Recovery and resolution planning

As Australia’s financial safety regulator, APRA is responsible for protecting the interests of bank depositors, superannuation members and insurance policyholders. We do this by setting and enforcing legally binding standards for these institutions to meet in areas such as capital, liquidity, governance and cyber security.

These prudential standards are designed to ensure our banks, insurers and super funds remain financially and operationally resilient so they can meet their commitments to customers in good times as well as in a downturn or a crisis.

While the failure of these institutions in Australia has been rare, APRA doesn’t set standards so high that we guarantee a zero rate of failure. To do so would place unnecessary costs on shareholders and customers of APRA-regulated entities, as well as impeding innovation and dynamism.

Sometimes, as in any competitive industry, a bank, insurer or superannuation trustee, gets into financial difficulty.

When that happens, APRA’s prudential standards and industry supervision are designed to ensure the entity is well positioned to respond to the stress and can ideally restore its resilience and continue serving its customers.

If it is unable to recover, APRA aims to minimise the impact of an entity failure to ensure little or no loss to customers and minimal disruption to the financial system. This can happen via either a voluntary exit by the failing entity or through APRA’s intervention – a process known as “resolution”.

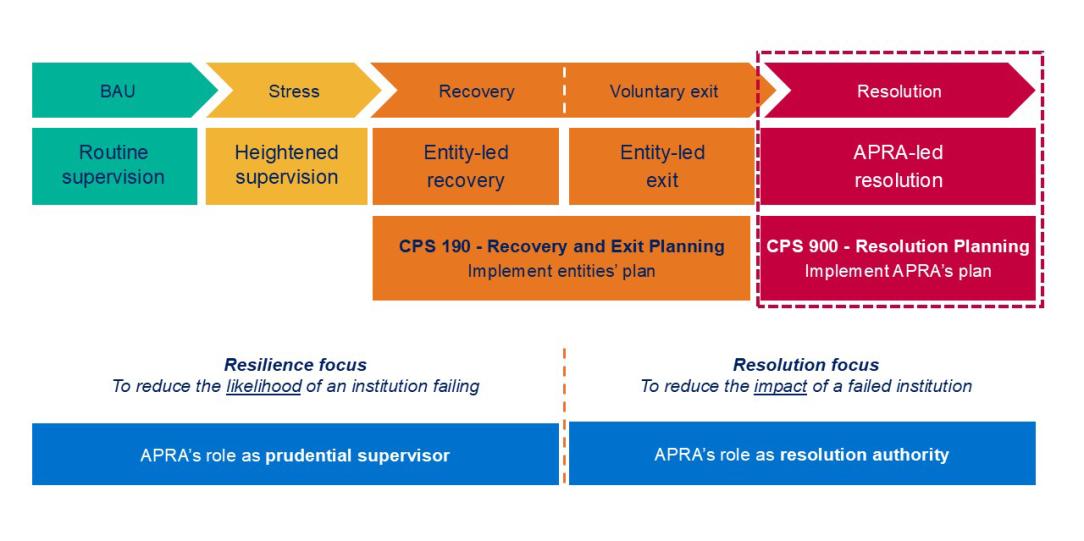

Recovery, exit, and resolution stress continuum

Hope for the best, prepare for the worst

In early 2023, a mid-sized American bank called Silicon Valley Bank suddenly found itself in deep financial trouble. Amid the turmoil and market panic that followed, several other US banks also failed or needed rescuing.

Events such as this illustrates that a crisis at one financial institution isn’t just bad for that institution and its stakeholders, such as customers and investors. In a worst-case, it can spark serious problems for the broader financial system through “financial contagion”.

Given this, APRA doesn’t wait for one of its regulated entities to get into trouble before acting.

We require all APRA-regulated entities to undertake contingency planning to give them the best chance of recovery when in stress, as well as being prepared to exit the industry in an orderly manner if all recovery options fail.

This is known as recovery and exit planning.

For larger and more complex entities, and those that provide critical functions, we also work closely with them to ensure pre-positioning steps are taken during peacetime so they could be readily resolved by APRA should they fail. This includes developing bespoke resolution plans for these financial institutions.

This process is called resolution planning.

Smaller entities without critical functions would not generally require the same level of pre-positioning in order to be resolvable as they tend to have simpler operations.

Recovery and exit planning

Under Prudential Standard CPS 190 Recovery and Exit Planning, APRA-regulated entities must develop and maintain credible plans for managing stress. These include actions to restore their financial position (recovery) or, if recovery isn’t possible, actions to enable an orderly exit from APRA-regulated activity (exit).

A recovery and exit plan sets out the steps that an APRA-regulated entity could credibly take in a stressed scenario to protect its bank depositors, insurance policyholders or superannuation fund members. It typically specifies certain “triggers” that the entity uses to determine in advance what actions it needs to take in a crisis, depending on its severity.

Every business is different and so each recovery and exit plan is designed to take into account the size, business model and complexity of the APRA-regulated entity. As the business evolves over time, so should its recovery and exit plan.

APRA also expects entities to conduct regular operational tests of the plan so they are prepared to implement it should the need arise.

Resolution planning

Unlike recovery and exit planning, APRA is responsible for preparing resolution plans for entities subject to CPS 900 Resolution Planning – that is the larger and more complex entities, and those that provide critical functions. These entities are required to support the planning process by sharing information and establishing and maintaining capabilities.

APRA may use its crisis management powers to resolve an entity that APRA judges has become non-viable or where APRA has doubts about the entity’s ability to exit voluntarily.

In seeking to achieve an orderly resolution, APRA has a range of options available. The most appropriate option will always depend on the circumstance at the time and the risks that APRA is seeking to address.

These include:

- Appointing a statutory manager, who replaces the board and manages the distressed entity on behalf of APRA;

- Recapitalising the distressed entity by converting capital instruments to equity (shares). This is most likely for large, systemically significant entities.

- Transferring all or part of a distressed entity to another APRA-regulated entity. This is typically used for small to medium-sized entities with limited critical functions.

- Winding down the distressed entity’s business and managing its orderly exit from the industry. This is most likely for smaller entities with no critical functions or systemic significance.

Viva la resolution

APRA’s resolution powers are rarely used because the failure of APRA-regulated entities is rare. When entities have encountered serious financial difficulty in recent times, they have been able to exit the industry voluntarily or arrange a merger with a more sustainable partner, meaning there was no need for APRA to manage the process via a resolution.

Although our preference is for entities to engineer their own recovery from a stressed scenario or exit voluntarily in an orderly manner, APRA continues to exercise its resolution muscles so that we are ready to act decisively, if necessary, to protect bank depositors, insurance policyholders or superannuation members.

In the event that a bank or general insurer fails, the Australian Government may need to intervene to protect the safety of deposits and policyholders.

The Financial Claims Scheme (FCS) is an Australian Government scheme that protects depositors of locally incorporated banks, building societies and credit unions, as well as most policyholders of general insurers, should one of these institutions fail. APRA is responsible for administering the FCS once it is activated by the Australian Government.

For banks, the FSC covers up to $250,000 per account holder per bank, building society or credit union. It also covers most general insurance policies for claims up to $5,000, with claims above $5,000 eligible if they fulfil certain criteria.

Established in 2008, the FCS has never been activated for a bank failure but has been used once in general insurance.

You can learn more about the FCS here: Financial Claims Scheme