Key statistics

| - | December 2024 | December 2025 | Year-on-year change |

|---|---|---|---|

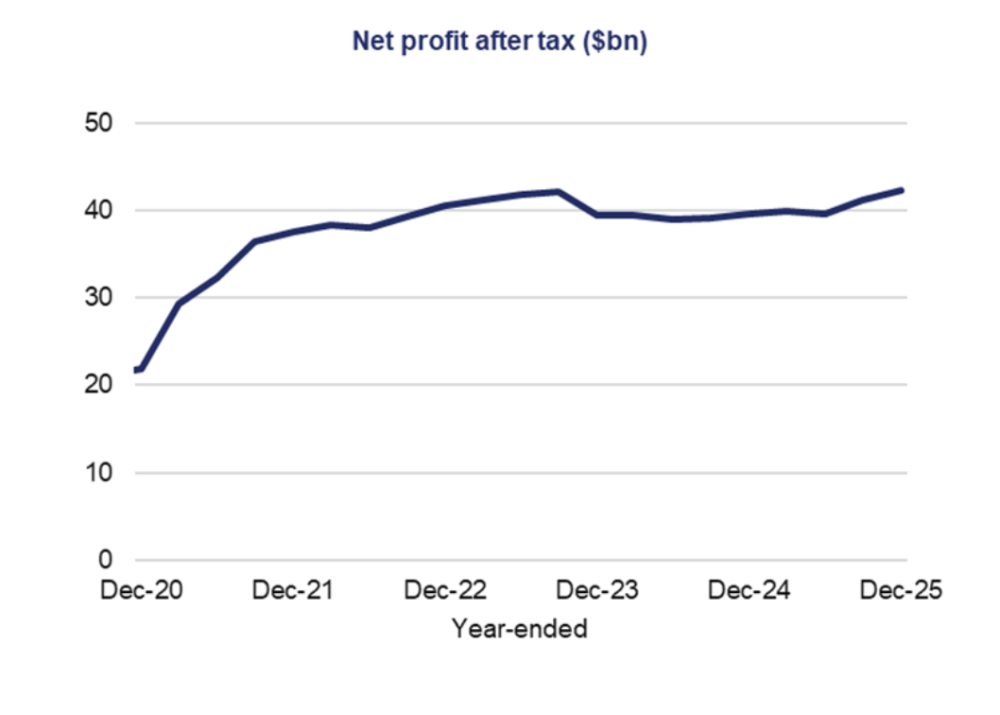

| Net profit after tax (year-end) ($bn) | 39.6 | 42.3 | 6.6% |

| Total assets ($bn) | 6,619.4 | 6,828.8 | 3.2% |

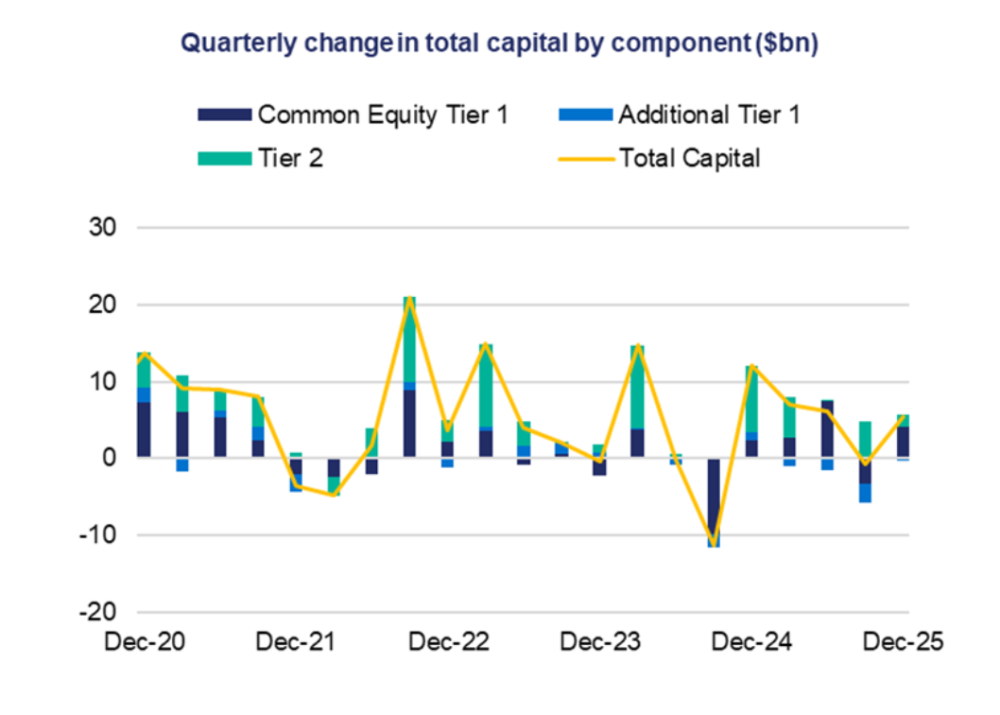

| Total capital base ($bn) | 449.6 | 467.5 | 4.0% |

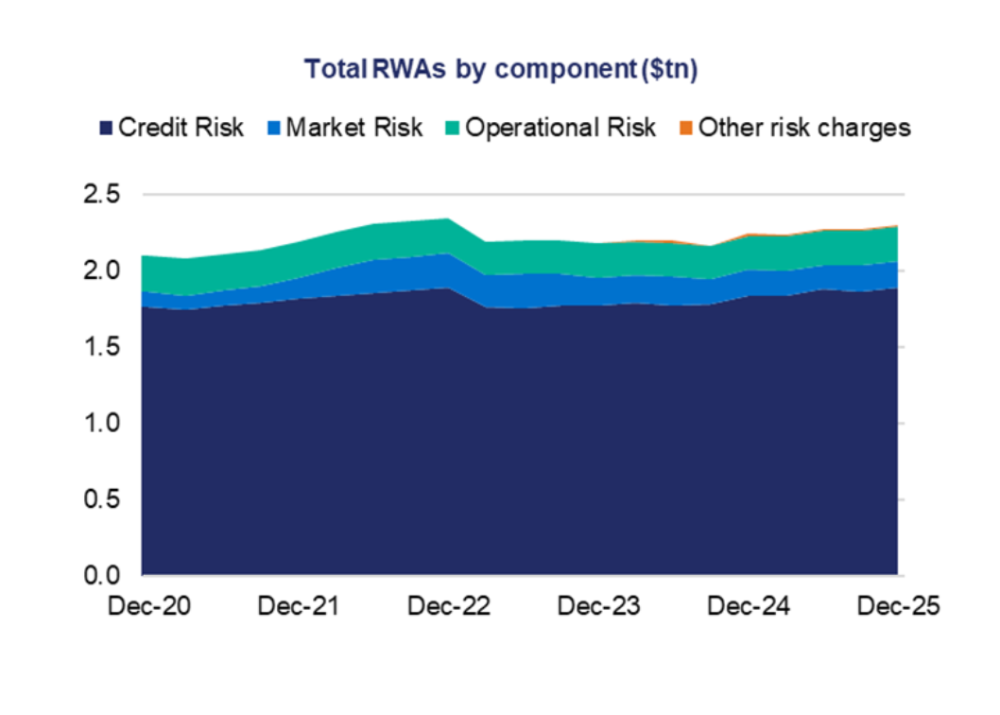

| Total risk-weighted assets ($bn) | 2,237.9 | 2,298.8 | 2.7% |

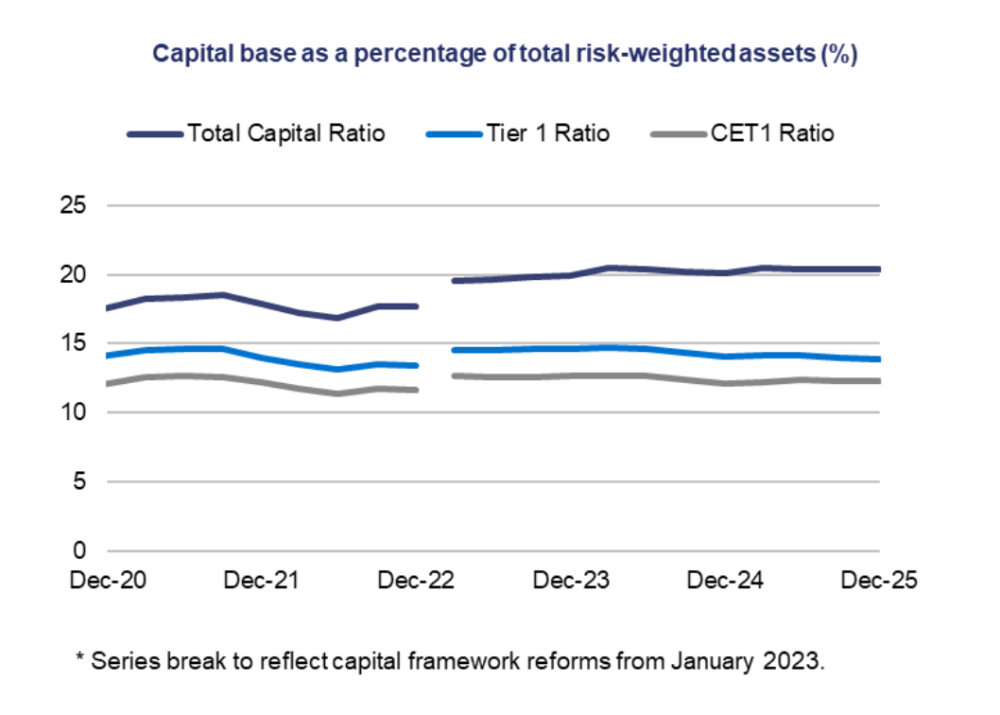

| Total capital ratio | 20.1% | 20.3% | 0.25 points |

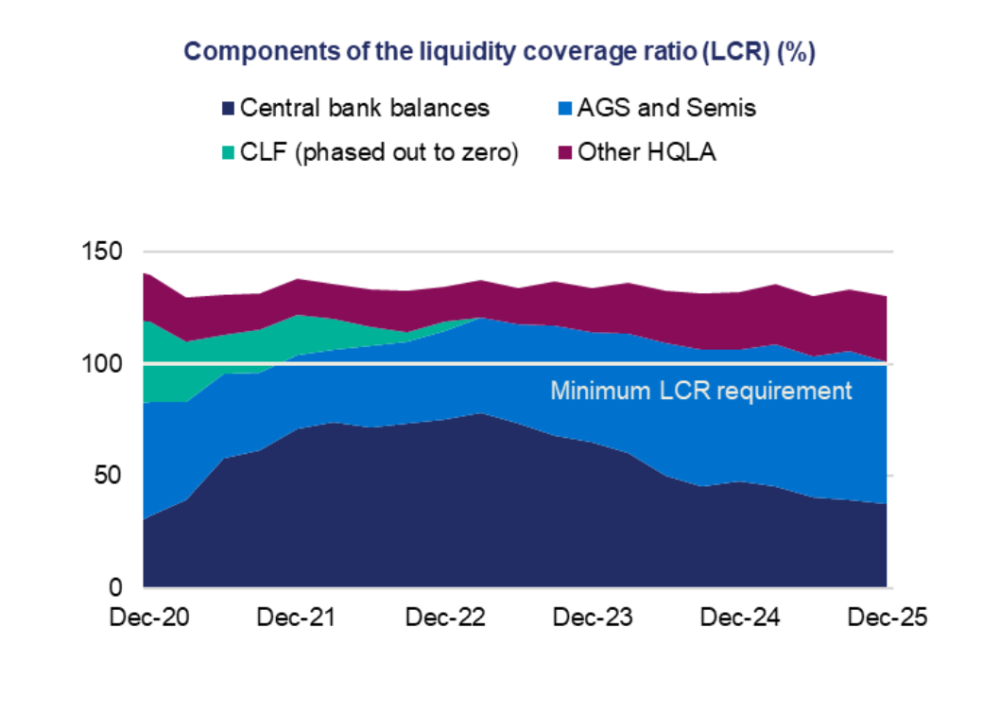

| Liquidity coverage ratio | 132.2% | 130.2% | -2.03 points |

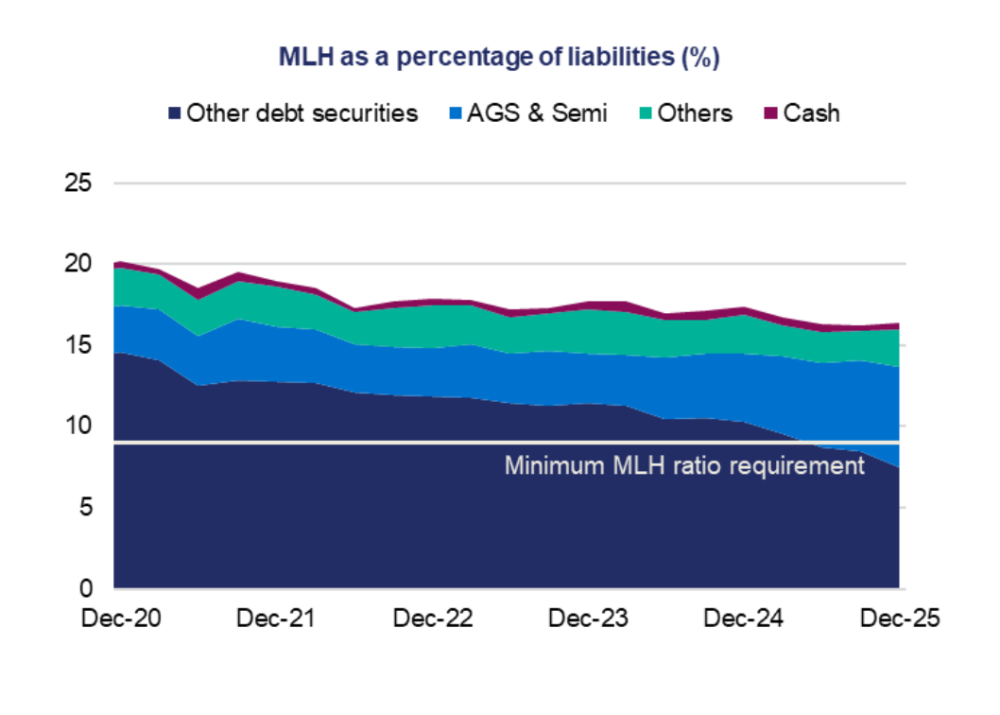

| Minimum liquidity holdings ratio | 17.4% | 16.4% | -0.97 points |

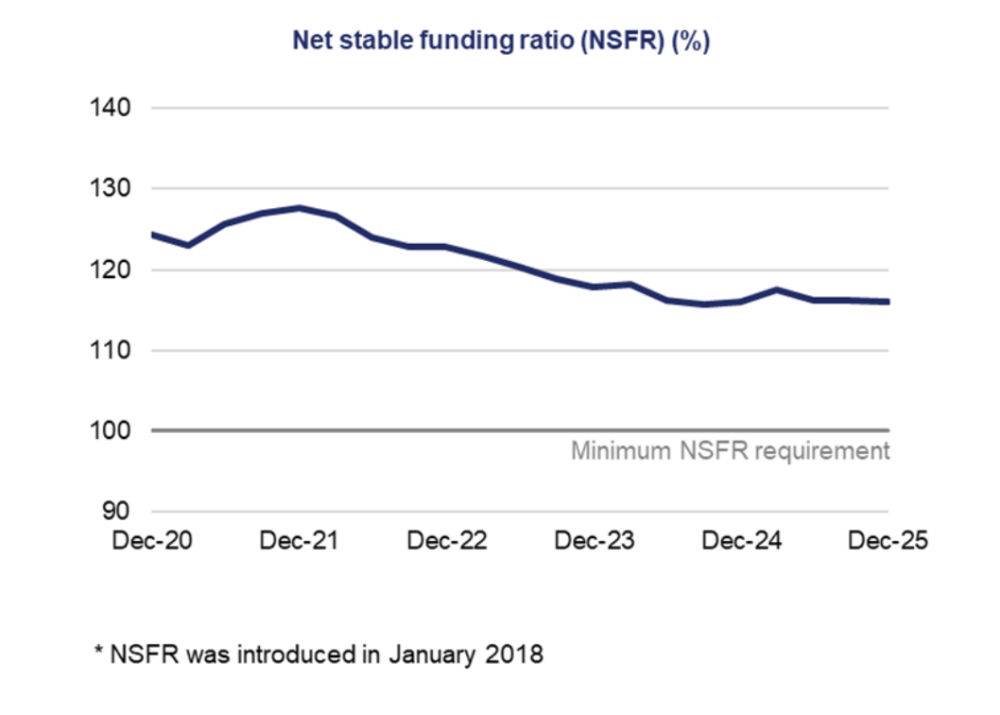

| Net stable funding ratio | 116.0% | 116.1% | 0.01 points |

Financial performance

Asset quality

Capital adequacy

Liquidity

Financial position