Executive summary

An authorised deposit-taking institution’s (ADI's) capital base is the cornerstone of its financial soundness. Prudential Standard APS 111 Capital Adequacy (APS 111) sets out detailed criteria for measuring an ADI's Regulatory Capital. This Discussion Paper outlines a substantial update to this important Prudential Standard.

The update incorporates further technical information to assist ADIs in issuing capital instruments; recent international standards, statements and guidance on capital adequacy measures; and changes to the capital treatment of a parent ADI’s equity investments in banking and insurance subsidiaries.

Since the last significant update to APS 111 in 2013, APRA has made various rulings and published further technical information to assist ADIs with compliance, which APRA is now proposing to incorporate into the Prudential Standard. In addition, the Basel Committee on Banking Supervision (Basel Committee) has released a number of standards, statements and guidance that are relevant to the measurement and determination of Regulatory Capital. These relate to banks’ equity investments in funds, banks’ holdings of Total Loss Absorbing Capacity (TLAC) instruments and capital arbitrage transactions. APRA is proposing amendments, where appropriate, to APS 111 to incorporate these Basel proposals.

In its recent publications, APRA has also flagged a review of the capital treatment of a parent ADI’s equity investments in banking and insurance subsidiaries. This review was prompted in part by recent proposals by the Reserve Bank of New Zealand (RBNZ) to materially increase capital requirements in New Zealand. The RBNZ’s proposals and APRA’s processes are a natural by-product of both regulators working to protect their respective communities from the costs of financial instability and the regulators continue to support each other as these reforms are developed.

APRA is proposing to change the capital treatment for these exposures and this particular proposal is the most significant amendment to APS 111. In developing the proposal, APRA has considered long-established trans-Tasman arrangements provided for in the Australian Prudential Regulation Authority Act 1998 and the RBNZ’s enabling legislation, under which the agencies assist each other in the performance of their regulatory responsibilities. This is particularly important given the four major Australian banks are the shareholders of the major banks in New Zealand.

APRA's capital requirements currently permit ADIs to leverage their investments in banking and insurance subsidiaries, whether domestic or offshore, and as such do not require dollar-for-dollar capital for these investments at the parent company level. This treatment raises the risk that capital held by the parent ADI is not sufficient to support risks to its depositors. Any reforms by other regulators to materially increase their capital requirements, including those proposed by the RBNZ, could exacerbate this risk.

At current levels of equity investment, APRA estimates the existing treatment provides an uplift to the average Common Equity Tier 1 (CET1) Capital ratio across the four major Australian banks of around 100 basis points for their equity investments in New Zealand banking subsidiaries. As a consequence, capital available to support risks to Australian depositors could be overstated.

As APRA is more concerned about large concentrated exposures, it is proposing to limit the amount of the exposure to an individual subsidiary that can be leveraged to 10 per cent of an ADI’s CET1 Capital. This means capital requirements are increasing for large concentrated exposures, as amounts over the 10 per cent threshold would be required to be met dollar-for-dollar by the ADI parent company. APRA is less concerned about small equity exposures in banking and insurance subsidiaries and so capital requirements will decrease for small exposures. Amounts under the 10 per cent threshold would be risk weighted at 250 per cent and included as part of the related party limits detailed in APRA’s recently finalised Prudential Standard APS 222 Associations with Related Entities (APS 222). See Box 1 in Chapter 2 of this Discussion Paper for a stylised example of the Level 1 treatment of an investment in a banking subsidiary.

APRA has calibrated the proposed capital requirements so they are broadly consistent with the Basel treatment of a banking group’s equity investments in non-consolidated financial entities, and also with the current capital position of the four major Australian banks, in respect of these exposures (i.e. preserving most of the existing capital uplift).

APRA is not proposing a full dollar-for-dollar capital requirement for an ADI’s equity investments in these subsidiaries, in recognition of the benefits of subsidiaries that are subject to prudential regulation, and that ownership of banking and insurance subsidiaries generally provides some beneficial diversification. However, as these exposures increase in size, the concentration risk associated such investments start to outweigh the diversification benefits. Requiring dollar-for-dollar capital for amounts above 10 per cent CET1 Capital reduces the risks to Australian depositors of increasing levels of these exposures.

The finalisation of the RBNZ’s proposed capital reforms, will, in all likelihood, require higher capital requirements for banks in New Zealand. Should Australian ADIs fund higher capital requirements in New Zealand by retaining the profits of their New Zealand subsidiary banks in those subsidiaries, no material additional capital, in aggregate, is likely to be required by Australian ADIs.

Other proposed changes to APS 111 include:

- promoting simple and transparent capital issuance by removing the allowance for the use of special purpose vehicles (SPVs) and stapled security structures; and

- clarifying and simplifying various parts of APS 111, which comprise the bulk of the proposed changes.

APRA does not consider its proposal to remove the use of SPVs and stapled security structures as material as these structures have not been a feature of ADI capital issuance since 2013 and, in the case of stapled security structures, less attractive for ADIs under the Basel III capital reforms.

APS 111 is open for consultation until 31 January 2020. APRA intends to finalise the changes to the Prudential Standard in early 2020 with the updated Prudential Standard to come into force from 1 January 2021. APRA is open to working with impacted ADIs on appropriate transition.

Glossary

ADI | Authorised deposit-taking institution |

Additional Tier 1 Capital | Capital instruments that provide loss-absorption while the ADI remains a going concern, but do not satisfy all of the criteria for inclusion in CET1 Capital. |

APRA | Australian Prudential Regulation Authority |

APS 110 | Prudential Standard APS 110 Capital Adequacy |

APS 111 | Prudential Standard APS 111 Capital Adequacy: Measurement of Capital |

Basel Committee | Basel Committee on Banking Supervision |

Basel III | A series of revisions to the Basel capital framework following the global financial crisis that commenced with the Basel Committee’s Basel III: A global regulatory framework for more resilient banks and banking systems, December 2010 (revised June 2011). |

CET1 Capital | Common Equity Tier 1 Capital. The highest quality component of capital. It is subordinated to all other elements of funding, absorbs losses as and when they occur, has full flexibility of dividend payments and has no maturity date. |

Level 1 | The ADI itself or the Extended Licensed Entity. |

Level 2 | The consolidation of the ADI and all its subsidiaries other than non-consolidated subsidiaries; or if the ADI is a subsidiary of a non-operating holding company (NOHC), the consolidation of the immediate parent NOHC and all the immediate parent NOHC’s subsidiaries (including any ADIs and their subsidiaries) other than non-consolidated subsidiaries. |

Mutual equity interests | Capital instruments issued by mutually-owned ADIs that meet the definition of CET1 Capital. |

Regulatory Capital | Consists of Tier 1 Capital and Tier 2 Capital. |

Tier 1 Capital | The sum of the components of CET1 Capital, Additional Tier 1 Capital, and eligible Mutual Equity Interests that is in excess of the limit for recognition as CET1 Capital. |

Tier 2 Capital | Other components of Regulatory Capital that, to varying degrees, fall short of the quality of Tier 1 Capital but nonetheless contribute to the overall strength of an ADI and its capacity to absorb losses. |

TLAC | Financial Stability Board (FSB) standard for Total Loss Absorbing Capacity, November 2015. The FSB’s TLAC Term Sheet sets out eligibility criteria for TLAC-eligible instruments. For the purpose of the deducting these holdings from Tier 2 Capital, TLAC holdings include: all direct, indirect and synthetic holdings of external TLAC; all instruments ranking pari passu with subordinated forms of TLAC; and excludes all holdings of instruments or other claims listed in the “Excluded Liabilities” section of the FSB TLAC Term Sheet. |

Chapter 1 - Introduction

1.1 Background

APS 111 requires an instrument to have certain characteristics to qualify as Regulatory Capital for an ADI and requires an ADI to make various deductions to determine total Regulatory Capital on both a Level 1 and Level 2 basis.

The key requirements of APS 111 are that an ADI must:

- include in the appropriate category of Regulatory Capital only those capital instruments that meet the detailed criteria for that category;

- ensure all Regulatory Capital instruments are capable of bearing loss on either a ‘going-concern’ basis (Tier 1 Capital) or a ‘gone-concern’ basis (Tier 2 Capital); and

- make certain deductions to capital, mainly from Common Equity Tier 1 (CET1) Capital, to determine total Regulatory Capital.

While Prudential Standard APS 110 Capital Adequacy (APS 110) sets out the minimum capital adequacy measures required by APRA, APS 111 provides the detail of the components of those capital adequacy measures. Certainty and comparability are key elements in the measurement and assessment of capital adequacy across all ADIs.

APS 111 has not significantly changed since 2013 when the Prudential Standard was updated for the Basel III capital reforms. These changes included more detailed criteria for the inclusion of capital instruments in CET1 Capital, Additional Tier 1 Capital (AT1 Capital) and Tier 2 Capital. APRA made minor updates to APS 111 in 2014 and 2017 to allow firstly, mutually owned ADIs to issue AT1 Capital and Tier 2 Capital instruments that provide for conversion into mutual equity interests (MEIs) and secondly, to allow mutually owned ADIs to directly issue MEIs by establishing criteria that must be met for these instruments to be eligible for inclusion in CET1 Capital.

Over time, APRA have provided a number of rulings relating to APS 111 and some of these rulings have addressed a lack of clarity in the content of the Prudential Standard. APRA has also published frequently asked questions (FAQs) to provide further information to assist ADIs in the interpretation of APS 111 with respect to the requirements for AT1 Capital instruments, Tier 2 Capital instruments, and MEIs.1

In addition, the Basel Committee has released standards and statements relating to banks' equity investments in funds and banks’ investments in TLAC instruments and capital arbitrage transactions.2 The Basel Committee has also published FAQs in regard to the Basel III definition of capital.3

APRA is reviewing APS 111 in line with these developments and with the intention of clarifying and simplifying the standard, where appropriate.

As part of this review of APS 111, APRA is also proposing a change to the treatment of a parent ADI’s equity investments in banking and insurance subsidiaries. A long-standing principle underlying APRA’s capital framework has been that an ADI’s equity investments be supported by CET1 Capital deductions, reflecting that equity risk should be borne by shareholders rather than depositors or other creditors. A variant to this principle is at the parent ADI level whereby APRA currently allows ADIs to leverage their investments in banking and insurance subsidiaries. APRA is proposing to amend the current policy by limiting the amount of equity exposures in banking and insurance subsidiaries that can be leveraged to 10 per cent of an ADI’s CET1 Capital. Amounts over the 10 per cent threshold would be required to be deducted from CET1 Capital.

1.2 Balancing APRA’s objectives

Financial safety | Financial system stability |

|---|---|

| Improved: The proposed changes to the Prudential Standard are expected to improve financial safety. The proposed changes to the capital treatment of equity investments in banking and insurance subsidiaries reinforces ‘unquestionably strong’ capital targets at Level 1. | Improved: The proposed changes to the Prudential Standard are expected to improve financial system stability. The proposed changes promote certainty, and comparability which are key elements in the measurement and assessment of capital adequacy across all ADIs. |

Efficiency | Improved: The proposed changes to the Prudential Standard are expected to improve efficiency. The proposed changes are expected to provide greater clarity for ADIs. The proposed changes to the requirements for disclosure and marketing of capital instruments are expected to improve the transparency of these instruments, and assist in their issuance. |

|---|---|

Competition | The impact of the proposed changes to the Prudential Standard on competition is expected to be neutral. All ADIs, regardless of size, are subject to the same criteria for which the capital instruments they issue must meet to qualify as Regulatory Capital and the various deductions to be made to determine total Regulatory Capital. Clarifications associated with these criteria are the bulk of the proposed changes to the Prudential Standard and are not expected to impact competition. APRA’s proposal for the capital treatment of a parent ADI’s equity investments in banking and insurance subsidiaries is not expected to disadvantage small ADIs compared to large ADIs. For ADIs that hold small equity investments in banking and insurance subsidiaries, APRA’s proposals will reduce capital costs. However, ADIs that have large concentrated equity investments in banking and insurance subsidiaries will have increased capital costs and are likely to be disadvantaged. That said, the proposal is only likely to result in increased capital costs for a small number of large ADIs. These large ADIs may address increased capital costs a number of ways, including restructuring their business or reducing their exposure and would have flexibility in managing their capital in response to the proposal, including increasing retained earnings. Should a strategic response to an increase in capital costs be to divest part or all of their affected subsidiaries, then affected ADIs may become more concentrated, potentially reducing revenue diversity. That said, higher capital costs associated with the proposals are unlikely to affect particular product markets or competition as a whole as there is no direct linkage between the increased capital costs and any particular portfolio or product. The costs of an ADI monitoring and complying with the proposed changes will have no impact on competition. All ADIs would have existing systems and data to monitor exposure levels and capital requirements. Capital compliance costs primarily relate to performing an alternative capital calculation and are considered immaterial. |

Contestability | No change. The proposed changes to the Prudential Standard has no impact on the ability of new entrants to enter the banking industry. |

Competitive neutrality | No change. The proposed changes to the Prudential Standard does not create advantage for public sector entities relative to other market participants.4 |

1.3 Timetable and next steps

APRA intends to finalise the changes to the Prudential Standard in early 2020, with the requirements expected to come into force from 1 January 2021.

Chapter one footnotes:

1 APRA Measurement of capital - frequently asked questions, updated June 2019.

2 Basel Committee Capital requirements for banks' equity investments in funds, December 2013, Basel Committee TLAC holdings standard, October 2016, and Basel Committee Statement on capital arbitrage transactions, June 2016.

3 Basel Committee, Basel III definition of capital – Frequently asked questions September 2017 (update of FAQs published in December 2011).

4 APRA has previously interpreted the objective of competitive neutrality as ensuring consistency in the treatment of classes or types of institutions. To ensure alignment with Parliament’s original intention, APRA now follows the more common usage of this term (for example, as found in the Commonwealth Competitive Neutrality Policy Statement). Ensuring consistency in regulatory treatment now falls within the competition objective.

Chapter 2 - Proposed policy changes to APS 111

2.1 Level 1 treatment of equity investments in prudentially regulated subsidiaries

In its June 2019 Response to Submissions Paper, Revisions to the capital framework for authorised deposit-taking institutions and August 2019 Response to Submissions Paper, Revisions to the related entities framework for ADIs, APRA flagged a review of the existing approach to risk-weighting an ADI’s equity investments in other ADIs and equivalent overseas deposit-taking institutions and insurance subsidiaries at Level 1.5,6

APS 111 provides a long-standing treatment which allows an ADI at Level 1 to risk weight, after deduction of any intangibles component, at 300 per cent (if the subsidiary is listed) or 400 per cent (if the subsidiary is unlisted), its equity investments in banking and insurance subsidiaries.7 This is a variant to APRA’s general capital treatment of equity exposures, which are required to be deducted from CET1 Capital.

The current treatment recognises, in part, that an intra-group equity investment in a prudentially regulated subsidiary, usually offshore, may warrant a favourable capital treatment compared to a full capital deduction, as a prudentially regulated subsidiary could represent lower risk to the parent ADI compared to a non-prudentially regulated subsidiary. Equity investments in banking and insurance subsidiaries may also provide the parent ADI with more diverse revenue streams.

However, departure from the general capital treatment of deduction for an equity exposure must be weighed against having appropriate levels of capital available to protect the parent ADI’s depositors. In measuring Regulatory Capital at the parent ADI level, the existing risk weights applied to these exposures provide an incentive for an ADI to support these investments with debt, allowing the equity investment to be levered. This has the effect of overstating capital available at the parent ADI level.

To address this issue, APRA is proposing to limit the extent to which an ADI may use debt to fund these exposures. ADIs, at Level 1, will be required to deduct these equity investments from CET1 Capital, but only to the extent the investment in the subsidiary is in excess of 10 per cent of CET1 Capital. An ADI may risk weight the investment, after deduction of any intangibles component, at 250 per cent to the extent the investment is below this 10 per cent threshold. The amount of the exposure that is risk weighted would be included as part of the related party limits detailed in the recently finalised APS 222.8

In proposing this capital treatment, APRA is less concerned about small equity investments in banking and insurance subsidiaries and more concerned about large concentrated equity investments. For ADIs whose investments in banking and insurance subsidiaries are currently below 10 per cent of CET1 Capital, the proposal will likely provide a capital uplift as the risk weight for equity exposures under the threshold will reduce from 400 per cent currently to 250 per cent. However, for ADIs that have large concentrated exposures, there is likely a requirement to hold more capital.

APRA has considered, but is not proposing, a full deduction of equity investments in banking and insurance subsidiaries. The existing treatment is long-standing, recognises the benefits of subsidiaries that are subject to prudential regulation, and recognises that ownership of banking and insurance subsidiaries generally provides some beneficial diversification to ADIs and therefore may have a positive effect on financial safety and stability. Should a strategic response (to a full deduction) be to divest part or all of their subsidiaries, ADIs may become more concentrated, potentially reducing revenue diversity and viable recovery options in a domestic stress event.

In proposing this change to the existing treatment, APRA has considered the impact of the proposals, particularly on the four major Australian banks’ investments in their New Zealand banking subsidiaries, which are material from both a business and capital perspective. At current levels of the equity investments, APRA estimates the existing treatment to allow risk-weighting rather than deduction provides an uplift to the average CET1 Capital ratio across the four major banks of around 100 basis points.

Based on data available to APRA and at an industry level, the impact of the proposed treatment is limited and that capital requirements remain, in aggregate, consistent with APRA’s intent under the ‘unquestionably strong’ framework. The capital outcome does, however, vary for individual ADIs, with a relatively larger impact on those ADIs invested relatively more in offshore subsidiaries compared to more domestically focused peers. Notwithstanding, reforms to strengthen capital in offshore subsidiaries by other regulators, including the implementation of the RBNZ’s proposed capital reforms, could require a substantial amount of additional capital beyond APRA’s unquestionably strong benchmarks.

APRA considers that its proposal balances the issues noted above with the objective of ensuring sufficient capital is held against the business of the ADI to support risks to Australian depositors. Importantly, the proposal ensures that APRA’s ‘unquestionably strong’ framework applies at both the ADI (Level 1) and consolidated group (Level 2) levels, consistent with APRA’s original intent.

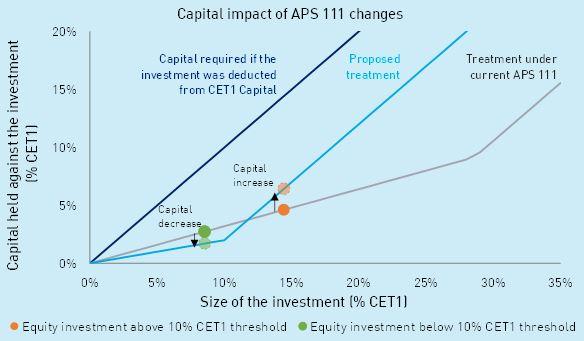

This box sets out a stylised example of the capital treatment of an ADI’s investment in a prudentially regulated banking subsidiary and the impact of the proposed 10 per cent CET1 threshold for a given level of equity investment in the subsidiary. The diagram outlines the boundaries between a full deduction approach (dark blue line), the current treatment (grey line) and the treatment proposed in this Discussion Paper (light blue line). These represent the boundaries that balance the size of the investment with the capital required under the limits in APRA’s prudential framework for equity investments (APS 111) and related entities (APS 222). A full deduction approach will result in dollar-for-dollar capital for this investment, regardless of the size of the investment. The treatment under the current APS 111 is a 300 per cent (if the subsidiary is unlisted) or 400 per cent (if the subsidiary is unlisted) risk weight for this investment. The proposed treatment in this Discussion Paper for this investment will depend on the size of the investment; for an equity investment below 10 per cent CET1 Capital, the investment is risk weighted at 250 per cent, with amounts above the 10 per cent CET1 Capital threshold deducted from CET1 Capital. Under the proposed treatment, capital requirements are decreasing for small exposures and increasing for large concentrated exposures.

|

2.2 TLAC holdings

Total Loss Absorbing Capacity (TLAC) is an international standard which was finalised by the Financial Stability Board (FSB) in November 2015.9 The objective of the standard is to ensure that banks have enough equity capital and bail-in debt to transfer losses to investors and minimise the risk of a government bailout.

The Basel Committee recently finalised its treatment of banks' investments in other banks' TLAC instruments.10 The main elements of the Basel framework are as follows:

- Tier 2 Capital deduction: banks must deduct their holdings of other banks' TLAC instruments from their own Tier 2 Capital. This would include instruments commonly referred to as ‘Tier 3’ issued by offshore banks;

- extension of the threshold approach to TLAC instruments, below which no deduction is required: banks are allowed to risk weight at 250 per cent the aggregate amount of their holdings of TLAC instruments issued by other banks below 10 per cent of their CET1 Capital with amounts above the threshold deducted; and

- instruments ranking pari passu with TLAC instruments must also be deducted from Tier 2 Capital.

The Basel framework aims to reduce the risk of contagion within the financial system should a bank enter resolution.

APRA agrees that the deduction approach reduces a potential source of contagion in the banking system. Without deduction of TLAC holdings across banks, the failure of one bank could lead to a reduction in the loss absorbency and recapitalisation capacity of another bank. Deducting TLAC holdings from Tier 2 Capital provides sufficient disincentive for ADIs to invest in other banks' TLAC instruments.

Accordingly, APRA proposes a full deduction of TLAC exposures and pari passu instruments from Tier 2 Capital. A full deduction is consistent with APRA’s existing approach to an ADI’s holdings of another ADI’s, or their own, regulatory capital instruments. APRA’s proposal adopts the Basel framework of requiring a Tier 2 deduction of TLAC instruments, but does not adopt a threshold approach.

International developments in regard to TLAC instruments have been guided by the principles outlined in the FSB’s TLAC standard. Notwithstanding, a number of different TLAC regimes have emerged globally. For the purpose of the deduction, APRA is proposing that TLAC instruments include, but are not limited to, any facility or instrument accepted by regulators, financial markets and creditors as a TLAC instrument.

2.3 Simplicity and transparency of capital instruments

As a general principle, the features of a capital instrument included as a component of Regulatory Capital, and the structure under which such an instrument is issued, should be transparent and capable of being readily understood by investors.

Provisions in the existing APS 111 rule instruments ineligible for inclusion in Regulatory Capital if the nature or complexity of their terms and conditions, location of issue, or their structure raises concerns over whether the instruments fully, and unequivocally, satisfy the requirements for Regulatory Capital.

These provisions in the existing APS 111 apply only to the use of special purpose vehicles (SPVs). APRA is proposing to remove the relevant Attachment in the existing APS 111 on the use of SPVs (see 2.4 below).

Notwithstanding the proposals in regard to the use of SPVs, APRA considers that it is appropriate that these existing provisions should apply to all issues of capital instruments and thus these requirements have been retained in the Prudential Standard to apply broadly.

2.4 Use of special purpose vehicles and stapled security structures

Under the existing APS 111, an ADI may issue a capital instrument through an SPV, subject to certain criteria. A stapled security structure consisting of the issue of a preference share and a stapled instrument of another form may also be included in AT1 Capital, subject to satisfying additional criteria.

In line with the objective of simplifying APS 111 and ensuring that capital instruments are transparent and capable of being readily understood, APRA is proposing to amend APS 111 so that capital instruments involving SPVs and stapled security structures are not recognised for capital adequacy purposes.

APRA understands these structures may be less attractive for ADIs (and investors) due to their complexity, and in the case of stapled securities, their reduced tax effectiveness. The use of SPVs and stapled security structures also increases complexity in regard to loss absorption and non-viability provisions included in APS 111.

The use of SPVs to issue capital instruments and stapled security structures have not been a feature of ADI capital issuance since 2013, when APS 111 was updated for the Basel III capital reforms. Prior to Basel III, the difference in limits for inclusion in Tier 1 Capital favoured the use of non-innovative capital such as stapled securities. Under Basel III, this incentive no longer applies.

APRA understands there are no existing Basel III capital instruments issued by ADIs involving SPVs and stapled security structures. Capital instruments involving SPVs and stapled security structures issued prior to 1 January 2013, where the ADI had obtained APRA’s approval for transition, remain eligible for this transition under the revised APS 111.

2.5 Use of fair values

The use of fair values, together with experiences from the global financial crisis, have emphasised the critical importance of robust risk management and control processes around fair value measurements.

The existing APS 111 requires an ADI to notify APRA promptly whenever there is a material reclassification by the ADI of financial assets and liabilities from amortised cost to fair values or from fair values to amortised cost.

APRA is proposing to include a further requirement in APS 111 for an ADI to notify APRA whenever there is a material change in the systems and controls used for valuation purposes; valuation methodologies; and valuation adjustments employed to produce fair values of financial instruments.

APRA is also proposing that the use of fair values is specifically addressed as part of the internal or external audit review of the ADI’s risk management framework under Prudential Standard CPS 220 Risk Management (CPS 220), including in the internal audit review of the implementation of policies and procedures for producing fair values and their use.

Chapter 2 footnotes

5 APRA Response to Submissions, Revisions to the capital framework for authorised deposit-taking institutions, June 2019.

6 APRA Response to Submissions Paper, Revisions to the related entities framework for ADIs, August 2019.

7 An ‘equivalent overseas deposit-taking institution’ refers to an overseas financial institution that is subject to equivalent minimum prudential standards and level of supervision as an ADI.

8 APRA Response to Submissions Revisions to the related entities framework for ADIs, August 2019.

9 FSB, Total Loss-Absorbing Capacity (TLAC) Principles and Term Sheet, November 2015.

10 Basel Committee TLAC holdings standard, October 2016.

Chapter 3 - Other policy issues

3.1 Equity investments in funds management vehicles

The Basel Committee has revised its framework for the treatment of banks' investments in the equity of funds management vehicles. The revised framework applies to equity investments in all types of funds including hedge funds, managed funds and investment funds.

The revised Basel framework includes a hierarchy of approaches for calculating capital requirements for equity investments in funds management vehicles:

- ‘look-through approach’, where banks apply the risk weights of the fund’s underlying exposures as if the exposures were held directly by the bank;

- ‘mandate-based approach’, where banks assign risk weights on the basis of the information contained in a fund’s mandate or in relevant legislation governing the funds; and

- ‘fall back approach’, where banks assign a 1250 per cent risk weight to their equity investments in funds.

The Basel framework also applies a leverage adjustment to the risk-weighted assets derived from the above approaches to appropriately reflect a fund’s leverage.

While a ‘look-through’ approach or a ‘mandate-based’ approach may provide incentives for ADIs to enhance their risk management of their investments, the approaches introduce significant complexity and may present operational challenges for ADIs.

APS 111 currently requires an ADI’s equity investment in funds management vehicles to be deducted from CET1 Capital. This reflects APRA’s long-standing policy to deduct from regulatory capital most equity holdings and other capital support provided by ADIs, based on the principle that equity risk should be borne by shareholders rather than depositors. In the instance of an ADI’s equity investments in funds management vehicles, this treatment also reflects the potential risk of a fund’s underlying investments, including where the fund’s holdings are not sufficiently transparent, are illiquid or the fund itself is highly leveraged, and that funds management does not generally constitute banking business.

APRA proposes not to adopt the Basel framework in this regard and instead retain the current deduction approach to equity investments in funds management vehicles. This proposal does not necessitate a change to the existing APS 111.

Further, APRA is not proposing a change to Prudential Standard APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk (APS 113) in regard to equity investments that are structured with the intent of conveying the economic substance of debt. Such investments are not required to be treated as equity exposures.

3.2 Capital arbitrage transactions

Over time, APRA has received requests to review or approve transactions (e.g. credit derivatives, guarantees), that seek to alter the form or substance of items subject to deduction. In APRA’s view these transactions can have the effect of overestimating eligible capital, without commensurately reducing the risk in the financial system.

Consistent with the Basel Committee’s statement on capital arbitrage transactions, it is APRA’s long-standing policy that transactions that have the aim of offsetting deductions are not recognised for capital adequacy purposes. APRA is proposing to make this explicit in APS 111.

3.3 Cross default clauses

The existing APS 111 requires that, in relation to AT1 Capital and Tier 2 Capital instruments, there must be no cross-default clauses in the documentation of any debt or other capital instrument of the issuer linking the issuer’s obligations under the AT1 Capital and Tier 2 Capital instrument to default by the issuer under any of its other obligations, or default by another party, related or otherwise.

APRA proposes to clarify in APS 111 that this restriction extends to event of default clauses specifying any acts/events/consequences arising in relation to an AT1 Capital or Tier 2 Capital instrument that would trigger default under the debt or other capital instrument. This clarification reflects APRA’s current assessment approach, which has been applied over recent years, when assessing capital instrument proposals.

Taken as a whole, this proposal would restrict any clause triggering default by the issuer upon any of the following events occurring:

- breach of obligations (e.g. non-payment) and consequences of, or actions to prevent a breach (e.g. enforcement of a judgement for debt, moratoriums or arrangements with creditors);

- material adverse change clauses (e.g. an event which the lender believes could affect the ability or willingness of the issuer to repay); and

- discretionary actions.

This clarification reflects the importance of capital being available to support an ADI’s financial position. Such support would be detrimentally affected if an adverse event relating to the capital instrument could trigger a default on other instruments.

APRA is also proposing to clarify that the restriction also means that an AT1 Capital or Tier 2 Capital instrument itself must not include clauses that would trigger default by the issuer upon the occurrence of the events referred to above in relation to any of the issuer’s debt or other capital instruments.

APRA is further proposing that, in applying the prohibition, other debt instruments and capital instruments which were issued or drawn prior to the revised draft Prudential Standard being published will be excluded, reflecting the impracticality of having those instruments amended. Any new issue or drawing from this date would need to meet these requirements.

3.4 Funding of capital instruments

The criteria for an instrument to be classified as Regulatory Capital includes a requirement that the issuer, any other member of a group to which the issuer belongs, or any related entity, cannot have purchased or directly or indirectly funded the purchase of the instrument.

APRA is proposing to clarify in the Prudential Standard that where the capital instruments of an ADI are used as collateral for a margin lending exposure, and the ADI has full recourse to the borrower for the margin loan, it is not required to deduct the capital instruments from the corresponding category of Regulatory Capital.

For the purposes of the Prudential Standard, lending to a borrower on a non-recourse basis secured against any capital instruments is to be treated as an indirect funding of the capital instruments.

3.5 Intra-group capital transactions

To improve transparency, APRA is proposing to include in APS 111 more detail of the matters APRA will consider in assessing the overall strength of Level 1 and Level 2 capital adequacy.

This would include, for example, the inability to extract capital from group members which may impact on the capital position of an ADI as head of a group (i.e. the Level 1 capital position). If capital cannot be extracted from other group members it may need to come from the parent ADI itself thereby undermining its capital position. The potential for such an outcome needs to be considered in assessing the capital position of the ADI.

APRA is also proposing to include in the Prudential Standard a specific requirement that an ADI must deduct from CET1 Capital, at Level 1 and Level 2, an amount to capture any capital support which APRA assesses might potentially be needed to support individual group members of a group to which an ADI belongs.

3.6 Minority interest and other capital issued out of fully consolidated subsidiaries held by third parties

Where an ADI is a subsidiary of a non-operating holding company (NOHC) which heads a Level 2 group, capital instruments issued by an ADI subsidiary to third parties are subject to the provisions in the Prudential Standard relating to minority interest.

APRA is proposing to clarify in the Prudential Standard that this requirement does not apply where a NOHC owns 100 per cent of, and its sole direct investment is in, the ADI subsidiary.

In the event the NOHC holds investments in other entities (whether in the Level 2 group or a wider group), the capital instruments issued by the ADI subsidiary to third parties are subject, at Level 2, to the minority interest provisions of the Prudential Standard. This reflects the fact that capital raised by the ADI subsidiary in these circumstances is not available for general usage by the group.

APRA is also proposing to clarify in the Prudential Standard that a fully consolidated subsidiary does not have to be a wholly owned subsidiary.

3.7 Documentation and statement of compliance

Under the existing APS 111, ADIs must provide copies of relevant documentation associated with the issue of AT1 Capital and Tier 2 Capital instruments. Where the terms of a capital instrument depart from established precedent, an ADI must consult with APRA on the eligibility of the instrument in advance of the issuance of the instrument, and provide APRA with all the documentation it requires to assess its eligibility.

APRA is proposing to extend the requirement to provide relevant issue documentation to CET1 Capital instruments.

To further assist APRA’s assessment of all capital instruments, APRA is also proposing to include in the Prudential Standard a requirement for a statement of compliance which is expected to:

- address each required capital eligibility criterion set out in the Prudential Standard; and

- clearly set out references to supporting documents and opinions.

A senior manager of the ADI will be required to sign the statement of compliance, acknowledging responsibility for the assessment.

3.8 Disclosure and marketing of capital instruments

The existing APS 111 does not provide for a consistent disclosure regime across capital instruments.

APRA is proposing to apply disclosure requirements in the Prudential Standard that are common across instruments but tailored to each form of capital instrument as appropriate. A consistent disclosure regime also makes clear that, for the large part, AT1 Capital instruments, Tier 2 Capital instruments and MEIs are subject to similar disclosure regimes.

In addition, APRA is proposing to apply a consistent reference to marketing across all forms of capital instruments, including ordinary shares. Where documentation, marketing of an instrument, or any ongoing dealings with investors in the instrument, suggest the instrument has attributes not consistent with the eligibility requirements in the Prudential Standard, the instrument will be ineligible to be included in Regulatory Capital.

3.9 Notification to APRA

The existing APS 111 requires an ADI to notify APRA immediately, when its Level 1 or Level 2 CET1 Capital ratio falls to or below 5.125 per cent of total risk weighted assets.

APRA is proposing to extend this requirement so that an ADI is required to notify APRA if it anticipates the CET1 Capital ratio falling below 5.125 per cent of total risk weighted assets. This also applies in the case of a fully consolidated subsidiary in the Level 2 group which may be exposed to the occurrence of a non-viability event imposed on it by a host regulator or by statute; or a foreign bank owned locally-incorporated ADI subsidiary subject to a non-viability event imposed by a home regulator or statute upon its foreign bank parent or group.

3.10 Other clarifications to APS 111

Table 1 sets out other minor clarifications to APS 111. These items, for the most part, do not seek to implement any change in policy but rather seek to clarify or make certain existing requirements in the Prudential Standard.

Table 1: Other clarifications to APS 111

Issue | Existing APS 111 | Proposed clarification to APS 111 |

Fee income | Current year earnings include the full value of upfront fee income, subject to certain criteria. | Reference to upfront fee income has been removed. This is to make clear that all forms of fee income, whether received or future income, may be included in current year and retained earnings, subject to certain criteria. |

Accumulated other comprehensive income and other disclosed reserves | Reserves from equity-settled share-based payments granted to employees as part of their remuneration package may be included in accumulated other comprehensive income and other disclosed reserves. | The amount of the reserve must be matched by an equivalent charge to profit or loss of the ADI for expensing the future issue of, or funding of the acquisition of ordinary shares by, employees. |

Deferred tax assets and deferred tax liabilities | An ADI must deduct from its CET1 Capital the net amount of its deferred tax assets less deferred tax liabilities. | For the purposes of this calculation, deferred tax liabilities and deferred tax assets must exclude amounts that have been netted in calculating goodwill and intangible assets and defined benefit superannuation assets. |

Gains and losses arising from changes in own creditworthiness | An ADI must eliminate from CET1 Capital all unrealised gains and losses that have resulted from changes in the fair value of liabilities (including capital instruments), due to changes in the ADI’s own creditworthiness. | All unrealised gains and losses in this regard include any adjustments to the value of liabilities and any associated embedded derivatives, where the adjustment is related to changes in the ADI’s own creditworthiness. |

Paid-up | Capital instruments must be paid-up and the amount must be irrevocably received by the issuer. | Paid up means the capital/payment has been received with finality by the issuer, is reliably valued, fully under the issuer’s control and does not, directly or indirectly, expose the issuer to the credit risk of an investor. |

Ordinary shares | To be classified as paid-up ordinary shares in CET1 Capital, an instrument must satisfy certain criteria. | The instrument must also be the only class of ordinary share, except for the distinction between voting and non-voting ordinary shares. Non-voting ordinary shares must be identical to voting ordinary shares of the issuer in all respects except the absence of voting rights. |

Distributable items | Distributions on ordinary shares, AT1 Capital and MEIs are paid out of distributable items (retained earnings included) of the issuer. | Distributable items are those items which are permitted to be distributed in accordance with relevant statutory and regulatory requirements applicable to distributions by an issuer. |

Recapitalisation of issuer | AT1 Capital and Tier 2 Capital instruments must have no features that hinder recapitalisation of the issuer, or any other members of the group to which the issuer belongs. | All capital instruments must have no features that hinder recapitalisation of the issuer, or any other members of the group to which the issuer belongs. |

Perpetual instruments | The principal amount of an AT1 Capital instrument is required to be perpetual (i.e. it has no maturity date). | Instruments with maturity dates and automatic roll-over features are not considered perpetual instruments. |

Payments/distributions | An issuer must have full discretion at all times to cancel payments/distributions on an AT1 Capital instrument. Limits on the use of dividend stoppers within AT1 Capital instruments. | An AT1 Capital instrument must not provide for investors upon non-payment of a distribution to convert an AT1 Capital instrument, and the amount of any unpaid dividend or interest, into ordinary shares or MEIs. Any restriction on the payment of distributions, or any restriction on redemptions or buybacks of CET1 Capital instruments, cannot apply to any existing holding company of the issuer, or any potential future holding company of the issuer, where the holding company does not undertake the role of issuer of the instrument. |

Maturity of instruments | The principal amount of a Tier 2 Capital instrument must have a minimum maturity of at least five years.

| Where a Tier 2 Capital instrument has a defined maturity and provides for a mandatory roll-over, the maturity of the instrument is deemed to only extend to the date upon which any roll-over may take effect. |

Optional redemption | In relation to AT1 Capital or Tier 2 Capital instruments, early redemption is permitted in certain circumstances. | When a loss absorption trigger point is reached (AT1 Capital) or a non-viability trigger event occurs (AT1 Capital or Tier 2 Capital), the loss absorption or non-viability provisions must operate without regard to any notification of early redemption. |

Incentives to redeem | AT1 Capital and Tier 2 Capital instruments must not contain step-ups in interest rates or other incentives to redeem. | Additional examples of incentives to redeem include mandatory conversions and options for investors to require a conversion and minimum and maximum interest rates on distributions. |

Taxation or regulatory events | AT1 Capital or Tier 2 Capital instruments may only provide for a call within the first five years of issuance as a result of a tax or regulatory event. | A tax or regulatory event, after which an instrument may be called, is confined to certain changes in law; related to the specific instrument and jurisdictions relevant to the instrument; not anticipated at the time of issue; and a consequence of an adverse impact on the issuer of the instrument. |

Conversion into ordinary shares | The conversion formula must be fixed in the issue documentation of the capital instrument. | The conversion number must be capable of being ascertained immediately, objectively and without further steps. Issue documentation must specify the financial accounts which will be used unequivocally to determine, at the point of conversion, the book value to be utilised. In calculating the ordinary share price at time of issue, adjustments may be made for ordinary share splits, bonus issues and share consolidations. For instruments which are, or may be, issued in foreign currency, the method for determining the exchange rate at relevant times must be clear in issue documentation. For mutually-owned ADIs, conversion provisions have been included in APS 111 for AT1 Capital and Tier 2 Capital instruments which can convert specifically into MEIs. |

Immediate conversion or write-off | Immediate conversion or write-off must occur when the ADI reaches a loss absorption trigger point or when the ADI is notified that APRA considers it would become non-viable. | The capital instrument must enable conversion or write-off to occur at any time of the day and on a day that is not a business day. |

Hierarchy of conversion or write-off | Issue documentation may provide, upon a loss absorption event (ATI Capital) and a loss absorption event at the point of non-viability (AT1 Capital and Tier 2 Capital), a hierarchy of conversion or write-off. | Any ranking must also provide for all AT1 Capital to be fully converted or written-off before any Tier 2 Capital are required to be converted or written-off. Any conversion or write-off of Tier 2 Capital instruments will only be necessary to the extent that conversion or write-off of AT1 Capital is insufficient to permit a declaration that a non-viability event ceases to apply. |

Amounts converted or written off | The amount of an instrument to be converted into ordinary shares or written off is the face value of the instrument, excluding any declared but unpaid dividends and accrued and unpaid interest. | The amount to be converted or written off is the face value of the instrument. Dividends and interest associated with the instrument which has been converted or written off, but which are not yet due and payable must also be extinguished. The aggregate amount of full or partial conversion or write-off must, as a minimum, be no less than the amount required to ensure the loss absorption event no longer applies; or the principal amount of all the instruments. Once a loss absorption event ceases to apply, no further conversion or write-off need be undertaken. |

Non-viability event | AT1 Capital and Tier 2 Capital instruments may also be subject to non-viability trigger events imposed by a home or host regulator in relation to instruments issued by a fully consolidated overseas subsidiary of an ADI and in relation to instruments issued by a locally incorporated subsidiary ADI of a foreign bank. | A non-viability event applicable to a parent ADI must function as a non-viability event for a subsidiary itself for AT1 Capital and Tier 2 Capital instruments it issues. A fully consolidated subsidiary incorporated overseas may, however, also be subject to non-viability requirements imposed by a host regulator. The implementation of such non-viability requirements upon the overseas incorporated subsidiary must not, however, serve as a loss absorption event for a parent ADI. A non-viability event applicable to a parent foreign bank, or to the group to which a foreign bank owned locally-incorporated ADI subsidiary belongs, may function as a non-viability event for the subsidiary itself for AT1 Capital or Tier 2 Capital instruments it issues. A locally-incorporated ADI subsidiary of a foreign bank would also disclose for AT1 Capital and Tier 2 Capital instruments it issues that such instruments are subject to potential loss as a result of home regulatory provisions. If a non-viability event occurs as a result of only host or home regulator or statutory non-viability requirements, the amount of conversion or write-off of AT1 Capital or Tier 2 Capital instruments issued by a fully consolidated overseas subsidiary of an ADI, or by a foreign bank owned locally incorporated ADI subsidiary, is determined by the relevant host or home regulator or statutory requirements. |

MEIs | There are no preferential distributions, including in respect of other elements classified as CET1 Capital. | MEIs involve preferential distributions and thus the existing APS 111 reference to non-preferential distributions is not applicable to MEIs. For MEIs, the principal amount is perpetual and is never repaid outside liquidation (other than discretionary repurchases subject to APRA’s approval). |

Chapter 4 - Consultation

4.1 Request for submissions

APRA invites written submissions on the proposals set out in this Discussion Paper.

Written submissions should be sent to ADIpolicy@apra.gov.au by 31 January 2020 and addressed to:

General Manager

Policy Development

Policy and Advice Division

Australian Prudential Regulation Authority

4.2 Important disclosure notice – publication of submissions

All information in submissions will be made available to the public on the APRA website unless a respondent expressly requests that all or part of the submission is to remain in confidence.

Automatically generated confidentiality statements in emails do not suffice for this purpose.

Respondents who would like part of their submission to remain in confidence should provide this information marked as confidential in a separate attachment.

Submissions may be the subject of a request for access made under the Freedom of Information Act 1982 (FOIA).

APRA will determine such requests, if any, in accordance with the provisions of the FOIA. Information in the submission about any APRA-regulated entity that is not in the public domain and that is identified as confidential will be protected by section 56 of the Australian Prudential Regulation Authority Act 1998 and will therefore be exempt from production under the FOIA.

4.3 Request for cost-benefit analysis information

APRA requests that all interested stakeholders use this consultation opportunity to provide information on the compliance impact of the proposed changes and any other substantive costs associated with the changes. Compliance costs are defined as direct costs to businesses of performing activities associated with complying with government regulation. Specifically, information is sought on any increases or decreases to the compliance costs incurred by businesses as a result of APRA’s proposal.

Consistent with the Government’s approach, APRA will use the methodology behind the Regulatory Burden Measurement Tool to assess compliance costs. This tool is designed to capture the relevant costs in a structured way, including a separate assessment of upfront costs and ongoing costs. It is available at: https://rbm.obpr.gov.au/home.aspx.

Respondents are requested to use this methodology to estimate costs to ensure that the data supplied to APRA can be aggregated and used in an industry-wide assessment. When submitting their cost assessment to APRA, respondents are asked to include any assumptions made and, where relevant, any limitations inherent in their assessment. Feedback should address the additional costs incurred as a result of complying with APRA’s requirements, not activities that institutions would undertake regardless of regulatory requirements in their ordinary course of business.

Attachment A – Policy options and estimated comparative net benefits

Two policy options are discussed further below, together with a preliminary analysis of the costs and benefits of each. The analysis of costs associated with each option focuses on compliance costs, that is, the direct administrative, substantive (business) and financial costs incurred by ADIs in complying with government regulation. Indirect costs for ADIs and other stakeholders arising as a consequence of regulation (or not applying regulation) are also considered.

Any information provided in response to APRA’s request for cost-benefit analysis information will be used by APRA to quantify the change in regulatory burden using the Regulatory Burden Measurement Tool, and inform calculations of the net benefits of the proposal.

Option 1 | No change to the existing APS 111. |

|---|---|

Option 2 | An update of APS 111 to amend the capital treatment, at Level 1, of equity investments in ADIs and equivalent overseas deposit-taking institutions and their subsidiaries, and insurance companies that are subsidiaries of the ADI; reflect APRA’s position on the Basel Committee standards, statements and guidance for ADIs’ equity investments in funds and TLAC holdings and capital arbitrage transactions; and clarify and simplify some of the content in the Prudential Standard. |

Option 1 – No change to the existing APS 111

Under this option, ADIs would not incur any additional compliance costs.

However, aspects of APS 111 may remain unclear and open to interpretation, requiring an expanded suite of FAQs or ad hoc letters to clarify the Prudential Standard.

Peer group comparisons with banks in other jurisdictions may be more difficult since regulators in these jurisdictions are likely to take account of Basel standards, statements and guidance.

Whilst not related to compliance costs, the costs of maintaining the status quo (e.g. continuing the existing capital treatment of equity investments in banking and insurance subsidiaries) could well be high, and detrimental to Australian depositors, with the amount of Regulatory Capital likely overstated for domestic risks for ADIs with large concentrated exposures. The status quo would provide further incentive for an ADI to support these investments with debt, allowing the equity investment to be further levered, amplifying risks to Australian depositors.

Option 2 – An update of APS 111

Under this option, ADIs would incur additional compliance costs.

The additional compliance costs under this option involve a one-off update to an ADI’s policies and processes to reflect changes to the Prudential Standard. There are also legal costs of updating the documentation of capital instruments. Under this option, APRA envisages a start date of 1 January 2021 for the introduction of the reforms. APRA considers there would be sufficient notice of proposed prudential standard requirements to allow ADIs to undertake any necessary changes to their policies and processes and documentation.

APRA considers the costs of complying is not materially more burdensome for ADIs than the current costs of complying as this option does not involve any changes to ADIs’ regulatory reporting requirements to APRA. ADIs already provide APRA with documentation associated with the issue of capital instruments and a statement of compliance. APRA considers there are no delay costs in relation to this option (e.g. expenses and loss of income incurred by an ADI through an application delay or an approval delay) as where the terms of a capital instrument depart from established precedent, an ADI is already required to consult with APRA on the eligibility of the instrument in advance of the issuance of the instrument, and provide APRA with all information and documentation it requires to assess the eligibility of the instrument.

Clarification of technical issues is being included in the Prudential Standard so there are no material extra costs expected. The Prudential Standard would be clearer and less open to interpretation. The proposed changes are expected to improve the transparency of capital instruments, and assist in their issuance.

This option also promotes certainty, and comparability which are key elements in the measurement and assessment of capital adequacy across all ADIs.

Peer group comparisons with banks in other jurisdictions is enhanced since regulators in these jurisdictions are also likely to take account of Basel standards, statements and guidance.

A benefit of the proposed changes to the capital treatment of equity investments in banking and insurance subsidiaries under Option 2 is that it mitigates domestic risks, reinforces ‘unquestionably strong’ capital targets at Level 1, and enhances financial stability. While costs associated with this particular proposal are capital costs and not regulatory costs (i.e. administrative, substantive compliance costs and delay costs), APRA’s proposal does not change the aggregate amount of capital in the system for these investments; ADIs with small diversified exposures will hold less capital for the exposures and others with large concentrated exposures will hold more.

ADIs will have a number of options in the way they choose to respond to the proposal to change the capital treatment of ADIs’ investments in banking and insurance subsidiaries – in this regard restructuring is an option but not a requirement to comply with the proposal. How ADIs choose to respond to the proposal to change the capital treatment will also partly depend on where the RBNZ lands on its proposed capital reforms.

Removal of the use of SPVs and stapled security structures promote simple structures, and is not expected to materially affect the ability of ADIs to issue capital instruments. Existing capital instruments eligible for transition under the existing APS 111 will continue to be eligible for transition under the revised standard.

For these reasons, APRA is of the view that Option 2 provides the greatest net benefit.

DisclaimerWhile APRA endeavours to ensure the quality of this publication, it does not accept any responsibility for the accuracy, completeness or currency of the material included in this publication and will not be liable for any loss or damage arising out of any use of, or reliance on, this publication. © Australian Prudential Regulation Authority (APRA) This work is licensed under the Creative Commons Attribution 3.0 Australia Licence (CCBY 3.0). This licence allows you to copy, distribute and adapt this work, provided you attribute the work and do not suggest that APRA endorses you or your work. To view a full copy of the terms of this licence, visit https://creativecommons.org/licenses/by/3.0/au/ |