The Australian Prudential Regulation Authority (APRA) today announced proposed changes to the application of the capital adequacy framework for authorised deposit-taking institutions (ADIs) to support orderly resolution in the unlikely event of failure. The proposed changes are a significant step towards building APRA’s resolution capability. The discussion paper released today seeks feedback from interested stakeholders on the proposals.

The Australian Government’s 2014 Financial System Inquiry (FSI) recommended APRA implement a framework for loss-absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian ADIs and minimise taxpayer support (FSI Rec 3).

The Government supported this recommendation in its response to the FSI.

These proposals would ensure ADIs have adequate financial resources available to support orderly resolution in the highly unlikely event of failure. This will be achieved by adjusting, where appropriate, an ADI’s Total Capital requirement.

These proposals are distinct from APRA’s work on ensuring ADI capital levels are ‘unquestionably strong’, which relates to the ongoing resilience of institutions and is in response to a separate FSI recommendation (FSI Rec 1).

APRA is proposing an approach on loss-absorbing capacity that is simple, flexible and designed with the distinctive features of the Australian financial system in mind, and has been developed in collaboration with the other members of the Council of Financial Regulators. The key features of the proposals include:

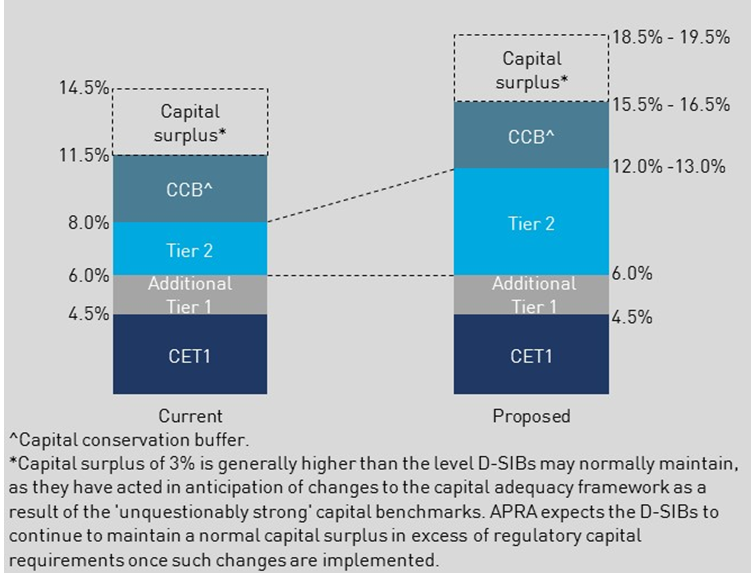

- for the four major banks – increasing Total Capital requirements by four to five percentage points of risk-weighted assets (see the illustrative example attached); and

- for other ADIs – likely no adjustment, although a small number may be required to maintain additional Total Capital depending on the outcome of resolution planning.

As ADIs will be able to use any form of capital to meet increased Total Capital requirements, APRA anticipates the bulk of additional capital raised will be in the form of Tier 2 capital. The proposed changes are expected to marginally increase each major bank’s cost of funding – incrementally over four years – by up to five basis points based on current pricing. This is not expected to have an immediate or material effect on lending rates.

APRA proposes that the increased requirements will take full effect from 2023, following relevant ADIs being notified of adjustments to Total Capital requirements from 2019.

In addition to the proposals outlined in this discussion paper, APRA intends to consult on a framework for recovery and resolution in 2019, which will include further details on resolution planning.

APRA Chairman Wayne Byres said one of APRA’s core functions as Australia’s prudential regulator is to plan for and, if required, execute the orderly resolution of the financial institutions it regulates.

“The resilience of the Australian banking system continues to improve, underpinned by the build-up of capital over the last decade.

“However, no matter how resilient financial institutions are, the possibility of failure cannot be entirely removed. Therefore, in addition to strengthening the resilience of the financial system, it is prudent to plan for the unlikely event

of failure.

“The events of the global financial crisis demonstrated the impact that failures can have on the broader financial system and the subsequent social and economic consequences.

“The aim of these proposals and resolution planning more broadly is to ensure that the failure of a financial institution can be resolved in an orderly fashion, which protects the interests of beneficiaries and minimises disruption to the financial system,” Mr Byres said.

Figure 1: Proposed change to the major banks' capital structures - as a percentage of RWA