average targeted increases across the industry, and the impact will inevitably be a bit less for some and a bit more for others. To the extent that is driven by a better allocation of capital to risk, it is also a fairer outcome across the system.

Second, it seems clear the latest proposals will need some recalibration. Broadly speaking, the results of the impact study we have conducted show that – relative to the 150 bps and 50 bps goals – the proposals are somewhat over-calibrated for standardised banks, and under-calibrated for IRB banks. So we will have to make some adjustments to what has been proposed to make sure we hit our targets.

This raises a related issue that COBA regularly highlights: the importance of the relativities between the two approaches. Here I want to highlight one of the important features of the new proposals: that banks using the IRB approach will need to calculate and disclose their ratios under both the IRB and standardised approaches. This will allow a direct, like-for-like comparison in capital levels, and make the debate about relativities much better informed.

That brings me to the final point I want to make, about mortgage risk weights. Much is made of the headline difference in risk weights between the IRB and standardised approaches. At first glance, they do indeed look different. But as we pointed out in our most recent discussion paper, the comparison is much more complex than a superficial comparison implies: there are differences in capital targets, the treatment of loan commitments, the application of capital for interest rate risk in the balance sheet, and adjustments to expected losses – all of which have the effect of adding to IRB bank capital requirements and mean that the headline gap is greatly narrowed in practice.

When looked at holistically, we think any gap is small. Perhaps most tellingly, we now hear from candidates for IRB status that they are concerned the proposals being developed will not provide them with any capital benefit whatsoever. Whether that is the case or not, we are very conscious of this issue in designing the new proposals, and we have explicitly stated that we intend that any differences will remain negligible.

Concluding remarks

Stability is easy to take for granted, but hugely costly once foregone. In a system notable for its relative stability, it can be easily forgotten that there have been around 150 systemic banking crises around the globe in the past 50 years.7 The cost of crises is invariably substantial. Stability will always remain APRA’s driving objective: we must stay true to our mandate to deliver a safe and stable financial system for the community.

We are, however, endeavouring to be more structured and systematic about the way we assess all of the components of our mandate – including competition – and be clearer in acknowledging the trade-offs being made. The paper we have released today is part of that process. And the regulatory changes in the pipeline are designed to make sure that competition occurs from a position of financial strength.

That said, it is important to recognise that the competitive landscape is shaped by more than regulation. Regardless of perceived regulatory headwinds, the mutual sector has grown strongly and won market share. That is to your great credit. The current environment, notwithstanding its challenges, offers you further opportunities. You will, to return to the theme of this event, undoubtedly be stronger together if you work collaboratively to grasp them, and I wish you every success in doing so.

1 See, for example, APRA’s Opening Statement to the Roundtable Hearing for the Productivity Commission Inquiry into the State of Competition in the Australian Financial System, 29 June 2017.

2 ‘Competition in the Australian Financial System’, Productivity Commission Report, No. 89, June 2018, p532.

3 APRA Capability Review Report, p69.

4 ibid, p71.

5 Financial System Inquiry (2014), Recommendation 3.

6 See ‘Financial instability: Prevention is better than cure’, Remarks to the European Australian Business Council, September 2019.

7 See Laeven, L and F Valencia (2018): "Systemic banking crises revisited", IMF Working Paper 18/206.