A more efficient and transparent bank licensing framework

Executive summary

Consistent with APRA’s strategic objective of ‘getting the balance right’, APRA’s 2025-2026 Corporate Plan announced a key policy priority of simplifying APRA’s bank licensing framework.1 The Corporate Plan stated that while APRA cannot control the flow of new applicants, it is important that its processes are as efficient as possible to give new entrants the best possible chance of success and to support competition in the banking sector.

Simplifying the bank licensing process also implements Action 6 of the Council of Financial Regulator’s Review into Small and Medium-sized Banks (CFR Review). This stated that APRA would update its authorised deposit-taking institutions (ADI) licensing framework to make the application process more transparent and efficient.2

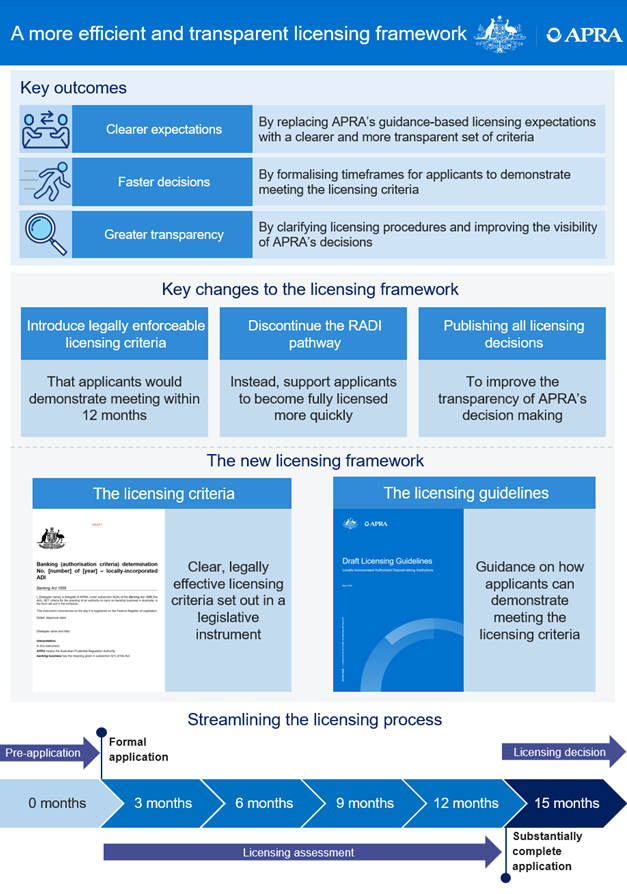

APRA published a discussion paper last year proposing changes to the ADI licensing framework.3 APRA is now seeking feedback on the new draft licensing framework, which has been published alongside this paper. The objectives of these reforms include:

- Clearer expectations, by replacing APRA’s guidance-based licensing expectations with a clearer and more transparent set of legally effective criteria.

- Faster decisions, by setting out timeframes for applicants to demonstrate meeting the licensing criteria and for APRA to make licensing decisions.

- Greater transparency of the licensing process, by clarifying licensing procedures and improving the visibility of APRA’s decisions.

A prudent licensing framework underpins financial safety, system resilience and depositor protection. While the reforms aim to improve the transparency and efficiency of the ADI licensing process, they do not diminish APRA’s expectations that ADIs uphold robust regulatory standards necessary for undertaking banking business while protecting depositors.

Key changes to the licensing framework

APRA’s 2025 discussion paper outlined proposals aimed at improving the clarity and efficiency of the licensing process for locally-incorporated ADIs. The three key changes to the ADI licensing framework that APRA proposed included:

- Replacing the existing guidelines with legally effective licensing criteria. Applicants must demonstrate that they meet the ADI Licensing Criteria within 12 months of submitting a licensing application.

- Discontinuing the Restricted ADI (RADI) pathway given its limited take-up and the challenges that new entrants using this pathway have faced in developing sustainable business models.

- Publishing all licensing decisions including refusals, to improve the transparency of APRA’s decision-making.

Feedback to APRA’s consultation was broadly supportive, particularly for setting targeted, outcomes-based and timebound licensing criteria. APRA is therefore proceeding with these proposals.

A summary of feedback received and APRA’s responses is provided in Attachment A to this consultation paper.

A more efficient and transparent licensing framework

This consultation paper seeks feedback on the draft licensing framework, which has been published alongside this consultation paper. The framework comprises:

- ADI Licensing Criteria – the ADI Licensing Criteria will consist of clear, legally effective criteria, set out in a legislative instrument. Applicants that are locally-incorporated bodies corporate must demonstrate that they meet the criteria within 12 months of submitting their licence application.

- ADI Licensing Guidelines – the ADI Licensing Guidelines will provide additional information and guidance on how APRA expects applicants to demonstrate that they meet the licensing criteria. While the guidelines frequently discuss legal requirements, they do not create enforceable requirements.

In addition to updating its licensing requirements, APRA aims to improve the clarity of the licensing process by refreshing the information provided to applicants. Attachment B to this consultation paper sets out proposed draft information on the licensing process. This information will be finalised and published on APRA’s website, alongside the final licensing framework, later in 2026.

The draft licensing framework released alongside this consultation paper applies to applicants seeking to establish locally-incorporated ADIs. APRA plans to separately revise its approach to licensing foreign ADI branches, recognising their distinct business model and risk profiles, following the finalisation of the licensing framework for locally-incorporated ADIs.

Next steps

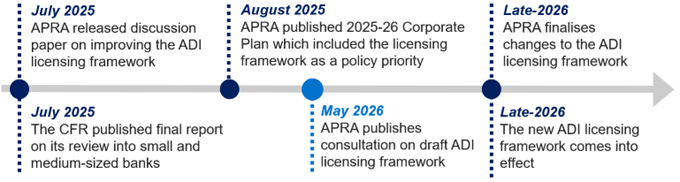

Written submissions should be provided to APRA by 31 July 2026. After considering feedback, APRA aims to publish the final licensing criteria and guidelines in late-2026. The new licensing framework will replace APRA’s existing ADI licensing guidelines.

Figure 1. Timeline for reform

Chapter 1 of this paper provides an overview of the licensing framework reforms. Further detail on the ADI Licensing Criteria and ADI Licensing Guidelines is provided in Chapter 2. Consultation details are provided in Chapter 3.

Chapter 1 – Overview

This chapter provides an overview of APRA’s ADI licensing framework reforms. It outlines issues with the existing licensing framework, sets out the key solutions to address these issues, and proposes transition arrangements.

Licensing challenges

APRA’s existing licensing framework was introduced in 2018. APRA has issued 17 new ADI licences under this framework, with roughly half of these granted to domestic start-up companies.

The existing licensing framework has been effective in supporting new entrants into the banking sector while maintaining APRA’s robust prudential requirements. However, APRA’s experience is that the licensing process can be lengthy and resource intensive, with iterative engagements and protracted assessment timeframes. While it is important that APRA’s ADI licensing framework reinforces APRA’s prudential expectations for regulated entities, there is scope to improve its clarity, transparency and efficiency.

In 2025, APRA reviewed its licensing framework to determine whether it remained fit for purpose. This review, combined with feedback from past applicants, found three key challenges with the licensing framework that have created barriers to accessing the banking sector.

Challenge 1 – Unclear licensing expectations

APRA’s licensing framework requires applicants to demonstrate they have appropriate resources, experience and operational readiness to prudently undertake banking business. This ensures that newly licensed ADIs can operate in a safe and sustainable manner, which protects depositors.

APRA’s licensing expectations are currently set out in broad guidelines, which can be challenging for applicants to navigate. For some applicants, this has led to protracted licensing assessment timeframes. This challenge has been particularly acute for smaller start-up companies.

Challenge 2 – Limited effectiveness of the RADI pathway

The RADI pathway was introduced in 2018 with the aim of facilitating market entry by small start-up companies. APRA’s experience has been that while the RADI pathway initially helped encourage new bank entrants, in recent years, the pathway has not been as simple and effective as intended. This is reflected in its limited take-up.

Many RADI applicants encountered difficulties transitioning to an ADI licence and feedback has been that a simpler and clearer pathway to gaining an ADI licence is preferred.

Challenge 3 – Uncertain licensing timeframes

Recent applicants have also provided feedback to APRA that licensing timeframes are not always clear. For example, it can be difficult to know when an application will be approved given the often-iterative process involved in meeting APRA’s licensing expectations. Additionally, the current licensing framework does not contain clear deadlines for licensing assessments and decisions.

Uncertain timeframes create burden for applicants, slows down the licensing process and creates barriers to enter the banking sector.

Addressing these challenges

Consistent with this feedback, APRA is proceeding with three substantial changes to the existing licensing framework. These changes aim to better facilitate entry to the banking sector, while retaining APRA’s high expectations for prudentially regulated entities.

Solution 1 – Replace the existing licensing guidelines with clearer, legally effective licensing criteria

APRA is replacing the existing licensing guidelines with clearer licensing criteria, which will be set out in a legislative instrument. The ADI Licensing Criteria will provide a more transparent set of requirements that applicants must demonstrate they meet before being authorised. Explicit and measurable requirements will clarify expectations and support more efficient engagement with APRA during the licensing process. Applicants will be better positioned to plan, allocate resources and develop the necessary capabilities ahead of submitting a formal application.

To support applicants in demonstrating how they meet the criteria, APRA will also publish ADI Licensing Guidelines. These guidelines will not contain legally enforceable requirements but will instead provide information on APRA’s expectations to support applicants in demonstrating that they meet the licensing criteria.

Further detail on the ADI Licensing Criteria and Licensing Guidelines is provided in Chapter 2.

Solution 2 – Discontinue the RADI pathway

Consistent with feedback to APRA’s 2025 discussion paper, APRA is discontinuing the RADI pathway. All applicants will now be subject to the same licensing criteria.

While the RADI pathway will be discontinued, the revised framework will continue supporting smaller start-up companies. Clearer and more transparent criteria will improve all applicants’ understanding of APRA’s expectations, while more streamlined and predictable licensing timeframes will address challenges with sustaining operations throughout the licensing process.

While all applicants will face the same minimum licensing criteria, the licensing assessment will consider the size, scale, complexity, and risk of an applicant’s proposed business. For example, applicants with more established or complex business models, such as existing non-bank financial institutions with sizeable loan portfolios, may be required to demonstrate a higher level of maturity in areas such as governance, risk management and operational capability compared to smaller, start-up companies. This aligns with APRA’s risk-based approach to prudential regulation.

Following authorisation, new entrants will most likely be subject to APRA’s prudential framework for non-Significant Financial Institutions.4 This framework supports competition by reducing regulatory burden for smaller ADIs.

Solution 3 – Clearer deadlines and more transparent decisions

To ensure prompt consideration of applications and certainty over the timing of licensing decisions, APRA will implement a 12-month period for an applicant to demonstrate that they meet the ADI Licensing Criteria, with an option for extension in exceptional circumstances.

In combination with the 12-month assessment timeframe, APRA will extend its practice of publishing successful ADI licence applications to all ADI licensing decisions. Publishing all licensing decisions will support more transparent decision-making and remove the risk that applications continue without a clear end. Refused applicants will be informed of the specific licensing criteria they have not demonstrated.

The outcome of applications that are withdrawn prior to APRA making a licensing decision will not be published.

Transition arrangements

To ensure a clear transition to the new licensing framework, all applicants will be subject to the new ADI Licensing Criteria when the legislative instrument comes into effect. This includes applicants that have applied under the existing framework.

While all applicants will be subject to the new ADI Licensing Criteria, there will be some minor differences in the timing to demonstrate meeting the criteria between these applicants.

Existing applicants

Applicants that have lodged a formal application under the existing framework that have not yet been granted a licence, and new applicants that are expecting to lodge an application before the new framework comes into effect, will be assessed under the new licensing framework. This is because the ADI Licensing Criteria will apply to all licensing applications upon commencement of the legislative instrument.

To ensure existing applicants have reasonable time to consider the new framework, these applicants will be permitted to demonstrate the ADI Licensing Criteria within 12 months from the date of the commencement of the legislative instrument, rather than from the date of lodging their application to APRA.

New applicants

Applicants that apply for a licence after the commencement of the legislative instrument will be subject to the new framework. These applicants are required to satisfy the ADI Licensing Criteria within 12 months from the date of lodging their application to APRA.

Applicants intending to apply for a licence under the new framework are encouraged to begin preparing their application with the draft licensing framework as a guide. These applicants are also encouraged to engage APRA early, with contact details provided in Chapter 4.

These transition arrangements are set out in the draft legislative instrument published alongside this consultation paper and would apply to both existing RADI and ADI applicants.

Chapter 2 – The revised licensing framework

This chapter provides an overview of the draft ADI Licensing Criteria and draft ADI Licensing Guidelines that will form the basis of the new licensing framework. The full draft ADI Licensing Criteria and ADI Licensing Guidelines have been published alongside this consultation paper, for feedback.

The ADI Licensing Criteria

The purpose of the new ADI Licensing Criteria is to codify APRA’s licensing expectations into a single legislative instrument with clear requirements. APRA expects applicants to, at a minimum, evidence meeting these requirements to demonstrate their ability to conduct banking business in a prudent manner. Following authorisation, ADIs are expected to maintain ongoing compliance with APRA’s prudential framework.

Codifying APRA’s licensing requirements in a legislative instrument will address feedback that APRA’s existing licensing process is unclear. The ADI Licensing Criteria will be publicly available, published on both APRA’s website and the Federal Register of Legislation. Applicants are required to demonstrate their capacity to meet the licensing criteria within 12 months of lodging an application.

A stylised example of how an applicant would engage with the new licensing framework is provided in Box A below, with more detail on the licensing process provided in Attachment B.

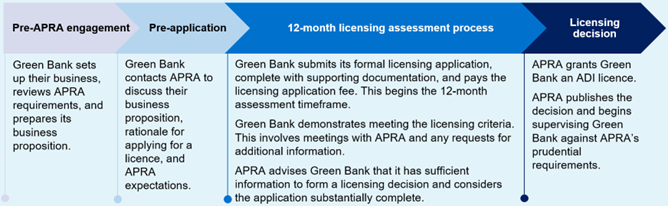

Box A. Green Bank: A quicker and more transparent licensing process

Green Bank is a locally-incorporated start-up company that is seeking an ADI licence to carry on banking business. It intends to apply for a licence under APRA’s new ADI licensing framework.

The following figure sets out a timeline of events for Green Bank to engage APRA, demonstrate that it meets the ADI Licensing Criteria, and receive an ADI licence to begin undertaking banking business.

Figure 2. Example licensing process

The ADI Licensing Criteria consists of two sections:

1. Authorisation criteria for a locally-incorporated ADI

This section sets out the licensing criteria that a locally-incorporated applicant must demonstrate to become licensed to carry on banking business in Australia. The ADI Licensing Criteria would require an applicant to:

- be structured and operate in a manner that APRA can effectively supervise;

- have sufficient financial and non-financial resources to prudently conduct banking business;

- have suitable skills and experience to prudently conduct banking business;

- maintain a risk management framework to prudently conduct banking business; and

- have credible plans for effectively responding to a stress that threatens its viability.

2. Timeframe to demonstrate meeting the ADI Licensing Criteria

This section details the requirement for applicants to demonstrate their capacity to meet the criteria within 12 months of submitting their application. APRA will have power to extend the timeframe in exceptional circumstances.

The ADI Licensing Guidelines

The ADI Licensing Guidelines aim to assist applicants in understanding how to meet the ADI Licensing Criteria and, more generally, to outline prudent practices for new entrant ADIs undertaking banking business. The ADI Licensing Guidelines should be read in conjunction with the ADI Licensing Criteria.

While the Licensing Guidelines discuss requirements from legislation, regulations and APRA’s prudential standards, the guidelines do not form part of the law, create enforceable requirements or contain legal advice. However, an applicant should consider the licensing guidelines to the extent they are relevant to its business model.

The Licensing Guidelines have been structured to provide guidance mapped to each licensing criterion. Excerpts from the ADI Licensing Criteria have been included in the guidelines, followed by accompanying guidance. This approach simplifies how applicants engage with the licensing framework.

Chapter 3 – Consultation details

After considering feedback, APRA intends to finalise amendments to the ADI licensing framework later in 2026. Further detail on the expected timeline is provided in the following table.

Table 1. Timeline for reform

| Timeline for reform | Date |

|---|---|

| Consultation package release | 13 May 2026 |

| Submissions deadline | 31 July 2026 |

| Final licensing criteria and guidance | Late 2026 |

Discussion questions

APRA welcomes feedback on the draft ADI Licensing Criteria and ADI Licensing Guidelines published alongside this consultation paper. In addition, APRA welcomes feedback on the specific policy questions provided in the table below.

Table 2. Discussion questions

| Questions |

|---|

|

|

|

|

|

Request for submissions and cost-benefit analysis information

APRA invites written submissions on the proposals set out in this Consultation Paper. Written submissions should be sent to licensing@apra.gov.au by 31 July 2026 and addressed to:

General Manager

Policy

Policy and Advice Division

Australian Prudential Regulation Authority

Important disclosure notice – publication of submissions

All information in submissions will be made available to the public on the APRA website, unless a respondent expressly requests that all or part of their submission is to remain in confidence. Automatically generated confidentiality statements in emails do not suffice for this purpose. Respondents who would like part of their submission to remain in confidence should provide this information marked as confidential in a separate attachment.

Submissions may be the subject of a request for access made under the Freedom of Information Act 1982 (FOIA). APRA will determine such requests, if any, in accordance with the provisions of the FOIA. Information in the submissions about any APRA-regulated entity that is not in the public domain and that is identified as confidential will be protected by section 56 of the Australian Prudential Regulation Authority Act 1998 and will therefore be exempt from production under the FOIA.

Request for cost-benefit analysis information

APRA asks that all stakeholders use this consultation opportunity to provide information on the compliance impact of the proposals, and any other substantive costs including business costs. Compliance costs are defined as direct costs to businesses of performing activities associated with complying with government regulation. Specifically, information is sought on any changes to compliance costs incurred by businesses as a result of APRA’s proposals.

Consistent with the Government’s approach, APRA will use the methodology behind the Regulatory Burden Measurement Framework to assess compliance costs. It is available at https://oia.pmc.gov.au/resources/guidance-assessing-impacts/regulatory-burden-measurement-framework.

APRA requests that respondents use this methodology to estimate costs to ensure the data supplied to APRA can be aggregated and used in an industry-wide assessment. When submitting cost assessments to APRA, respondents should include any assumptions made and, where relevant, any limitations inherent in their assessment. Feedback should address the additional costs incurred as a result of complying with APRA’s requirements, not activities that institutions would undertake due to foreign regulatory requirements or in their ordinary course of business.

Attachment A – Response to submissions

APRA received six submissions to its July 2025 consultation on improving APRA’s licensing framework. Non-confidential submissions have been published alongside this consultation paper. The following table summarises the feedback received in submissions and provides APRA’s response.

Table 3. Response to submissions

| Proposal | Stakeholder feedback | APRA response |

|---|---|---|

1. Develop formal, legally effective licensing criteria Set targeted and outcomes-based criteria in a legally effective legislative instrument, that applicants must meet within 12 months. | Broadly supportive. Requested further detail on the criteria and on what licensing milestones are required during the 12-month timeframe. Requested some flexibility in the 12-month deadline in specific circumstances. | Proceed with developing formal, legally effective licensing criteria. Applicants will have 12 months to demonstrate that they meet the criteria. In exceptional circumstances, APRA will have power to extend the timeframe if necessary. Develop guidelines that provide additional detail to support applicants in demonstrating that they meet the licensing criteria. |

2. Discontinue the RADI pathway Discontinue the RADI pathway given its limited take-up and the challenges it has faced to attract more new entrants into the banking sector. | Broadly supportive, with feedback from past RADI applicants agreeing that the pathway has experienced challenges in supporting entry of sustainable new banking businesses. In particular, RADI entrants found it difficult to maintain capital adequacy requirements over the 2-year RADI period and suggested a shorter licensing timeframe. | Proceed with the removal of the RADI framework, ensuring that the revised licensing framework is supportive of small, start-up entities seeking an ADI licence. |

3. Publish all licensing decisions, including refusals Publish all licensing decisions, including where a licence application is refused. APRA will not publish decisions if the applicant voluntarily withdraws their application ahead of APRA’s licensing decision. | APRA received limited feedback on this proposal. The feedback received sought clarification on the benefits of publishing licensing refusals. | Proceed with publishing licensing decisions, including refusals, to improve the transparency of the licensing process. |

Attachment B – The licensing process

This Attachment provides an overview of the licensing process to assist applicants prepare their applications and engage with APRA.

After considering feedback, APRA will finalise the information provided in this attachment and publish it on APRA’s website as part of the finalised ADI licensing framework later in 2026.

Overview

The licensing process involves five steps, which are summarised in the table below.

Table 4. The licensing process

| # | Step | Description |

|---|---|---|

| 1 | Pre-application | Preliminary consultation, allowing applicants to understand APRA’s expectations and identify potential issues. |

| 2 | Formal application | Applicant makes a formal application to APRA requesting authority to conduct banking business in Australia and pays the applicable application fee. The fees for licence applications are available on APRA’s website. |

| 3 | Assessment | The licensing assessment is the process for APRA to ensure the applicant meets the licensing criteria. This includes a review of the applicant’s business plan, policies and procedures, and onsite meetings. |

| 4 | Substantially complete application | An application is determined to be substantially complete once an applicant has demonstrated it has sufficient financial and non-financial resources and it has submitted all the expected supporting material, which is of sufficient quality and detail to allow APRA to complete its assessment. |

| 5 | Licensing decision | APRA grants or refuses the application for a licence and publishes its decision. APRA will aim to make the licensing decision within 90 days of determining an application to be substantially complete. |

Steps in the licensing process

This section provides a step-by-step overview of the five steps in the licensing process. Applicants are encouraged to familiarise themselves with these steps before engaging APRA.

Step 1 – Pre-application

Applicants should engage APRA before submitting a formal application. Pre-application discussions provide an opportunity to discuss the licensing process and APRA’s expectations. Additionally, APRA can better understand the applicant’s business strategy and raise any material issues or concerns. For example, pre-application discussions with an applicant may indicate that it would not be undertaking banking business and does not therefore require an ADI licence, or that its corporate structure must change to satisfy prudential requirements.

Table 5. Pre-application process

| Meeting | Purpose |

|---|---|

| Initial meeting |

|

| Business proposition review and feedback |

|

Step 2 – Formal application

After addressing feedback from the pre-application process, applicants should be ready to lodge a formal application. Applications should be made to APRA in writing with the necessary information and supporting documents.

APRA expects that documents provided in the application process should be final and approved by the relevant management and/or governance body.

When providing information to APRA, applicants should note that section 137.1 of the Criminal Code Act 1995 makes it an offence to give false or misleading information to a Commonwealth entity or to a person who is exercising powers or performing functions under, or in connection with, a law of the Commonwealth, or to omit any matter or thing without which the information is misleading. The penalty for this offence is 12 months imprisonment.

External advisors

Applicants may use external advisors for support in preparing their supporting information. Where applicants engage external consultants, APRA expects that the applicant reviews and understands the information provided by the consultants to ensure it accurately reflects the applicant’s strategy, business mix, risk profile, size and complexity. An applicant is ultimately responsible for how its frameworks operate and how risk is managed within its organisational structure and the information provided to APRA. APRA will test with an applicant, through discussions and onsite visits, how its frameworks will be implemented and used by the business.

Document submission

APRA uses a secure document portal for submission of applications and supporting material. Applicants must provide APRA with the details of the individuals who will be responsible for submitting the application. Access to the secure document portal will be arranged for the selected individuals representing the applicant.

Applicants must advise APRA as soon as possible if there are changes to information provided as part of the licensing application, noting applicants have 12 months to satisfy the ADI Licensing Criteria.

Each policy, procedure or other document should be submitted as a separate file, with a clear numbering system and document title to facilitate navigation of the documents. Where minimum supporting information is contained within another document its location should be clearly stated. APRA does not require applicants to submit hard copy documents.

While APRA will treat an applicant’s information in confidence, the information is not covered by the secrecy provisions in section 56 of the Australian Prudential Regulation Authority Act 1998 and could be subject to a Freedom of Information request. Applicants may therefore wish to submit all their documents to APRA as “commercial in confidence”.

Application fees

All applicants are required to pay an application fee prior to APRA commencing its formal assessment of their application. APRA will provide applicants with an invoice for the application fee once APRA has received the formal application.

The fees for licence applications are available on APRA’s website. Application fees are reviewed on a regular basis. APRA’s application fees, along with other charges and levies, are published in the annual Cost Recovery Implementation Statement.

In instances where an applicant’s organisational structure involves a holding company, APRA may require that the ADI have an authorised Non-operating Holding Company (NOHC). An authorised NOHC is subject to a licensing assessment and may incur a separate application fee.

Applicants should consider whether any person who holds or otherwise controls voting shares in the applicants will require an approval under the Financial Sector (Shareholdings) Act 1998 (FSSA).

All application fees are non-refundable regardless of the outcome of the application.

APRA will issue applicants with an invoice for the application fee and the account details to make the Electronic Funds Transfer (EFT). To facilitate this, applicants should provide APRA with the name of the company (the applicant), the applicant’s ABN and relevant contact details (name and position of contact, application address).

Withdrawing an application

An applicant may withdraw its application at any time. Withdrawal requests must be submitted to APRA in writing and signed by two senior officers of the applicant. APRA will not publish its licensing decision on a withdrawn application.

Withdrawal of an application does not prejudice any future applications the entity may make, given new applicants will, in most instances, be treated as a new application. However, the application fee is non-refundable so any subsequent application would be required to be submitted with the applicable fee.

Other regulators

Applicants will likely need to separately apply for licences or approvals for other non-APRA regulated activities to carry on their proposed business. For example, all ADIs require an Australian Financial Services Licence (AFSL) or an exemption from the Australian Securities and Investments Commission (ASIC). It is the applicant’s responsibility to ensure it applies for such licences or approvals.

APRA suggests that these are submitted to the respective regulatory body at the same time as the ADI application. APRA will communicate directly with ASIC, as well as other regulatory bodies such as AUSTRAC regarding the application.

Ownership of ADIs and their holding companies is governed by the FSSA which limits the control of a person, or group of associates, over the voting power in an ADI’s shares. A person or group who holds that voting power in excess of the relevant FSSA limit will need to apply to the Treasurer (or APRA, under a delegation from the Treasurer) for approval under the FSSA. This application should be submitted at the same time as the ADI licence application. It is the person’s responsibility to ensure they have the correct approvals under the FSSA and any other relevant legislation. APRA recommends that shareholders and any other persons with a controlling interest in an applicant should seek independent legal advice in this regard.

Assumption of restricted words and expressions

Applicants can start the licensing process with its existing company name (e.g. ‘Applicant Ltd’) and request approval from APRA to reserve with ASIC a company name containing a restricted term (e.g. ‘Applicant Bank Ltd’). Applications for consent to reserve a company name containing a restricted word or expression should only be made once a formal application for an ADI licence has been made to APRA and the appropriate licensing application fee paid.

Step 3 – Assessment

APRA’s assessment of a licence application will focus primarily on whether the applicant demonstrates that it meets the licensing criteria. Applicants are encouraged to utilise the ADI Licensing Criteria and the ADI Licensing Guidelines to ensure their application is adequate.

Proposed new ADIs differ widely in their scale, complexity and potential impact on the financial system. Consistent with APRA’s risk-based approach, the depth of APRA’s assessment against the ADI Licensing Criteria through the licensing process will be proportionate to the risks within the applicant’s business.

APRA breaks down assessment of the application into three distinct components:

- Formal application – This is where an applicant makes their formal application under section 9 of the Banking Act for authority to conduct banking business in Australia. If an applicant has not finalised some of the expected documentation when it submits its formal application, it should indicate when the finalised supporting information will be provided, noting applicants have 12 months from APRA confirming receipt of their formal application to demonstrate that it meets the ADI Licensing Criteria.

- Revised or additional information – APRA may require resubmissions and request additional material as it reviews a licensing application.

- Substantially complete application – Applications are substantially complete when APRA has sufficient documentation and evidence to determine whether an applicant has demonstrated that it meets the licensing criteria.

Once a formal application is received, APRA will review the information provided in the application and begin assessing the application against the licensing criteria. APRA will provide feedback on the application and may request additional information, hold meetings with the applicant and review aspects of the applicant’s operations onsite.

If an applicant makes material changes to its proposed business (for example, changes to its strategy, board, management, or legal structure) after APRA has determined the application to be substantially complete, APRA will assess the impact of the changes on the entity’s application. Applicants are expected to notify APRA if this occurs, noting they have 12 months to demonstrate that they meet the ADI Licensing Criteria and any material changes during the application process could impact the licensing timeframe.

Timeframe

When an applicant has lodged a formal licensing application and paid the licensing application fee, the 12-month timeframe for the licensing assessment begins. Applicants are expected to fund themselves throughout the licensing process. APRA cannot ‘fast-track’ applications where applicants have insufficient funds.

Document submission, review and feedback

APRA expects most of the required documentation to be submitted with the formal application. APRA allows flexibility for some material documentation to be submitted up to 3 months after application lodgement. On an exceptions basis and with APRA approval, applicants may submit some documentation up to 6 months after application lodgement. Further detail around required documentation is provided on APRA’s website and in the Licensing Guidelines.

If an applicant does not provide the required documentation within the timeframes provided by APRA, this restricts APRA’s ability to conduct the licensing assessment and APRA may refuse the application.

Document review and feedback by APRA is an iterative process that ensures submitted documents are of sufficient quality to demonstrate that the applicant can meet the ADI Licensing Criteria and comply with the Banking Act and the Financial Sector (Collection of Data) Act 2001 (FSCODA). APRA will typically not progress to onsite reviews or board meetings until a material proportion of the licence application has been assessed.

Information Technology (IT) resilience meetings

The IT resilience meetings assess the applicant’s IT infrastructure, IT security tools and controls, systems and timescales for implementation and testing, outsourcing arrangements and business continuity plans to ensure that these are fit for purpose.

APRA will also determine whether individuals responsible for the management of the applicant’s IT risk have the necessary skills, knowledge, and expertise. IT resilience meetings are dependent on the applicant’s IT system build. Applicants will likely meet with APRA to discuss IT resilience during the assessment process, with further meetings scheduled as necessary for APRA to gain assurance. Additional meetings are normally required where an applicant has unique or complex IT systems.

Board and management meetings

APRA will meet with individual members of management and the Board. APRA will assess whether management and the Board have the necessary skills and experience to prudently conduct banking business. APRA typically schedules the final meeting with the applicant’s Board towards the end of the licensing process to discuss any outstanding issues.

APRA will visit the applicant’s premises to assess resources and the applicant’s ability to operationalise. The visit will typically be scheduled in conjunction with the final meeting with the Board.

Following the final meeting with the Board, the applicant must submit a declaration of their current financial position. The declaration must include:

- the applicant’s most recent Common Equity Tier 1 capital position;

- the estimated monthly burn rate until six months post licensing;

- an estimate of how long initial regulatory capital is expected to remain above minimum requirements without additional capital raises; and

- the amount and timing of any expected capital raises up to and immediately after licensing.

APRA will not declare an application to be substantially complete if an applicant cannot demonstrate it has sufficient capital.

Step 4 – Substantially complete application

APRA will advise an applicant when it considers the application is substantially complete. Advising of the substantially complete application means that an applicant has provided sufficient documentation and evidence to APRA to make a licensing decision.

APRA will then, as soon as possible, publish a licensing decision on the licensing application. APRA will aim to make this decision within 90 days. Determination by APRA that an application is substantially complete does not prevent APRA requesting any further information it requires to make a final licensing decision.

Step 5 – Licensing decision

The assessment team prepares a recommendation of the licence application outcome for a senior APRA official not involved in the application process. Licensing application outcomes, including both granting and refusing to grant a licence, will be published by APRA on its website.

A decision to refuse an application under section 9 of the Banking Act is subject to Part VI of the Banking Act – Reconsideration and Review of decisions. Under Part VI a person who is dissatisfied with a decision may request APRA reconsider the decision. The request for APRA to reconsider must be made within 21 days of the date the person was notified of the decision and must set out the reasons for the request.

From receipt of a request to review a decision APRA has 21 days to confirm, vary or revoke its decision. If APRA does not confirm, vary or revoke its decision within this timeframe then its decision is taken to be confirmed.

If the applicant is dissatisfied with the outcome of APRA’s review they may make an application to the Administrative Review Tribunal for a review of APRA’s decision.

Footnotes

1 APRA, APRA Corporate Plan 2025-26 (Corporate Plan, August 2025)

2Council of Financial Regulators, Review into Small and Medium-sized banks (Final Report, July 2025)

3APRA, Improving the licensing framework for authorised deposit-taking institutions (Discussion Paper, July 2025)

4 In addition to APRA’s existing work on improving proportionality within the ADI prudential framework, APRA is also working closely with Treasury on a possible special regime for the smallest ADIs (which would likely include new entrant ADIs), further reducing regulatory requirements for this cohort.