To: All authorised deposit-taking institutions

APRA will consult on enhancements to its capital and liquidity frameworks to better support our mandate to balance safety, efficiency and competition in promoting financial system stability. As Australia’s prudential regulator, APRA continually assesses the prudential framework to ensure it remains fit for purpose in promoting financial resilience with the most recent round of reviews resulting in amendments in Q3 2024. This is central to delivering our mandate and takes on heightened importance in the current risk environment.

Maintaining a strong and resilient banking system

APRA’s ‘unquestionably strong’ capital framework is a cornerstone of the Australian banking system’s resilience, ensuring banks are well-positioned to absorb shocks and respond to periods of turbulence. Strong capital positions must be paired with effective liquidity risk management and, while APRA’s supervision has ensured that the liquidity practices of Australian ADIs’ have strengthened in recent years, there is scope for further improvement. Strong liquidity resilience helps banks withstand stress by allowing time to restore confidence and avoid disorderly failure. This issue was underscored by the 2023 banking turmoil, which demonstrated how quickly liquidity stress can emerge when confidence falters.

APRA has reviewed its liquidity policy framework and will consult on liquidity proposals that build on existing supervisory efforts by APRA and industry to uplift risk management practices. APRA’s approach will be proportionate and targeted. For larger banks, the focus will be on vulnerabilities that are not captured by current minimum requirements, such as cliff risk from deposits just outside the 30-day horizon and intraday payment risk. For smaller banks, more risk-sensitive settings are planned to increase incentives for better risk management. This would allow banks with more stable funding sources to reduce their liquid asset holdings.

Opportunities for a more efficient regulatory framework

APRA monitors the calibration of its capital settings on an ongoing basis and has identified an opportunity to consult on narrowly targeted measures to reduce the regulatory burden on banks, while maintaining the strength of the banking system. APRA intends to make credit risk weights for selected forms of corporate lending more granular and risk sensitive. This will include lending to critical infrastructure projects, to high-quality corporates without a credit rating and to residential property developers. The adjustments are expected to increase banks’ capacity for this type of lending which would support business investment and productivity, while remaining consistent with an unquestionably strong, risk-based framework.

The final part of APRA’s package is implementing the Basel Committee’s Fundamental Review of the Trading Book (FRTB) standard. To finalise Australia’s implementation of Basel III, APRA intends to consult on a simplified version of the standard tailored to Australian conditions. APRA expects this approach will enable similar risk management outcomes but at a meaningfully lower implementation, and ongoing, cost.

‘Getting the balance right’ on financial resilience

Overall, we expect this package of policy reforms will be broadly cost neutral across the banking industry. APRA expects large banks will see benefits from targeted adjustments to capital settings but also some costs associated with improved liquidity resilience. The planned liquidity reforms for small banks should lead to cost savings for those that rely on more stable sources of funding.

Further detail on APRA’s approach and the timing for consultation can be found in Attachment A.

Yours sincerely,

John Lonsdale

Chair, APRA

Attachment A

Indicative consultation proposals

Workstream 1: Credit risk capital

APRA intends to consult on targeted amendments to the standardised capital framework to increase risk sensitivity and better align requirements with underlying risk:

- Infrastructure – allowing a lower risk weight for large domestic public infrastructure.

- Unrated corporates – allowing a lower risk weight for high-quality unrated corporate exposures subject to certain criteria.

- Land acquisition, development and construction (ADC) – adjusting criteria to allow for more exposures to qualify for the lower 100 per cent risk weight for residential property development.

APRA expects the changes will also provide more flexibility for internal ratings-based (IRB) ADIs that are currently bound by the standardised floor.

Workstream 2: Liquidity risk

For ADIs using the Liquidity Coverage Ratio (LCR) framework, APRA intends to consult on a range of measures including:

- Measures to address risks not covered by LCR minimum requirements (e.g. intraday risk and cliff risk), including consideration of a Pillar 2 liquidity framework.

- Improvements to liquidity risk monitoring through Internal Liquidity Adequacy Assessment Process (ILAAP) requirements.

- Broadening high-quality liquid asset (HQLA) eligibility, including for covered bonds (subject to ceilings and haircuts).

- Reviewing the LCR approach for foreign branches operating in Australia.

For ADIs using the Minimum Liquidity Holdings (MLH) framework, APRA intends to consult on a more risk-sensitive framework to incentivise better liquidity risk management practices. We’re also planning to create a more even playing field for industry by setting a transparent limit on the use of bank debt securities and other lower quality liquid assets.

APRA expects these changes will address gaps, strengthen the liquidity resilience of ADIs and incentivise better risk management. For small ADIs with more stable funding sources APRA expects the changes will generate some cost savings.

Workstream 3: Market risk

APRA intends to consult on a simplified version of the Basel Committee’s Fundamental Review of the Trading Book (FRTB) standard:

- APRA does not plan to implement the non-modellable risk factor framework or the modelled approach for default risk capital. APRA also plans to significantly streamline the internal risk transfer rules.

- APRA is considering adjustments to streamline the profit and loss attribution test as well as the trading-desk level requirements. APRA intends to repurpose some existing elements of our traded market risk framework, particularly the ‘Risks Not in VaR’ framework.

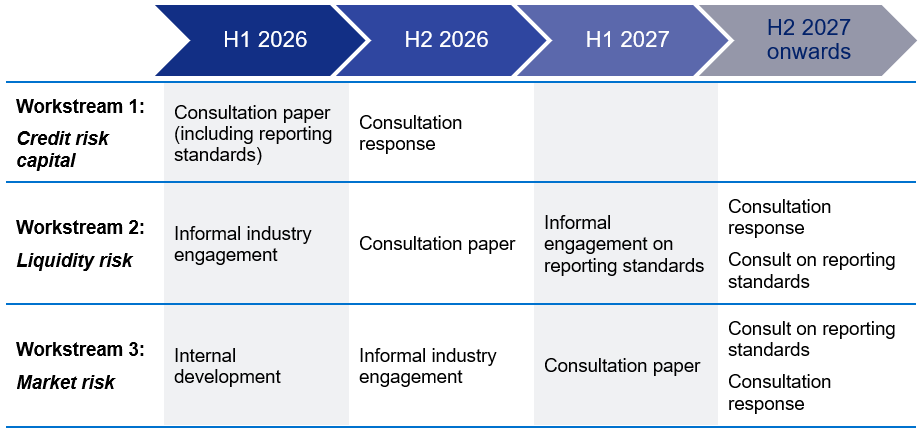

Indicative consultation roadmap

To help manage the burden on industry, APRA will progress each workstream independently and stagger consultations. A preliminary consultation roadmap for the package is shown in Figure 1. Informal industry consultation will begin in the coming weeks. APRA intends to incorporate this plan into its next Corporate Plan scheduled mid-year and, in consultation with other agencies, will update the Regulatory Initiatives Grid (RIG).

APRA will consult on the package in stages, starting with a consultation on changes to standardised risk weights for credit risk, planned for the first half of this year. Implementation timing will be confirmed as part of the consultation process. APRA will provide adequate time once requirements are finalised and will take account of implementation challenges raised by industry when setting final dates.

Figure 1 – Indicative consultation roadmap