21 May 2026

The System Risk Outlook provides an overview of risks and vulnerabilities affecting the Australian financial system, from the perspective of Australia’s financial safety regulator.

21 May 2026

The System Risk Outlook provides an overview of risks and vulnerabilities affecting the Australian financial system, from the perspective of Australia’s financial safety regulator.

The Australian financial system, including APRA‑regulated banks, insurers and superannuation funds, remains resilient in an increasingly volatile and interconnected world. Strong capital, liquidity and prudential safeguards mean our financial system is well-positioned to absorb shocks and continue providing critical services to households and businesses, even if economic conditions deteriorate.

At the same time, the risk environment is evolving. Geopolitical tensions, rapid technological change and growing global interconnectedness are reshaping how shocks could emerge and transmit through the system.

To ensure resilience is maintained, APRA has intensified its oversight of its entities given developments in both the international and domestic environments and is sharpening its expectations for sound risk management by regulated entities. This edition of the System Risk Outlook highlights some key areas where APRA is currently focused but does not capture the full range of issues APRA continues to monitor across the system.

As Australia’s financial safety regulator, APRA plays a central role in maintaining and strengthening resilience in the financial system. This objective is shared with other agencies on the Council of Financial Regulators (CFR), with each contributing to financial stability through different mandates. But what does resilience look like in practice, and why does it matter?

At its core, resilience is the capacity of the financial system to withstand and recover from shocks. This means maintaining confidence that deposits are safe, insurers can pay valid claims, and superannuation funds are managing members’ money well – even under stress. A resilient financial system can also continue to provide critical services and support economic activity during periods of disruption, underpinning trust in the system as a whole. Building resilience in good times is essential, so shocks – when they happen – are absorbed rather than amplified.

The regulation of Australia’s financial system has been designed with resilience front of mind. Through its prudential framework, APRA sets standards and safeguards that strengthen institutions ahead of stress, helping lean against the build-up of vulnerabilities during upswings and supporting shock absorption during downturns. By taking a countercyclical approach – building buffers in strong conditions so they can be drawn on during stress – the framework helps sustain confidence in the system, including among international investors, and supports continued access to funding at relatively low cost.

A useful way to understand resilience is to think of the financial system as a house that must remain safe and liveable in all kinds of weather. In calm conditions, most houses appear to function well. But resilience is only truly tested in bad weather, when the strength of the underlying structure determines whether damage is absorbed or amplified. Seen this way, a resilient financial system has several key characteristics:

As with a well-built house, resilience starts with a strong foundation. For financial institutions, this means financial cushions and buffers that absorb losses, alongside robust operational, governance and risk management practices that allow them to continue functioning or recover quickly from economic downturns or disruptions.

A resilient financial system has appropriate rules and oversight. Much like building standards for a house – which set requirements for structural strength, drainage and fire safety – the guardrails for the financial system are designed to reduce the risk that vulnerabilities accumulate unnoticed, while still allowing the system to grow, innovate and function efficiently.

In a resilient house, damage to one area should not undermine the integrity of the whole structure. Likewise, a resilient financial system limits the spread of stress, reducing the risk of contagion or spillovers across institutions. This allows institutions to fail or be resolved in an orderly way, while preserving essential services and confidence in the system.

In a house, damage to load-bearing elements or essential systems can compromise the stability of the entire structure. Similarly, some financial institutions play a more critical role for system resilience than others. The distress or failure of large or highly interconnected institutions can have far-reaching consequences, requiring stronger safeguards – like larger buffers and closer supervision – to protect financial stability.

Resilience is not static. Even where the system is resilient today, it must continue to learn from the past and adapt as new and unanticipated threats emerge. Just as building standards evolve over time, the financial system and the regulatory framework must adapt to technological change, shifting economic conditions and emerging risks.

Importantly, APRA pursues resilience in a way that balances safety with competition and efficiency. Prudential settings are designed to support resilience without unduly constraining institutions’ ability to take risk or support economic activity. In practice, this means APRA does not pursue a ‘safety at all costs’ agenda. A zero-failure regime would impose severe constraints on risk-taking, limiting the financial system’s ability to perform its vital role in the economy. Instead, APRA’s focus is on reducing the likelihood that vulnerabilities build up across the system and ensuring that, if stress does occur, it can be absorbed without disrupting critical financial services or undermining confidence in the financial system.

This chapter provides an overview of what APRA is seeing in the international environment, highlighting external shocks and global vulnerabilities that could affect the Australian financial system.

APRA is seeing a more challenging international risk environment. Geopolitical tensions, including the escalation of conflict in the Middle East, have increased risks to the global economy and financial markets. More broadly, vulnerabilities remain in financial markets, and technological developments are creating new and evolving sources of risk, including from cyber and AI‑related threats.

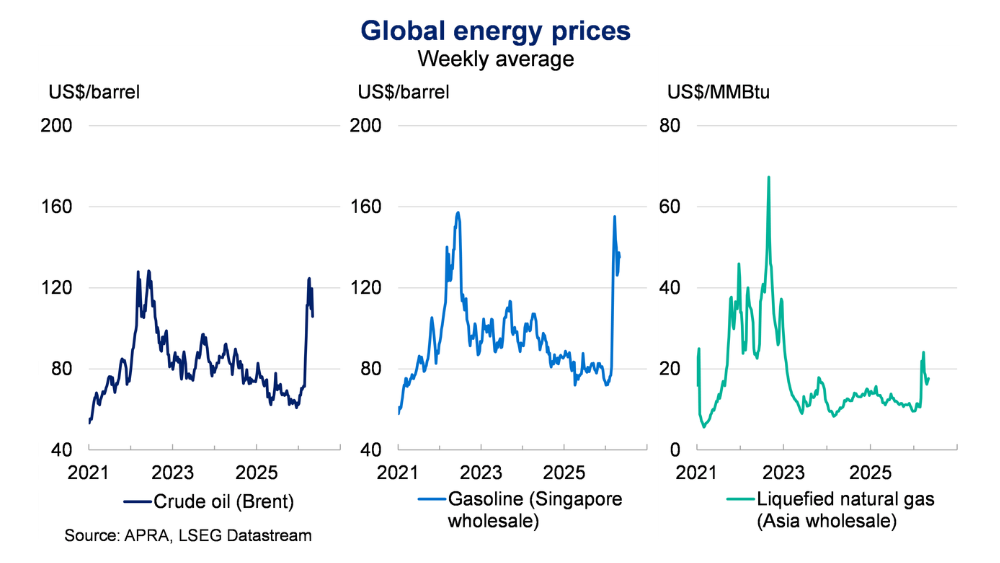

The escalation of conflict in the Middle East has had a material adverse impact on global energy supply. The conflict has seen the Strait of Hormuz close for an extended period, disrupting around 20 per cent of global oil supply, and critical energy infrastructure in the region has been damaged. These developments have driven a sharp rise in global oil and gas prices, which remain volatile on a day-to-day basis (Figure 1). In response, some governments have implemented fuel rationing measures to preserve local supply. Higher energy prices and supply disruptions are being felt by consumers globally, while disruptions to transport and logistics in the region have affected trade in a range of other commodities.

Developments in the Middle East have shifted the near-term outlook for the global economy. The Reserve Bank of Australia (RBA) and Treasury expect inflation in Australia’s major trading partners to be higher than previously anticipated, with growth outcomes differing across economies depending on their exposure to international commodity markets. Over the longer term, the conflict is likely to contribute to a more volatile and uncertain geopolitical environment, place additional pressure on public finances in some economies, and accelerate global efforts to diversify energy sources and supply chains.

Recent developments in global financial markets include:

Beyond geopolitical and market developments, technological change continues to reshape the global financial system. Rapid innovation is influencing how financial services are delivered, with the potential for significant efficiency benefits and expanded access to markets and services. At the same time, this innovation is also changing how operational risks may emerge and transmit across borders. This has contributed to increased attention by regulators internationally on a range of operational and other non-financial vulnerabilities. Some key international developments are highlighted below.

AI is being rapidly adopted across the global financial services industry to support automation, decision making and customer service. As a result, the governance and oversight of AI-enabled systems is becoming a greater focus of regulators. For example, the Monetary Authority of Singapore is consulting with industry on detailed guidance for managing AI-related risks, while in the UK, regulators are working closely with industry to monitor the degree of AI adoption and assess potential risks to financial stability.

The capabilities of cyber threat actors continue to grow, with cyber risks increasingly shaped by broader economic and geopolitical dynamics. An area of heightened attention is the potential for increased threats from highly advanced AI models. While many challenges are immediate, some risks may crystallise over a longer horizon, including the potential for advances in quantum computing to undermine widely used encryption methods. Enhancing cyber resilience remains a top priority for regulators globally.

Tokenisation is expanding across global financial markets, enabling financial assets such as securities or bonds, as well as insurance contracts, to be represented digitally and transactions to be settled more quickly. International developments highlight both the potential to deliver efficiency and transparency benefits, and new operational, cyber and interconnectedness considerations. Box A explains the concept of tokenisation in more detail.

Tokenisation is the process of representing value, rights or obligations in digital form using programmable tokens. This can include financial assets, such as shares and bonds, money-like instruments such as deposits, and contractual arrangements such as insurance policies. Blockchain and distributed ledger technology is the infrastructure on which tokenised assets are recorded and transacted, and these tokens can be programmed to automatically execute predefined actions when certain conditions are met. While tokenisation is not yet widespread in the global financial system, it is expanding rapidly (particularly in the United States).

One form of tokenised money that has attracted considerable global interest is stablecoins issued by private sector entities. Stablecoins are a type of bearer instrument, which means they grant ownership and payment rights to whomever possess them (rather than to a named individual). The most common type of bearer instrument is physical cash. Stablecoins claim to hold a stable value relative to a reference asset, such as a fiat (traditional) currency like the Australian or US dollar. Confidence in this value is supported by reserve assets held to back the stablecoin, with rules on these reserves differing across jurisdictions.

Banks have also demonstrated an interest in tokenisation. Some large overseas banks have begun issuing ‘tokenised deposits’, which are a digital representation (‘twin’) of an existing bank deposit. In addition, banks have been experimenting with ‘deposit tokens’, which may offer functionality similar to stablecoins. Central banks are also exploring central bank digital currencies (CBDCs) as a tokenised form of public money. In the insurance sector, tokenisation is being considered as a way to digitise policies and claims and support more automated risk transfer.

Tokenisation could bring a range of benefits to the global financial system, including:

At the same time, tokenisation could introduce new vulnerabilities that may amplify shocks to the global financial system, including:

Tokenisation represents a rapidly evolving approach to financial market infrastructure that could change how assets are issued, traded and settled. While adoption remains uneven across countries and sectors, the combination of potential efficiency gains and new forms of risk means tokenisation will be increasingly important to the global financial system.

Private markets comprise investments that are not traded on public exchanges and are typically held for the long term, including private equity, private credit, infrastructure and other unlisted real assets. Globally, private market assets under management are estimated to be around US$20 trillion, a roughly fourfold increase from a decade ago. While this represents significant growth over a short period, private markets remain much smaller than public markets, which collectively hold assets worth hundreds of trillions of dollars.

When structured and governed effectively, private markets can deliver clear benefits to the global financial system, including diversification for investors and access to longer-term or more flexible financing for borrowers. These features have supported strong growth in recent years. However, the same characteristics can also give rise to vulnerabilities, particularly where opacity, leverage and weaker oversight are present.

Recent developments overseas have brought some of these vulnerabilities into sharper focus, particularly in private credit (non-bank lending conducted outside public markets):

More broadly, there is uncertainty about how private markets would behave in a severe downturn, reflecting the limited extent to which they have been tested under stress. In late 2025, the Bank of England announced that its next system-wide exploratory scenario will examine how private markets operate under stress and the potential implications for the UK financial system and economy.

This chapter focuses on vulnerabilities and sources of resilience within the Australian financial system, including how global shocks transmit domestically and how APRA is reinforcing system resilience.

The Australian financial system remains resilient, but heightened global risks mean we cannot be complacent. APRA is reinforcing resilience across a range of dimensions, including strengthened crisis preparedness, operational and cyber resilience, and targeted actions on longstanding and emerging vulnerabilities. These efforts support the financial system’s ability to absorb shocks and continue providing essential services.

Global energy developments are spilling over to the Australian economy and financial system. The RBA and Treasury expect elevated global energy prices to add to inflationary pressures and weigh on economic growth, depending on the duration and intensity of the conflict. While APRA-regulated entities have limited direct exposures to the Middle East, APRA has been engaging regularly with entities to understand how they are being affected by developments overseas and to assess preparedness under a range of scenarios.

APRA is seeing that:

Beyond direct financial exposures, APRA is considering how entities’ reliance on global material service providers could amplify stress (an issue discussed more broadly below). While APRA-regulated entities appear to have limited direct exposure to material service providers located in the Middle East, a larger share of entities rely on US-based providers (particularly for technology services). APRA’s close entity engagements will continue while conditions remain fluid.

APRA is active in the Council of Financial Regulators' (CFR) Geopolitical Risk Program, which is working with Australia’s largest financial institutions to strengthen crisis preparedness and uplift geopolitical risk management. The Program made important progress in 2025 to diagnose opportunities to enhance risk management, and in 2026 is focused on risk reduction through an established set of minimum expectations for geopolitical risk readiness that apply to entities in the Program. These principles-based expectations cover areas including enterprise risk management, payments contingency, personnel risk and political risk. Continued strong engagement with industry is critical to reinforcing resilience across the financial system.

This work complements a range of targeted initiatives underway by APRA to strengthen resilience to geopolitical vulnerabilities. This includes core bank stress testing activities, an expanding cyber program, active supervision against a new prudential standard on operational risk management, and exploratory work on strengthening liquidity resilience to geopolitical shocks. APRA is also integrating geopolitical considerations into routine supervision activities to ensure that regulated entities continue to strengthen risk management and contingency planning.

At the core of Australia’s financial system resilience are strong capital and liquidity positions across regulated entities. These help ensure the system can absorb shocks and continue providing essential services to households and businesses, even in a pronounced economic downturn or recession.

Setting capital requirements is one of APRA’s core prudential tools to support financial system safety and stability. Capital provides a financial cushion that enables institutions to absorb unexpected losses arising from normal business activities, like loan defaults for banks or surges in insurance claims (see APRA Explains). In addition to minimum capital requirements – which institutions are expected to meet at all times – APRA’s prudential frameworks include additional layers of capital (or buffers) and an expectation to be forward-looking in planning and managing their capital. By allowing buffers to be drawn down in downturns, APRA’s framework supports institutions’ ability to continue providing financial services to households and businesses when conditions are most challenging.

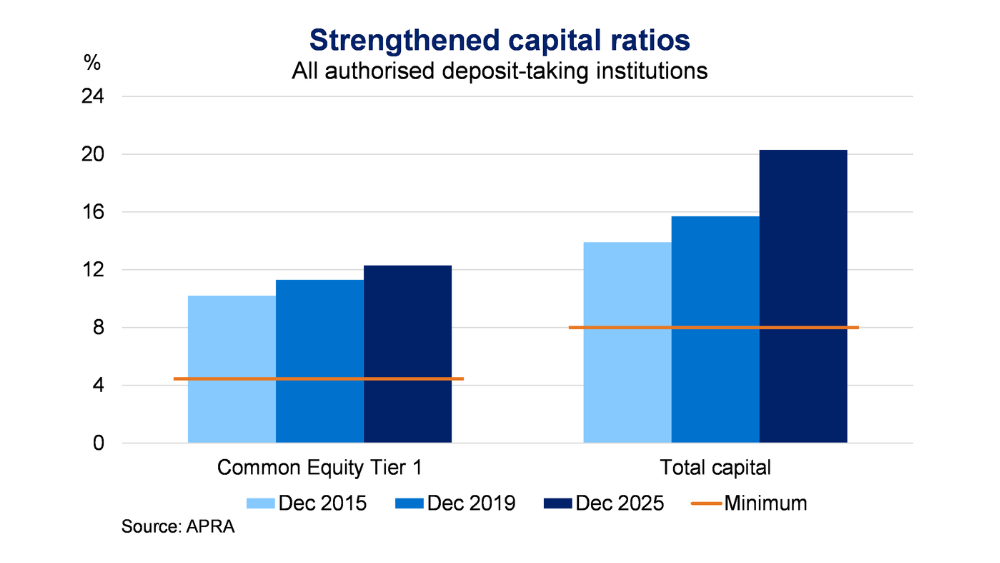

At an aggregate level, APRA is seeing that Australian banks’ capital ratios have been high and stable for several years. These ratios are well above regulatory minimums and higher than at the onset of the COVID‑19 pandemic (Figure 3). APRA’s latest round of bank stress testing reaffirmed that these capital positions provide resilience to 'severe but plausible' downside scenarios (Box B). Taken together, APRA’s ‘unquestionably strong’ capital framework, adopted in 2020, provides confidence in the banking system’s ongoing capacity to provide critical support to customers and the economy through a more challenging global environment. Our capital requirements also support strong credit ratings, helping lower funding costs and providing Australia with access to foreign investment. Solid profitability and recent increases in provisioning further reinforce banks’ resilience.

APRA is also seeing that the insurance industry remains well capitalised, with key capital ratios comfortably above regulatory minimums. While insurers are facing a range of structural challenges affecting demand, such as an ageing population, climate change and rising mental health claims, strong capital positions and reinsurance arrangements are supporting insurers’ capacity to absorb these pressures and continue providing cover to policyholders.

Liquidity, or the ability to meet cash demands as they come due, is another critical dimension of financial resilience for APRA-regulated entities. Banks must be able to meet depositors’ demands, while insurers need to pay claims, sometimes at short notice. APRA is seeing that banks hold sufficient quantities of liquid assets to meet their obligations, and increased supervisory focus on liquidity since the 2023 collapse of Silicon Valley Bank has contributed to some uplift in liquidity risk management practices. For insurers, liquidity risk remains low, reflecting both traditional investment strategies and access to reinsurance. However, APRA is closely monitoring developments that could pose challenges to liquidity over time, including exposures to unlisted assets and growing interconnectedness across the system.

APRA is constantly looking at its prudential settings to ensure they strike a balance between stability, efficiency and competition. On 16 March 2026, APRA announced a consultation roadmap for capital and liquidity reforms for banks aimed at ensuring the prudential framework remains fit for purpose in promoting financial resilience. The proposed changes seek to align Australia’s settings more closely with international practice, while maintaining APRA’s ‘unquestionably strong’ capital framework, and reinforcing liquidity resilience. The capital reforms are narrowly focused on building risk sensitivity into our regulatory framework for some types of corporate lending, which we expect to reduce regulatory burden and support productivity without compromising stability. Both capital and liquidity are important to ensure Australia’s financial system remains resilient in the face of any adverse economic conditions.

While strong financial positions underpin resilience at individual institutions, the resilience of the financial system as a whole also depends on how institutions are connected and interact under stress. These interconnections can enhance efficiency, but they can also amplify the transmission of stress when shocks occur. Direct financial links – such as funding relationships between institutions – can leave both entities exposed in the event of a sudden withdrawal of funds or default. Indirect links, including common exposures through financial markets, can also transmit stress across the system. Maintaining visibility of these linkages is an important part of APRA’s work to support system-wide resilience.

One area of heightened focus is the relationship between the banking and superannuation industries. Superannuation is a large and growing part of Australia’s financial system. Some of the structural features of superannuation – such as steady inflows from members and restrictions on leverage – mean that it acts as an important stabiliser during stress and strengthens the system. At the same time, its growing importance means it has become more interconnected across the system, particularly with banks.

Aggregate data show that the superannuation industry accounts for just over 10 per cent of banks’ total domestic funding. Looking across different types of funding, superannuation funds hold around 30 per cent of banks’ short-term debt (such as negotiable certificates of deposit) and equity (Figure 4). These shares rise to around 40 per cent when estimates of superannuation funds’ indirect claims on banks via investment funds are taken into account. If superannuation funds were forced to sell these assets rapidly during a stress event, this could increase bank funding costs and potentially exacerbate liquidity stress across the system.

APRA’s inaugural system risk stress test has reinforced the value of analysing these linkages through exploratory, system-level scenarios. Phase 1 of the exercise showed that superannuation funds can continue to be a stabilising force during a shock, but in some cases, their actions can also amplify the negative effect of a shock on members and the broader system. The Phase 1 results were summarised in the November 2025 System Risk Outlook, and APRA plans to publish a final report incorporating Phase 2 findings in mid-2026. More broadly, APRA’s stress testing program continues to provide important insights into various dimensions of financial resilience of the entities we regulate, as well as some aspects of non-financial resilience (Box B).

Stress testing is a key component of APRA’s toolkit to maintain the safety and stability of the Australian financial system. At its core, stress testing involves assessing the impact of a range of severe downside scenarios on the financial system. Some exercises may be focused on specific entities within the system, while others may look at the system as a whole. Importantly, insights from stress testing are used to inform APRA’s prudential supervision and policy priorities. Performing stress testing regularly using varied scenarios encourages ongoing improvements in stress testing capability for both APRA and regulated entities.

APRA’s stress testing program includes three complementary activities.

APRA’s stress testing program is constantly evolving to ensure it continues to provide rigorous assessments of entities’ resilience. This is especially important in an environment where risks to the financial system are heightened, and as the Australian financial system becomes more interconnected, including with other financial systems globally. In 2025, a key evolution was APRA’s first exploratory system risk stress test. The findings of Phase 1 were summarised in Box C of the November 2025 System Risk Outlook, and Phase 2 results will be published in mid-2026.

In 2026, APRA is conducting a stress test with the five largest banks, focused on financial resilience in an increasingly volatile world. The stress scenario considers how a prolonged period of global disruption, driven by heightened geopolitical instability, could translate into a severe macroeconomic stress. A central feature of the scenario is a major global energy supply shock, with oil prices rising sharply and remaining elevated for an extended period, amplifying inflationary pressures and weakening global growth. For Australia, this results in a sharp rise in unemployment, significant declines in property prices and a sustained economic downturn, placing pressure on banks’ capital and liquidity positions.

This exercise is being run jointly with the Reserve Bank of New Zealand, deepening understanding of cross-border interlinkages between major Australian and New Zealand banks. The joint approach supports a coordinated assessment of how severe global shocks may transmit across parent and subsidiary balance sheets and strengthens Trans-Tasman stress testing capability for both supervisors and banks. Key insights from the stress test will be made available later this year.

APRA has a longstanding focus on lifting operational and cyber resilience across the industries it regulates, which has taken on greater importance as cyber threats and technological risks evolve. Key areas of focus include:

APRA has recently written a letter to industry to reinforce its expectations for AI-related governance arrangements and the management of supplier risks. Key concerns include board capability and effective oversight, heightened cyber risks, weak identity controls, increasing supply chain concentration and dependency, and inadequate assurance over dynamic AI systems. In response, APRA has set clear minimum expectations for boards and executives and signals an increase in supervisory intensity, including the potential for enforcement action where AI-related risks and vulnerabilities are not managed effectively. APRA will continue to engage with industry on AI and is currently finalising its forward plan for supervision of AI risks.

APRA continues to pursue a sizeable work program on cyber resilience alongside peer agencies on the CFR and is working to ensure that entities are alert to evolving risks and proactively taking actions to reduce their vulnerabilities. APRA has engaged with entities on the potential for widespread cyber impacts of highly advanced AI models. APRA heard clear recognition from regulated entities that these developments require a step change in cyber practices and a continued uplift in capabilities to protect critical technology assets. This uplift could involve the use of AI-enabled tools to identify vulnerabilities and respond more rapidly to threats. In line with advice from the Australian Signals Directorate, APRA is emphasising the need for entities to prioritise and strengthen cyber security defences.

Beyond specific geopolitical events, managing vulnerabilities introduced by material third-party service providers remains a core operational resilience focus for APRA. One of the risks APRA continues to highlight is concentration, where many institutions rely on the same providers, making the system vulnerable to a single point of failure. This includes concentration of AI providers, and APRA expects entities to actively manage concentration risk. In addition, APRA is progressively increasing supervisory focus on material service provider dependencies, including direct engagements with service providers that are important across the system.

Project Acacia – a joint research initiative by the RBA and the Digital Finance Cooperative Research Centre – has provided valuable insights on how innovations in digital money and settlement infrastructure might support the development of tokenised asset markets in Australia. The CFR agencies have been supporting Project Acacia, given the importance of a whole-of-government approach to help promote safe innovation with clear understanding of the risks. APRA supports responsible innovation that could enhance the functioning of the Australian financial system and will continue to support the RBA in implementing a program of work that builds on Project Acacia’s findings.

Australia’s households are facing a more challenging economic environment. Higher interest rates and inflation are placing greater pressure on household finances. Households remain highly indebted and housing credit growth remains strong, although there are signs of some moderation in credit growth and housing price growth. At the same time, the outlook for the global and domestic economies is highly uncertain. APRA’s macroprudential policy settings form part of the broader framework supporting financial system resilience in this environment.

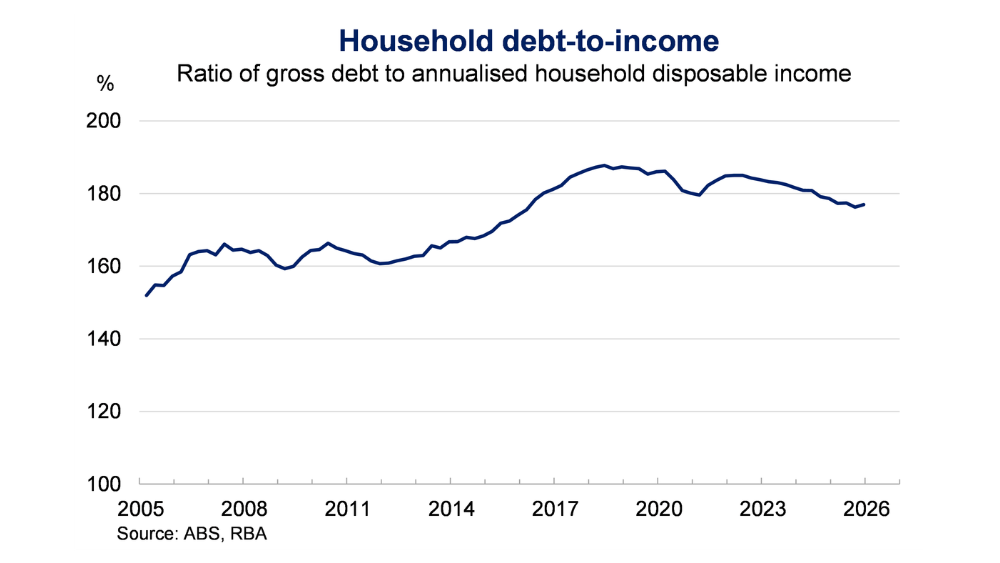

High household debt is a key vulnerability of the Australian financial system. While aggregate household debt relative to disposable income has declined from its peak, it remains high by historical and international standards at just under 180 per cent (Figure 5). Highly indebted households are more likely to experience difficulties servicing their loans when economic conditions deteriorate, which can undermine the resilience of banks and the broader financial system.

Since 1 February 2026, APRA-regulated banks have been subject to a limit that restricts new mortgage lending to borrowers with debt of six times income or more to 20 per cent or less. This limit applies separately to owner-occupiers and investors. APRA activated this policy pre-emptively to contain a build-up of housing-related vulnerabilities, particularly from lending to highly indebted investors. Preliminary data for the March quarter 2026 suggest that lending at debt of six times income or more remained well below the 20 per cent limit (Figure 6). At the individual bank level, only a small number of banks are trending close to the limit.

New lending to housing investors has been very strong over the past year, but the outlook has become more uncertain in recent months. Investor credit growth was about 10 per cent over the year to March, its fastest pace in a decade. Despite strong competition among banks for investor loans, lending standards have not eased. Looking ahead, higher interest rates, weaker sentiment and weaker housing price growth are expected to weigh on investor demand.

In aggregate, borrowers and lenders exposed to the housing market have retained a high level of resilience. Many households have built up large cash and equity buffers – larger than those held prior to the onset of COVID-19 – and the share of non-performing loans remains low. While financial pressures are expected to increase alongside higher energy costs and interest rates, recent RBA analysis suggests that most borrowers can continue servicing their debts under a range of adverse scenarios. Banks’ sound and prudent lending standards further help guard against the material accumulation of vulnerabilities. APRA continues to regularly assess its macroprudential policy settings to ensure they support financial stability (Box C).

The objective of macroprudential policy is to promote financial stability. It operates in a countercyclical way by building resilience or reducing excessive risk-taking during periods of strong financial conditions, when vulnerabilities tend to accumulate, so that the financial system can remain stable and support the economy if conditions deteriorate.

APRA has a range of tools, including those described in the November 2025 System Risk Outlook, that can be applied and adjusted where systemic risks become excessive. These measures have typically been deployed through the banking system, reflecting the central role of leverage in the financial cycle and banks’ significant exposures to the household sector. This Box provides some examples to illustrate how these tools operate in practice.

Taken together, these examples illustrate how macroprudential policy is designed to operate through the financial cycle. By building resilience or reducing excessive risk-taking when vulnerabilities are increasing and supporting the financial system and economy when conditions deteriorate, macroprudential policy ultimately aims to promote financial stability.

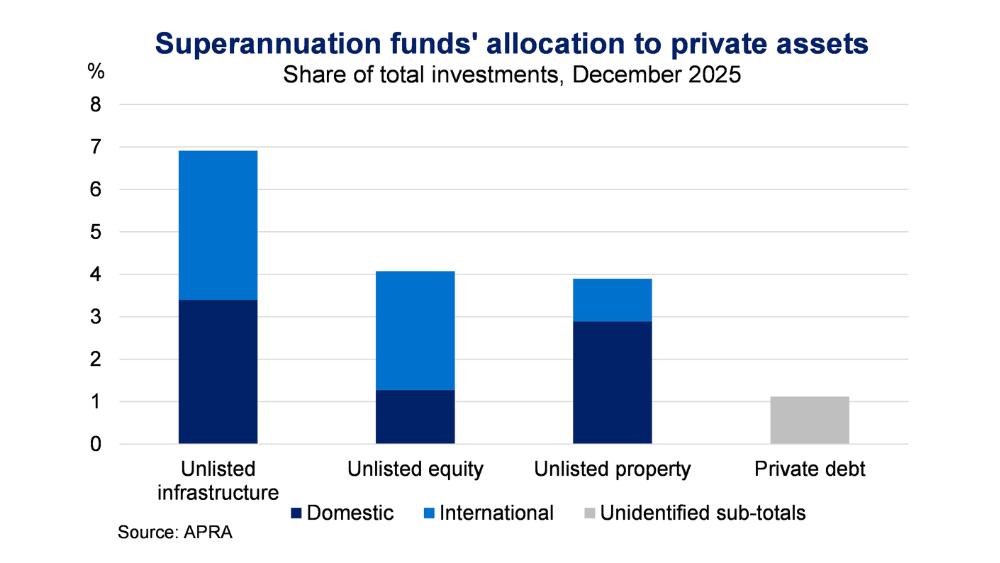

APRA is seeing that the industries it regulates have diverse exposures to private markets, both domestically and overseas. Developments in private markets globally could spill over to Australia through regulated entities’ exposures to international asset markets and funding arrangements. About 16 per cent of investments by APRA-regulated superannuation funds are in private market assets, and around half of this exposure is offshore (Figure 7). The insurance industry has smaller investment exposures, at around 4 per cent of total assets, but these exposures are increasing as insurers seek higher returns and greater diversification. Banks’ exposures are more indirect, reflecting their role in providing financing rather than investing directly. APRA has observed a recent increase in banks’ appetite for, and exposure to, international funds finance products, which are used to provide debt and other financial support to private investment funds.

Consistent with other CFR regulators, APRA considers that risks from private credit are contained domestically. Private credit in Australia differs from overseas in important ways, including being smaller in size and more concentrated in real estate rather than technology. Williams and Timbs, in their 2025 report prepared for the Australian Securities and Investments Commission (ASIC), estimate private credit in Australia to be relatively small, at around $200 billion, or roughly 3 per cent of the size of the banking system. However, the growing scale, complexity and cross-border nature of private markets, including private credit, mean international stress could transmit more quickly and through more channels than in the past.

APRA continues to monitor areas of vulnerability for entities exposed to private markets, particularly where global developments could transmit to Australia. While system-wide risks from domestic private credit remain contained, regulated entities are globally connected and therefore exposed to developments overseas. APRA has recently reinforced expectations around valuation governance, investment governance and liquidity risk management for superannuation funds investing in unlisted assets. We have also finalised changes to the capital treatment for certain life insurance products that allow unrated and privately rated investments to back those products, and increased supervisory focus on banks’ funds finance portfolios. Data gaps remain a challenge for effective oversight, and APRA will continue to work closely with ASIC and other CFR agencies to improve visibility of private markets and monitor emerging vulnerabilities.