Insurance recovery planning thematic review – key observations

To: General insurers and life insurers

The purpose of this letter is to outline APRA’s observations from a recent recovery planning thematic review including areas of better practice. APRA conducted this thematic review with a group of in-scope large and medium-sized general insurers and life insurers (insurers). APRA assessed their recovery plans against the recovery planning guidance (the Guidance1) provided to the in-scope insurers. The Guidance is available to insurers through their APRA supervision team.

Building recovery and resolution capability, through improved planning, will remain a key strategic priority for APRA over the coming years. A recovery plan comprises a menu of options designed by a financial institution to enable it to survive a financial shock and restore itself to a sound financial condition without the need to seek public sector support. APRA will use the outcomes of the thematic review to inform its development of a prudential framework for recovery and resolution, which will include a prudential standard and accompanying guidance. APRA plans to consult on this framework next year.

APRA’s key observations from the thematic review, including areas of better practice, are set out in Attachment A. APRA encourages insurers to consider these observations in the ongoing development of credible recovery plans.

If you have any questions, please contact your APRA supervision team.

Yours sincerely

Geoff Summerhayes

Executive Board Member

1The Guidance was developed using the Financial Stability Board (FSB) Key Attributes of Effective Resolution Regimes for Financial Institutions, and the International Association of Insurance Supervisors (IAIS) standard on recovery planning (ICP 16).

Attachment A: Key observations

This section provides a summary of APRA’s key observations from the thematic review, including areas of better practice. APRA encourages insurers to consider the better practice examples alongside the existing Guidance in the ongoing development of credible recovery plans (referred to as the plan(s)).

APRA observed that the recovery planning process has assisted in-scope insurers to advance their overall approach to risk management, and to build a better understanding of the importance of recovery planning.

However, there remain considerable areas for improvement before in-scope insurers can be assessed to have credible plans in place that are effectively integrated with the risk management framework. APRA considers the usability of the recovery plan is a key factor when assessing its credibility. APRA expects recovery planning to be a dynamic process, where the plans continue to be assessed, tested and improved with ongoing board oversight.

1. Governance

Robust governance arrangements are essential both for effectively developing and maintaining the recovery plan, and for ensuring appropriate monitoring and escalation processes are in place to allow for timely implementation of recovery options.

i. Integration with risk management framework

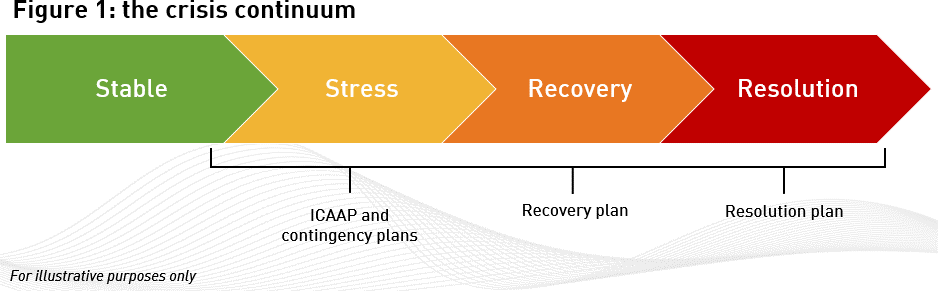

Recovery planning can be viewed as being at the more extreme end of the risk management continuum. Many of the plans assessed are not yet effectively integrated with the broader risk management framework. APRA expects the elements of the recovery plan including the escalation procedures, trigger framework, recovery options and communication strategy to be consistent and aligned with other risk management documents. Figure 1 provides an illustrative example of how recovery planning fits into the crisis continuum.

Better practice examples include:

- Integration with and cross-referencing to other risk management documents, where appropriate. This includes ensuring that the governance arrangements for escalation and activation of the plan are well understood and coordinated across the institution and recovery options can be implemented in a timely manner.

- Consideration of how the communication strategy in the recovery plan is aligned with the insurer’s broader approach to effective communication.

ii. Monitoring, escalation and activation processes

Weaker plans lack clarity on the processes for monitoring and escalating emerging issues. It is not clear how escalation procedures would work in practice, and the mapping of roles and responsibilities of key stakeholders needs to be strengthened.

Better practice examples include:

- Clear articulation of the link between the trigger framework and the governance arrangements within the plan. Stronger plans make use of diagrams and flowcharts to illustrate the link between their trigger framework and governance arrangements.

- Clear accountability mapping of the roles and responsibilities of key stakeholders for each stage of the monitoring and escalation process.

- Strong and clear decision-making mechanisms in place for activating the plan, and for selecting and implementing recovery options.

- Well-defined processes in place for how and when to notify regulators (local and foreign, where relevant), regarding an emerging crisis and any proposed response under the plan.

iii. Operational testing

Most in-scope insurers have not yet developed a sufficient framework for operational testing of plans. Regular operational testing of the plan is important, particularly to build confidence that the governance and escalation procedures in the plan are well understood, including by the board and senior management, and could be implemented in a timely manner in a crisis.

APRA considers it prudent for insurers to conduct regular (at least annual) dry-runs and training exercises focusing on internal escalation processes, the formation and functioning of crisis management teams and determination of communication strategies.

Better practice examples include:

- A planned and documented approach to regular operational testing of the plan, including identification of the key factors to be tested.

- Incorporation of the lessons learnt from operational testing into the plan to ensure its ongoing development.

2. Trigger frameworks

The trigger framework should operate in a manner which reflects the escalating nature of stress events, so as to facilitate timely contingency planning and the intensifying of responses as the severity increases.

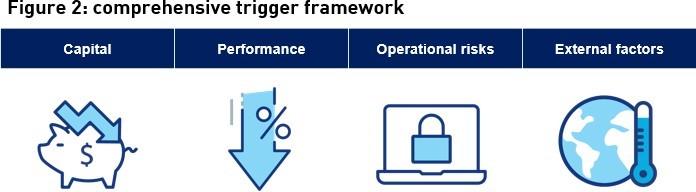

i. Range of metrics

A number of plans rely on a single capital trigger for activation of the plan instead of considering the use of a wider range of metrics to identify emerging risks across a variety of areas. The trigger framework should be aligned with the insurer’s broader risk management framework, and should be sensitive to deteriorating conditions across a variety of areas.

Better practice examples include:

- Incorporating a wide variety of early warning indicators (EWIs) and triggers. For example, the trigger framework can benefit from inclusion of metrics relating to capital, profitability and other performance metrics, sensitivity and volatility factors, reinsurance, external factors, liquidity, and the insurer's operational conditions.

- Considering a range of metrics, which include quantitative and qualitative criteria and include leading and lagging indicators, where possible.

ii. Timely trigger points

Stronger plans make use of a staggered trigger framework, so that the plan operates in a cascading manner to trigger intensifying responses as the severity of a stress increases, and does not rely on a single trigger point.

Better practice examples include:

- Indicators and triggers are calibrated early enough to allow sufficient lead time to plan for and implement recovery options. For example, where a hard capital recovery trigger point is utilised, it is calibrated to automatically activate the plan or prompt a decision to activate the plan well before the regulatory minimum is reached.

- Using a traffic light approach to the calibration of each metric for recovery planning purposes.

- Alignment between the calibration of trigger points in the plan to those metrics used in other related contingency plans, for example, the Internal Capital Adequacy Assessment Process (ICAAP), to create a cascading trigger framework.

3. Recovery options

The core element of a credible recovery plan is a comprehensive menu of realistic recovery options, supported by the requisite level of supporting analysis required to assess and implement the options.

i. Menu of recovery options

The majority of insurers consider a range of recovery options covering different aspects of the business, preparing the insurers to be able to respond to a number of different stress scenarios. However, APRA also expects insurers to consider recovery options that may have a significant impact on their business structure and strategy.

Better practice examples include:

- Comprehensive menus of recovery options, developed without being limited to any specific stress scenario.

- Consideration of recovery options which may have permanent structural or strategic implications for the insurer.

- Consideration of capital raising options, run-off of business lines, portfolio transfers and sales, reinsurance arrangements and changes to business and investment strategies.

ii. Valuations and assumptions of recovery options

Significant work is required in this area to strengthen the credibility of the plans. Many insurers did not sufficiently detail the estimated financial impacts of implementing the recovery options. While acknowledging that estimating a financial impact of a recovery option in a stress scenario is subject to many factors, it is important to do so, including to detail and test the valuation methodologies and assumptions.

Better practice examples include:

- Detailing the estimated financial benefit expected from implementing recovery options, including the assumptions and valuation methodologies. Financial estimates are useful to help inform whether implementing a recovery option may be, firstly, credible and, secondly, sufficient for recovery across different stress scenarios.

- Valuations and assumptions reflect the stressed conditions in which the recovery plan is intended to operate. For example, larger discounts are applied to recovery options in stressed conditions compared to what would be applied in normal operating conditions.

iii. Supporting analysis / playbooks for recovery options

This element is significantly underdeveloped across the majority of insurers, and APRA expects improvements in the next iteration of plans.

Better practice examples include:

- Incorporating an appropriate level of strategic, financial and operational analysis to assess the effectiveness of each recovery option, and to support its practical implementation.

- Strengthening the overall usability of a recovery plan through the development of operational ‘playbooks’ for the key cornerstone recovery options. Playbooks should be developed with the objective of maximising the insurer’s ability and readiness to execute the recovery option quickly in a crisis, and typically include additional detail on the implementation steps (including preparatory actions), accountability mapping, interdependencies across the business, expected timeframe analysis and the communication strategy.

4. Scenario analysis

The use of scenario analysis provides an important mechanism to help assess the credibility of the recovery plan, in particular the calibration of the trigger framework and feasibility of recovery options. The scenarios therefore need to be sufficiently severe to activate the recovery plan.

i. Severity of scenarios

Many insurers do not consider a range of scenarios that reach the level of severity required to activate the recovery plan. Additionally, few insurers consider non-financial risk scenarios, for example, impacts from an operational risk event.

Better practice examples include:

- Consideration of a broad range of stress scenarios, including idiosyncratic, systemic and a combination of these two scenarios.

- Designing scenarios that are sufficiently severe to activate the recovery plan and test the calibration of the trigger framework and the feasibility of a range of recovery options.

- Leveraging off any existing stress testing frameworks within the risk management framework and ensuring that the scenario analysis is sufficiently robust for recovery planning purposes.

ii. Triggers and recovery options

Many insurers do not identify which triggers are breached in the scenario analysis section of the plan. This is important for assessing whether the trigger framework is effectively calibrated to escalate emerging risks in a timely manner under the different stress scenarios.

Better practice examples include:

- Detailing which metrics from the trigger framework are breached under each scenario, and at which point.

- Using the scenario analysis to explore a wider range and severity of stress events which would require more significant recovery options to be implemented, beyond just relying on the availability of capital raising recovery options.