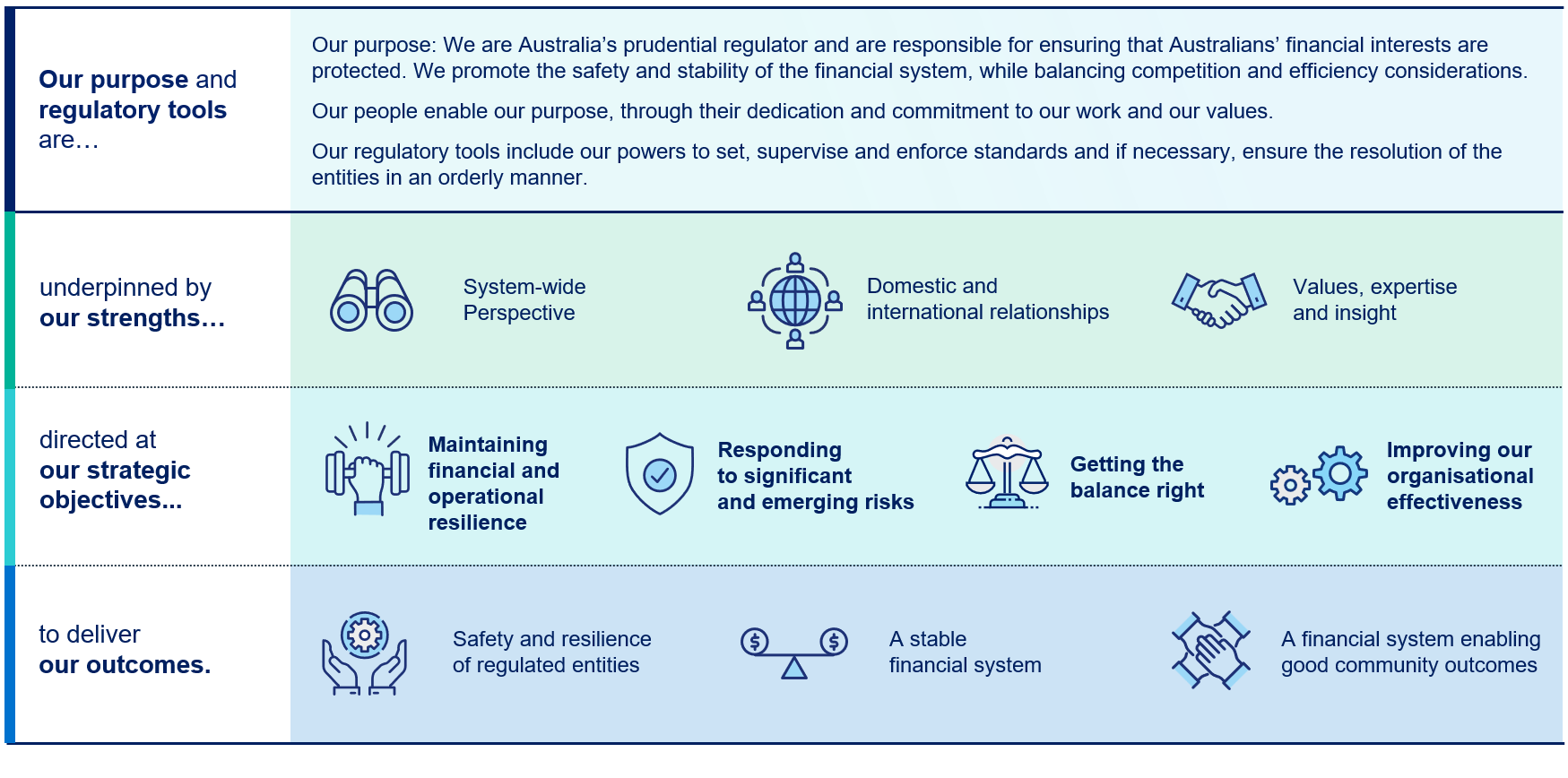

The first three strategic objectives focus on promoting the safety and stability of the financial system in a balanced and efficient way. Under these objectives, APRA has detailed specific policy, supervision and data initiatives planned for the banking, insurance and superannuation industries over the next 12-24 months. Regulated entities should read these industry priorities in conjunction with their entity-specific supervisory programs, which are calibrated to their Tier and Stage.

Under the Government’s Regulatory Initiatives Grid, APRA has consulted with other financial sector agencies on the planned timings of its initiatives with the aim of improving coordination and alignment across regulators.

APRA’s planned industry initiatives have been scoped to address identified risks to safety and stability, while ensuring that APRA’s regulatory settings are efficient and proportionate. Most of the initiatives below are not new, and this plan provides further detail on areas of focus and updates to timeframes.

As always, APRA will remain adaptable to changes in the external environment and will adjust these priorities as needed to ensure the industries it regulates can continue to respond to new and emerging risks.

Having spent more than a decade building up the strength of the prudential framework, APRA is now in a position to focus on maintaining that strength. Last year, we reduced our policy changes by more than half, having finalised the implementation of government recommendations for large and comprehensive reforms under the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. This year, we continue to prioritise targeted improvements to our standards, to maintain resilience as the risk outlook evolves.

Maintaining resilience requires a strong day-to-day supervisory focus, both at the individual entity and industry-wide levels. At an individual entity level, APRA’s supervisory programs continue to reflect the particular risks that entities are exposed to, with a focus on intervening early to resolve issues. Outlined below are APRA’s policy, supervisory and data priorities at an industry-wide level, for maintaining financial and operational resilience.

Policy priorities

APRA’s policy priorities are directed at targeted changes to reinforce banks’ financial resilience:

- Bank capital instruments: Following extensive consultation last year, APRA plans to finalise proposed revisions to its capital standards in the first half of 2025-26. These changes will remove Additional Tier 1 capital from the banking prudential framework to ensure that capital instruments can fulfill their intended role in absorbing losses during periods of stress. The updated capital framework will take effect from 1 January 2027.

- Bank liquidity framework: In the second half of 2025-26, APRA plans to commence engagement with industry on potential revisions to the bank liquidity framework. This initiative aims to modernise the framework in response to evolving risks. APRA will also seek to incorporate relevant findings from the CFR review into small and medium-sized banks.

Supervisory priorities

A significant component of APRA’s day-to-day supervision is focused on assessing potential risks to financial resilience. APRA’s regular supervisory activities include frequent monitoring of financial viability and capital adequacy, with a focus on banks’ internal capital models and heightened supervisory attention on areas of concern in liquidity, credit, investment, and insurance risk. At an industry-wide level, a key supervisory priority is strengthening crisis preparedness:

- Recovery and exit planning: APRA will maintain close oversight of industry’s implementation of Prudential Standard CPS 190 Recovery and Exit Planning. This standard requires all regulated entities to prepare for stress events that could threaten their viability. APRA will assess how banks and insurers have addressed APRA’s feedback from last year’s supervisory reviews, which identified several areas for improvement. Superannuation trustees will be required to formally submit their recovery and exit plans to APRA for the first time this year. APRA will review these plans and provide feedback, where appropriate.

- Resolution planning: As Australia’s resolution authority, APRA plays a critical role in preparing for the potential failure of regulated entities to minimise losses to beneficiaries and limit disruption to the broader financial system. Over the coming year, APRA will continue working with 14 entities to develop and refine bespoke resolution plans. The introduction of Prudential Standard CPS 900 Resolution Planning in 2024 formalised obligations for larger and more complex entities to support APRA in this process, where requested.

- Crisis simulations: APRA will collaborate with the other CFR members - the Australian Securities and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank of Australia (RBA) - to conduct a crisis simulation exercise to test agency communication responses to a hypothetical bank failure.

Data priorities

Reporting standards: To reflect proposed changes to Additional Tier 1 capital in the broader banking prudential framework, APRA will make corresponding updates to its reporting standards. In the first half of 2025-26, APRA plans to finalise revisions to Reporting Standards: ARS 110.0 Capital Adequacy; ARS 221.0 Large Exposures; and ARS 222.0 Exposures to Related Entities.

Operational resilience

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Policy | Refresh Governance standards | ✓ | ✓ | ✓ |

|---|

| Supervision | Assess entity implementation of APRA’s new operational resilience standard | ✓ | ✓ | ✓ |

|---|

Policy priorities

APRA’s policy priorities are focused on strengthening governance practices across all its regulated industries:

Governance: In the second half of 2025-26, APRA plans to consult on draft standards and guidance to update core governance requirements. These changes aim to address persistent poor practices and establish clear expectations for all regulated entities – almost 80 per cent of entities currently under heightened supervision by APRA exhibit underlying governance issues. To inform these revisions, APRA is continuing to engage extensively with stakeholders to gather diverse perspectives.

Supervisory priorities

APRA’s supervisory priorities are focused on strengthening all regulated entities’ resilience to operational risks:

Operational resilience: On 1 July 2025, Prudential Standard CPS 230 Operational Resilience (CPS 230) came into effect, introducing enhanced requirements for operational risk management across all regulated entities. Given the growing reliance on third parties, rapid technological advancements and geopolitical uncertainty, effective implementation of CPS 230 is critical to maintaining financial safety and stability. Over 2025-26, APRA will engage with entities to ensure they are meeting their new obligations. APRA’s supervision program will initially focus on the largest entities (significant financial institutions), including through targeted prudential reviews of some entities.

2. Responding to significant and emerging risks

As a forward-looking and proactive regulator, much of APRA’s impact is achieved through working cooperatively with entities to identify and rectify problems before they cause harm.

In the current environment, we are particularly focused on potential risks from geopolitical tensions, cyber-attacks, interconnections, an ageing population and climate change. We are also closely monitoring potential vulnerabilities that could emerge in banks’ housing lending portfolios as interest rates decline.

System-wide risk

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Supervision | System stress test | ✓ | ✓ | - |

|---|

| Geopolitical risk workplan | ✓ | ✓ | ✓ |

| Macroprudential policy | ✓ | - | - |

Supervisory priorities

- System stress test: In the second half of 2025-26, APRA will publish the results of its inaugural system stress test, designed to evaluate risks to financial stability arising from interconnectedness in the financial system. The test scenario assesses the impact and potential feedback loops between the banking and superannuation sectors from a significant financial market disruption alongside a major operational risk event. APRA will collaborate with industry and regulatory peers to address any vulnerabilities identified through this exercise.

- Geopolitical risk: APRA is working closely with the banking industry and regulatory peers to enhance the financial system’s preparedness for a geopolitical risk event. A dedicated geopolitical risk workplan has been developed, initially focusing on targeted engagements with banks throughout 2025-26 – this will be followed by further work across other industries. APRA’s workplan aims to identify gaps in preparedness and strengthen resilience across a range of scenarios. This initiative forms a key part of the CFR’s broader workplan, announced in December 2024.

- Macroprudential policy: Under Prudential Standard APS 220 Credit Risk Management, banks are required to be pre-positioned to implement a range of credit-based macroprudential measures, if needed, to address risks to financial stability. Given the potential for risks in housing lending to build as interest rates decline, APRA will be engaging with banks on implementation aspects of different macroprudential tools during the first half of 2025-26.

Cyber resilience

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Supervision | Strengthen regulated entities' cyber resilience | ✓ | ✓ | ✓ |

|---|

| Enhancing government and industry response to cyber incidents | ✓ | ✓ | ✓ |

| Address systemic cyber vulnerabilities | ✓ | ✓ | ✓ |

| Assess potential risks associated with the use of artificial intelligence (AI) | ✓ | ✓ | ✓ |

Supervisory priorities

- Strengthening regulated entities' cyber resilience: In 2025–26, APRA will prioritise targeted supervisory engagements to assess entities progress in uplifting cyber resilience. These engagements will focus on evaluating specific cyber control areas and identifying potential single points of failure within entity systems, processes and dependencies. Initial efforts will concentrate on superannuation trustees, insurers and smaller banks. In the superannuation sector, a key focus will be assessing funds’ responses to APRA’s concerns outlined in its June 2025 letter on Information Security Obligations and Critical Authentication Controls.

- Enhance government and industry response to cyber incidents: Effective cyber incident response requires strong coordination between industry and government. A key priority for APRA is working with regulatory peers to strengthen incident response protocols, including improvements to information-sharing arrangements. This will be supported by the design and execution of simulation exercises to test whole-of-government responses to cyber events. APRA will continue its collaboration with the CFR Cyber and Operational Resilience Working Group to advance system-wide resilience.

- Address systemic cyber vulnerabilities: APRA will work with entities to develop a system-wide view of entities’ reliance on third party service providers. With increasing reliance on third parties for critical functions, including technology, there is the potential for disruptions outside the financial sector to present risks to financial stability. All entities will be required to submit a register of their material service providers by 1 October 2025.

- Assess emerging risks associated with the use of AI: In the first half of 2025-26, APRA will undertake targeted supervisory engagements with a group of larger entities to understand better emerging practices and potential risks associated with AI. These engagements will assess the appropriateness of risk management and oversight practices to support responsible adoption of AI across the financial system.

Improved outcomes for superannuation members

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Supervision | - APRA and ASIC retirement income covenant pulse check

- Intensified supervision of expenditure

- Review of investment governance and member outcomes of platform products

| - | ✓ | - |

|---|

| Data | - Retirement reporting framework

- Integration of retirement product data into the 2026 Comprehensive Product Performance Package.

| - | ✓ | - |

|---|

Supervisory priorities

- Retirement income covenant pulse check report: In the first half of 2025-26, APRA and ASIC will jointly release a pulse check report evaluating industry progress in implementing the retirement income covenant. Previous reviews identified significant variability in how the covenant was adopted, with some entities demonstrating a lack of urgency in embracing its intent. This pulse check will assess industry’s progress in implementing their retirement income strategies, aimed at supporting improved outcomes for members in retirement.

- Intensified supervision of expenditure: Fund-level expenditure will remain a key focus to ensure superannuation trustees act in the best financial interests of their members. Over the next 12 months, APRA will undertake targeted assessments of expenditure data, and where deficiencies are identified, trustees will be required to make improvements.

- Targeted review of platform products: APRA is currently undertaking a review to assess the quality and soundness of trustees’ governance and oversight of investments offered via platforms. The review focuses on key areas including due diligence, onboarding, monitoring, and removal of investment options, as well as strategic planning and practices to promote member outcomes. APRA will assess current practices against relevant prudential standards. APRA’s findings will be shared with the superannuation industry, highlighting areas where enhancements are expected.

Data priorities

- Retirement reporting framework: APRA is working with Treasury to design a new reporting framework on retirement outcomes, which would commence in 2027. This initiative will enable monitoring of the outcomes delivered to members in retirement in a consistent and transparent way.

- 2026 Comprehensive Product Performance Package (CPPP): Following the release of retirement reporting data in mid-2025, APRA will integrate this data into the CPPP from the second half of 2025-26. This will provide a more comprehensive view of product performance across the superannuation sector.

Climate risk

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Supervision | Insurance Climate Vulnerability Assessment | - | - | ✓ |

|---|

Supervisory priorities

Climate Vulnerability Assessment: In the second half of 2025-26, APRA plans to release the results of its Climate Vulnerability Assessment for the general insurance sector. This assessment has involved Australia’s five largest general insurers and has included detailed analysis of granular, modelled premium data. The findings will provide governments, insurers, policyholders, and the broader community with a clearer understanding of how general insurance affordability may evolve over the medium term in response to the physical and transition risks associated with climate change.

3. Getting the balance right

Under APRA’s mandate, we must balance our financial safety and stability objectives with competition and efficiency considerations. We take this obligation seriously. APRA has a long-established framework to minimise any undue cost of regulation for industry. By design, our prudential standards avoid overly prescriptive requirements which would otherwise stymie innovation and increase compliance costs. We are risk-based and proportionate.

Our framework is also subject to regular review. Most recently, the CFR and ACCC assessed Australia’s regulatory framework for small and medium-sized banks, finding that frameworks were broadly fit for purpose and also highlighting some areas for improvement. Later this year, APRA’s framework will again be subject to an independent review by the International Monetary Fund under its Financial Sector Assessment Program.

As productivity concerns have become more pronounced economy-wide, we have increased our focus on competition and efficiency considerations. In recent years we have progressed a more targeted policy agenda, worked more collaboratively with industry on policy reforms, strengthened our coordination with other agencies, and ceased certain data collections.

This year – under this new objective – we are progressing nine actions to further minimise burden on industry. Some of these are actions that APRA committed to as part of the CFR review into small and medium-sized banks. Others are broader initiatives, which impact additional industries.

In terms of impact, many of our actions are incremental – they build on existing proportionality in the framework. In aggregate, APRA estimates that its actions will moderately reduce the burden for the financial sector and, at the margin, help to free up capital for other productive purposes.

In addition to the actions outlined below, APRA is also making changes to strengthen competition and efficiency considerations in our internal decision making and culture. This work is more forward looking – it aims to ensure we continue to strike the right balance over the longer-term. We are introducing new public performance measures to strengthen our public accountability (see Performance Measures).

Summary of priorities by industry| | Activity | BNK | SUP | INS |

|---|

| Policy | Introducing further proportionality | ✓ | ✓ | ✓ |

|---|

| Simplifying the bank licensing framework | ✓ | - | - |

| Promoting access to internal capital modelling | ✓ | - | - |

| Promoting access to cost-effective reinsurance | - | - | ✓ |

| Reducing capital requirements for annuities | - | - | ✓ |

| Removing unnecessary or duplicative rules | ✓ | ✓ | ✓ |

| Coordinating with peer agencies on payments reform | ✓ | - | - |

| Supervision | Providing greater clarity of supervisory expectations relating to bank capital adjustments | ✓ | - | - |

|---|

| Data | Strengthening data sharing with other agencies | ✓ | ✓ | ✓ |

|---|

Policy priorities

- Introducing further proportionality: In the first half of 2025-26, APRA will consult on a proposal to formalise a third tier into our proportionality framework for banks. APRA’s existing policy framework is based on a two-tier system that differentiates prudential requirements between significant financial institutions (SFIs) and non-SFIs. A third tier will allow APRA to introduce more nuance into its prudential requirements of banks, reflecting different business models. Following APRA’s consultation with banks, APRA plans to turn its focus to the insurance and superannuation frameworks.

- Simplifying the bank licensing regime: In July 2025, APRA commenced consultation on proposed changes to its bank licensing regime. While APRA cannot control the flow of new applicants, it is important that our processes are as efficient as possible to give new entrants the best possible chance of success. Our goal is to reduce the time taken to process new bank license applications by around half, through providing greater clarity on APRA’s expectations and introducing greater formality within the framework.

- Promoting access to internal capital modelling: In the first half of 2025-26, APRA will consult on changes that aim to simplify and clarify our accreditation process that allows banks to use internal modelling for regulatory capital purposes. The use of internal models can result in moderately lower capital requirements, where banks can demonstrate sophisticated risk management. APRA’s proposed changes aim to improve transparency and implementation flexibility.

- Promoting access to cost-effective reinsurance: APRA is currently consulting with general insurers on ways to maintain access to affordable and appropriate reinsurance in the face of rising global costs. APRA will release further details on its proposals in the first half of 2025-26.

- Reducing capital requirements for annuities: APRA is currently consulting on a proposal to reduce prudential capital requirements for life insurers offering annuity products. APRA’s aim is to moderately lower the cost to life insurers of providing annuity products, helping to attract participants and support growth in the market. APRA plans to finalise its proposed changes in the second half of 2025-26.

- Removing unnecessary or duplicative rules: As part of APRA’s consultation on governance standards (see Strategic objective: Maintaining financial and operational resilience), APRA is exploring with industry opportunities to remove outdated or duplicative requirements. A key focus is addressing overlaps between reporting obligations under APRA’s fit and proper requirements and statutory obligations under the Financial Accountability Regime.

- Coordinating with peer agencies on payments reform: APRA will continue to work closely with government on proposed reforms to the regulation of Stored Value Facilities (SVF). These reforms aim to simplify the existing regulatory framework, to better support innovation and competition. Under the new regime, APRA plans for its prudential requirements of SVFs to be more streamlined than for banks, consistent with relative risks. Following the establishment of the legislative framework for SVFs, APRA intends to consult on new prudential standards. The timing of consultation on draft legislation will be determined by the government.

Supervision priorities

Providing greater clarity of APRA’s supervisory expectations relating to capital adjustments: Throughout 2025-26, APRA will begin implementing changes to how it communicates with banks regarding adjustments to minimum capital requirements. These changes will provide banks with greater clarity on the reasons for the adjustment and the outcomes needed to address APRA’s concerns. APRA’s goal is that banks will be better able to take action to have capital adjustments lowered or removed. This work will complement broader initiatives to provide greater transparency of supervisory expectations across all industries, including communications on supervisory engagements.

Data priorities

Strengthening data sharing with other agencies: APRA will continue to explore opportunities to share data with other regulators, helping to reduce duplicative requests on entities.

4. Improving our organisational effectiveness

As the primary data collection authority for Australia’s financial system, APRA’s data collection responsibilities have expanded significantly in recent years. This growth reflects both emerging risks to the financial system, and new government policy initiatives, such as the superannuation performance test.

Like many public and private sector organisations, APRA has also intensified its focus on strengthening the resilience of its technology and data infrastructure in response to the increasing frequency and sophistication of cyber threats.

Unlocking the value of AI for APRA’s organisational effectiveness will be a key priority. APRA is well positioned to utilise AI to strengthen its regulatory and oversight capabilities, optimise existing resources and support innovation. APRA’s approach will build on existing foundations in a balanced way.

Recognising the broader scope of APRA’s role and the evolving operating environment, the Australian Government committed $73.2 million in additional funding through the FY2024-25 Federal Budget to enhance APRA’s data capabilities.

This funding will support five key initiatives aimed at strengthening APRA’s technology and data infrastructure. These investments also aim to equip APRA’s people with the data and insights needed to drive continued excellence in supervision.

- Implementing a secure cloud-based platform: By December 2025, APRA will launch a new cloud-based platform to support both current and future data collections. This platform will significantly enhance data analytics capabilities, delivering deeper and more timely insights. It will also improve data accessibility for supervisors, enabling more timely decision-making.

- Finalising the transition to APRA Connect: By December 2027, APRA plans to fully transition all data collections to APRA Connect and retire its legacy systems. The current platform requires substantial manual effort and validation, and this shift is expected to significantly reduce the compliance burden on industry. APRA estimates long-term savings for industry at approximately $6 million annually.

- Strengthening data governance and data management: APRA has established a Data Council of senior executives to oversee APRA’s data priorities. A key area of focus is identifying data collections that could be retired or streamlined to reduce burden on industry.

- Enhancing cyber security and privacy controls: APRA is strengthening its cyber security and privacy practices in alignment with key government frameworks and the Privacy Act. Ongoing improvements to existing controls are focused on safeguarding sensitive information and systems. Priority areas include the Australian Signals Directorate’s ‘Essential Eight’, the Protective Security Policy Framework, and the Australian Privacy Principles.

- Upgrading supervision management systems: To support integrated analytics, streamlined reporting and improved efficiency, APRA is implementing an enhanced supervision management system. The new platform is scheduled to go live in November 2025.

APRA’s people: Building capability in an inclusive and agile organisation

APRA relies on the expertise and judgement of its people to achieve its objectives. APRA has a highly engaged workforce, with a strong commitment to purpose. To maintain a highly engaged, capable and adaptive workforce, APRA will continue to:

- Invest in leadership skills and capabilities: APRA is empowering its people to grow as confident leaders while deepening their expertise in supervision, risk, data and policy. The investment reflects our commitment to building a future-ready organisation with leadership behaviours reinforced through training, leadership role modelling and clear performance expectations.

- Foster an inclusive culture: APRA will continue to enhance our position as a leading, inclusive employer. We will consult with staff in updating our Inclusion and Diversity strategy, building on our successes, and embracing future ways of working.

- Sharpen our approach to remuneration: We are reviewing the framework and increasing transparency of our approach to remuneration, whilst strengthening alignment of capability needs and individual performance.

Supervision excellence

In a rapidly complex and dynamic operating environment, APRA must continue to evolve and strengthen its supervisory capability. The ability to respond swiftly and effectively to emerging risks depends on having skilled supervisors with deep expertise. To support this, APRA will continue to invest in its people and tools through the following initiatives:

- Building capability: to enhance supervisory and industry expertise, APRA will establish a supervisory development centre. Building on existing training programs, this will deliver immersive, scenario-based training designed to empower supervisors with the skills and confidence to navigate complex challenges. The focus will be on strengthening core supervision capabilities and fostering continuous professional growth.

- Smartening our supervision tools: APRA is strengthening its data analytics and data science capabilities, enabled by an enhanced technology toolkit. These changes will equip supervisors with real-time information and insights across entities, industries and geographies.

- Sharpening frameworks and methodology: APRA will continue to review and refine its supervision framework to ensure our methodologies remain fit for purpose and aligned with the evolving risk landscape.