To: All APRA-regulated entities

Poorly designed or implemented remuneration practices can incentivise behaviour that is harmful to customers and detrimental to long-term financial soundness. To enhance minimum standards for remuneration, APRA developed Prudential Standard CPS 511 Remuneration (CPS 511). At the time of finalising CPS 511, APRA committed to review implementation and publish the findings.

CPS 511 implementation review

APRA undertook the review in two phases between September 2021 and December 2022. The objective of the review was to understand how entities are approaching implementation of CPS 511. Entity compliance was not assessed since CPS 511 was not in force at the time.1

In the first phase, APRA followed the journey of 15 entities as they prepared to implement the standard.2 These were predominantly but not all Significant Financial Institutions (SFIs)3 and involved detailed assessments, including meetings with Board Remuneration Committee (RemCo) Chairs. The second phase was a light-touch, one-off survey of remaining SFIs. In both phases, APRA asked about CPS 511’s key requirements: remuneration framework, governance, design and consequence management. In total, the review covered 39 entities.

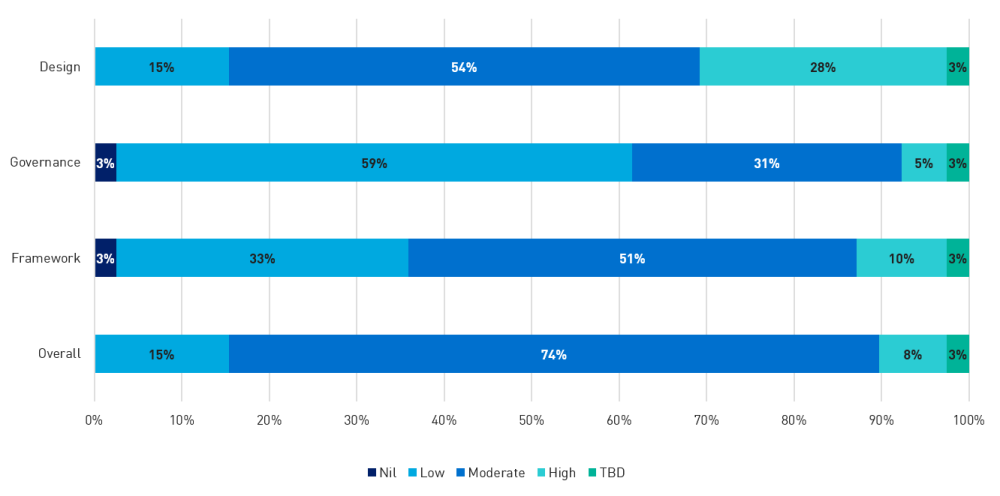

All entities were asked to rate the level of change required to implement CPS 511. Remuneration design was identified as being the area requiring the greatest uplift to existing practices, by approximately 80% of entities. By contrast, more than 60% of entities surveyed considered remuneration governance to require only a low level of change. Approximately 70% of entities rated the overall change required from implementation as moderate.

Figure 1. Key areas of change rated by review entities

Summary of findings

APRA found early signs of a step change in remuneration practices. APRA was pleased to see entity efforts to strengthen alignment of remuneration and risk management in remuneration frameworks. This was evident through inclusion of risk measures in variable remuneration design and downward-adjustment processes. Board engagement had improved across all entities, including through RemCo oversight of CPS 511 implementation.

While APRA was broadly comfortable with entities’ progress to implement CPS 511, given the timing of the review they were more focused on the design of their remuneration frameworks. To ensure sustainable change, industry should consider the following common gaps observed during the review:

- limited progress implementing controls to manage potential conflicts arising from compensation arrangements of third-party service providers;

- inadequate understanding of how selected non-financial measures (NFMs) will drive desired behaviour, risk outcomes and performance; and

- insufficient rigour in the proposed processes to ensure remuneration consequences result from poor risk management outcomes.

Once remuneration outcomes start to be determined under the new requirements, APRA will be better able to assess whether CPS 511’s key objectives have been fully satisfied. APRA’s approach to this will be risk-based, such as through prudential reviews and engagements.

Implications of review findings

While the review predominantly involved SFIs, the findings are relevant to all APRA-regulated entities. The findings are intended to support wider industry implementation, promote consistent application and clarify expectations in key areas.

Detailed observations from the review are annexed to this letter, along with hypothetical scenarios used in the review to test consequence management processes. The Annex should be read in conjunction with Prudential Practice Guide CPG 511 Remuneration (CPG 511), which sets out better practice in relation to APRA’s requirements on remuneration.

Learnings from the review will be considered for inclusion in CPG 511 in due course, subject to consultation with industry. The observations set out in the Annex do not create a present obligation on regulated entities to adhere to them but provide insight into potential future directions in APRA guidance.

Yours sincerely,

John Lonsdale

Chair

Annex – Detailed observations from CPS 511 pre-implementation review

| Framework – General observations and application to groups | Relevant paragraphs |

|---|---|

| CPS 511 requires entities to maintain a remuneration framework with clear objectives. Most entities used the CPS 511 implementation process to clarify the purpose of variable remuneration. In the review, entities that could articulate this were well-positioned to develop a sound framework. APRA found that most entities had enhanced the emphasis on risk management in remuneration frameworks. The more robust remuneration policies also reinforced the desired risk culture and described the risk functions’ role in remuneration decisions. CPS 511 requires the identification of specified roles. Many entities intended to set criteria to identify these roles, but not all had developed these criteria in detail or established processes for ongoing monitoring. Some entities were already working on how to maintain ongoing integrity of this process by establishing information systems and oversight. Entities which are the “head of a group” are required to apply CPS 511 requirements “appropriately”. APRA found local groups were generally applying CPS 511 on a group basis and considering roles in non-regulated subsidiaries and offshore arrangements that may also be subject to overseas regulations. International groups were applying CPS 511 within the context of their home jurisdiction group remuneration framework, which often required an Australian overlay to meet specific requirements. Where applicable, APRA clarified the intention that for the Senior Officer outside Australia (SOOA) of a foreign bank or insurer, CPS 511 would align to the Financial Accountability Regime (FAR). Specific CPS 511 requirements would apply to the SOOA’s variable remuneration on a pro-rata basis, based on the proportion of their overall role which is allocated to the APRA-regulated entity.4 | CPS 511: 5, 6, 8, 21, 22, 74, 75 CPG 511: 27

|

| Framework – Compensation arrangements of third-party service providers | Relevant paragraphs |

|---|---|

CPS 511 requires entities to manage material conflicts that may result from compensation arrangements of third-party service providers. This requires ongoing assessment of relevant third-party compensation arrangements, potential material conflicts and mitigating controls. Most review entities noted the high degree of effort needed to implement this requirement. APRA observed:

| CPS 511: 22c, 75c CPG 511: 37 to 40

|

| Governance – General observations and engagement with Risk | Relevant paragraphs |

|---|---|

A primary objective of CPS 511 is to strengthen board accountability, oversight and decision making on remuneration. APRA observed strengthened board engagement through RemCo oversight of the implementation process. However, APRA observed limited consideration had been given to date on how meaningful ongoing governance practices could be established, such as active board challenge to recommended remuneration outcomes. All review entities had designed a process for the RemCo to consult the Risk Committee, as required by CPS 511. Several entities already had formal engagement between the Committees in place. APRA steered others away from solely relying on verbal input or cross-committee membership. There was room for improvement in the effectiveness of this engagement in most entities. A few entities’ boards had taken the following steps:

| CPS 511: 23, 30, 49, 50, 52, 87

|

| Design – General observations and non-financial measure selection | Relevant paragraphs |

|---|---|

CPS 511 requires significant changes to the way entities design their variable remuneration arrangements and APRA observed significant uplift underway. APRA was pleased to see several review entities had assessed the overall appropriateness of their existing remuneration arrangements before considering specific design requirements. Many entities cited challenges in selecting appropriate NFMs to include in performance-related variable remuneration. The most common gap observed was a limited understanding of how NFMs were expected to produce desired behaviours, making it challenging to demonstrate appropriateness. Examples of more effective approaches included:

NFMs are expected to evolve over time. Entities recognised that as remuneration outcomes are determined under CPS 511, they will start to understand the impact of selected NFMs in achieving desired behaviours and so design of NFMs will be refined. | CPS 511: 33, 34, 78

|

| Design – Balanced incentives and achieving material weight with NFMs | Relevant paragraphs |

|---|---|

CPG 511 clarifies that the purpose of applying a material weight to NFMs is to promote a balanced approach to incentives, so that financial measures are not a dominant driver of remuneration outcomes and prudent management of risk is encouraged. To achieve this balance, CPS 511 imposes two distinct requirements: to reward positive risk outcomes based on clearly defined NFMs; and to address poor risk outcomes through the downward-adjustment process (i.e. the ‘carrot and stick’ approach). APRA found that some entities had not fully appreciated this two-pronged approach in CPS 511 and were relying on downward-adjustment tools and triggers alone to satisfy the material weight requirement. During the review, APRA explained the need to evidence both rewarding positive risk outcomes as a result of NFMs and addressing poor risk outcomes through downward-adjustment. APRA observed this resulted in entities finding it challenging to demonstrate how selected NFMs would impact remuneration outcomes and contribute to achieving material weight. However, a number of entities were showing early signs of developing sustainable practices, for example:

APRA also observed examples of prudent approaches to ensuring NFMs achieved material weight in remuneration outcomes. Some entities used an additional modifier or gateway as a lever to give stronger weight to NFMs. Others introduced principles for how to achieve material weight that set the tone for how the board wished to holistically approach NFMs. | CPS 511: 33, 34, 37, 78, 80 CPG 511: 49, 50, 59, 63 |

| Design – Deferral of variable remuneration | Relevant paragraphs |

|---|---|

CPS 511 sets a minimum benchmark for remuneration deferral practices. For entities that were deferring variable remuneration already, it has been more straightforward to implement the CPS 511 deferral requirements. Deferral was less commonly used prior to CPS 511 in superannuation, and consequently implementation was reported as more challenging. One challenge included determining the start date of the deferral period. Some superannuation entities had established annual short-term incentive plans which included member return measures that looked back over multiple years. In this situation, APRA reinforced that entities may only include one performance year in the calculation of the deferral period. If superannuation entities wish to include the whole return measurement period in the deferral period, this can be achieved using a long-term incentive plan, with return measures identified and communicated at the start of the period. Several entities were unclear about whether sign-on and buy-out awards need to be included in the calculation of total variable remuneration and are therefore subject to deferral. CPS 511 stipulates that any award that is conditional on the achievement of objectives is variable remuneration. As a result, sign-on and buy-out awards that are contingent on an individual remaining employed with the entity for a defined period, meet the variable remuneration definition. | CPS 511: 41 to 43, 78b CPG 511: 65 to 67

|

| Consequence management – General observations and robust decision-making | Relevant paragraphs |

|---|---|

To ensure entities apply consequences for poor outcomes, CPS 511 requires a process to be in place which considers whether reductions in variable remuneration are needed. Almost all review entities had made good progress on designing such a downward-adjustment process. Yet, when tested against the hypothetical consequence management scenarios APRA requested as part of the review, APRA found that downward-adjustment processes showed a lack of rigour, which could undermine consistent decision-making. Certain entities also found it challenging to demonstrate how their downward-adjustment process would robustly reflect risk outcomes and the appropriate remuneration impact for individuals. Entities with more robust approaches to designing downward-adjustment processes included some or all of the following:

Consequence management was also being achieved – especially by entities with limited or no variable remuneration – through other methods, including restrictions on fixed remuneration increases, training, coaching and performance improvement plans. | CPS 511: 33c, 37, 44, 78c, 80, 85 CPG 511: 42, 73, 76, 82

|

Consequence Management – hypothetical scenarios

- Insurance - Multiple public reports throughout the year of severely mishandled claims due to repeated instances of misinterpretation of policies by claims staff. Remediation costs expected to be in excess of $30m. Upon investigation, discovered misinterpretation related to various claims between 2015 and 2018. While individual claims staff were directly responsible for the mishandled claims, further investigation by the entity indicated this was due to inadequate training by the claims training staff at the time. Additionally, risk reporting to Head of Claims did not highlight any anomalies (nor did the Head of Claims identify any anomalies). Internal Audit also did not identify any issues during the period.

- Banking - Assurance review of a home lending portfolio identified an issue with several home loan serviceability assessments. A deeper portfolio review identified misleading serviceability assessments were supported by fraudulent documentation provided by a particular mortgage broker. A close personal relationship existed between the banker and mortgage broker, and documented processes and controls (within the Home Lending team) were not followed. To remedy, entity recreated serviceability assessments based on accurate customer information to ensure prudential standards were met. Some customers had been granted loans that they could not afford. Further customer remediation was then required with costs exceeding $10m.

- Superannuation - A material unit pricing error impacted an entity’s MySuper option. Remediation costs are estimated to be around $10m. Upon investigation, it was discovered that the unit pricing error remained undetected since 2016, and many members (both in-force and exited) have potentially been impacted. Whilst the calculation error was made by the custodian which performs a component of the unit pricing calculation as an outsourced service provider, checks and reconciliations performed by internal Investment Operations team as well as first and second line internal risk teams did not detect the error. Nor was there any escalation to the Board or Investment Committee.