Key metrics

Hospital treatment membership

General treatment membership

Hospital treatment episodes

General treatment services (ancillary)

Benefits (millions)

Out-of-pocket per episode/service

Membership and coverage

Hospital Treatment

At 31 March 2026, 12,790,111 people, or 45.8% of the population, were covered by hospital treatment cover. There was a slight increase compared to December 2025.

There was an increase in coverage of 101,918 insured people in the March 2026 quarter compared to December 2025. Family policies increased by 13,860 and single policies by 21,615 during the quarter.

The largest increase in coverage during the quarter was 11,771 for people aged between 40 and 44. The largest net increase (taking into account movement between age groups) was for the 0-4 with an increase of 26,315 people.

Net quarterly change in insured persons

Lifetime health cover

The majority of adults with hospital cover (87.0%) have a certified age of entry of 30, with no LHC loading.

At the end of the 31 March 2026 quarter, there were 1,187,740 people with a certified age of entry of more than 30 and subject to a Lifetime Health Cover loading; a net increase in people paying a penalty over the preceding 12 months of 85,524. There was a net increase in people with a certified age of entry of 30 (with no penalty) over the year of 99,722. Over the year, 88,245 people had their loading removed after paying a loading for ten years.

Number of persons insured by age

Hospital treatment tables

General Treatment

At 31 March 2026, 15,491,109 people or 55.5% of the population had some form of general treatment cover. There was an increase of 113,964 people when compared to the December quarter. There was an increase of General Treatment policies of 56,267 for March 2026 which was mainly driven by Single Policies which increased by 28,013. For the 12 months to 31 March 2026, the number of insured persons with general treatment cover has increased by 332,938.

The general treatment (ancillary) by age charts and data in this report show data for those people that have general treatment policies covering ancillary services, regardless of other treatment included in the product. This excludes those general treatment policies that do not cover ancillary treatment.

There was an increase of 92,465 people with general treatment (ancillary) coverage in the March 2026 quarter. The largest net increase in coverage, after accounting for movements across age groups, was 26,315 for people in the 0 to 4 age group.

Net quarterly change in insured persons (ancillary)

Number of persons insured by age (ancillary)

General treatment tables (ancillary)

Benefits Paid - Hospital treatment

Benefits per episode/service

| Hospital treatment | March 2026 | Change from December 2025 |

|---|---|---|

| Acute | $2,840 | -1.0% |

| Medical | $68 | -1.7% |

| Medical devices or human tissue products | $732 | 10.0% |

| Cardiac | $3,140 | 1.2% |

| Hip | $1,653 | -0.2% |

| Knee | $1,683 | 0.8% |

Total benefits and growth rate

| Hospital treatment | March 2026 | Change from December 2025 |

|---|---|---|

| Hospital | $4,749,761,741 | -11.4% |

| General | $1,876,830,842 | 3.5% |

During the March 2026 quarter, insurers paid $4,749.76 million in hospital treatment benefits, which was 11.37% lower compared to the December 2025 quarter. Hospital treatment benefits were comprised of:

- $3,465.03 million for hospital services such as accommodation and nursing

- $700.79 million for medical services

- $583.93 million for medical devices or human tissue items.

The age group for which most hospital benefits are paid is between 75 and 79 (top chart). Total benefits by age group is affected by the average benefits paid per person (displayed in the second chart) and the number of people in each age group.

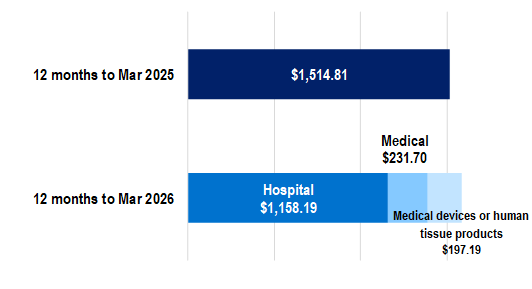

Average hospital benefits per person increased from $1,514.81 for the year ending March 2025 to $1,587.08 for the year ending March 2026. The largest amount of benefits per person was spent on hospital accommodation and medical, followed by medical services and then medical devices or human tissue benefits.

Hospital treatment benefits paid by age 12 months to 31 March 2026

Hospital treatment benefits per person covered and percentage of benefits paid by age cohort

Hospital treatment benefits per person

General treatment benefits

Benefits per service

| - | March 2026 | Change from December 2025 |

|---|---|---|

| Dental | $71 | 4.4% |

| Chiropractic | $37 | 9.4% |

| Physiotherapy | $44 | 6.8% |

| Optical | $87 | 3.8% |

During the March 2026 quarter, insurers paid $1,861.79 million in general treatment (ancillary) benefits. This was a decrease of 3.3% compared to the December 2025 quarter. Ancillary benefits for the March 2026 quarter included the major categories of:

- Dental $1,014.03 million

- Optical $285.48 million

- Physiotherapy $144.27 million

- Chiropractic $87.79 million.

There is a marked difference between the distribution of benefits over age groups between hospital benefits and ancillary benefits. The major difference is the higher claiming rate in older age groups for hospital benefits while benefits per person for ancillary benefits are more evenly spread over the age groups.

General treatment (ancillary) benefits per person during the year to March 2026 were $488.85 increased to $504.89 for the year to March 2025. The largest component of ancillary benefits is dental, for which $280.22 was paid per insured.

General treatment benefits paid by age 12 months to 31 March 2026 (ancillary)

General treatment benefits per person covered and percentage of benefits paid by age cohort (ancillary)

General treatment benefits per person (ancillary)

Medical treatment benefits

Medical benefits

Total benefits for medical services decrease by 8.3% during the March quarter 2026.

The change in medical benefits paid per service was calculated over a range of medical services and does not mean medical services overall decreased or increased in cost. The average benefits paid reflects the type of medical services utilised during the quarter as well as the volume of services. The medical service for which the greatest amount of benefits was paid was anaesthetics, comprising 25.1% of all medical benefits and totalling $176.09 million.

Medical benefits by Speciality group

Medical devices or human tissue benefits

Total benefits paid for medical devices or human tissue products decreased by 21.8% in March 2026 compared to December 2025. Similar to medical services, the change in benefits paid for medical devices or human tissue products was calculated over a range of medical devices or human tissue products (see chart) and does not mean medical devices or human tissue products overall changed in cost. The change in benefits paid may reflect a change in the type of medical devices or human tissue products utilised, or a change in the overall utilisation of medical devices or human tissue products. The medical devices or human tissue products group for which the greatest amount of benefits were paid was cardiac, comprising 18.1% of all medical devices or human tissue products benefits and totalling $95.44 million.

Benefits paid for medical devices or human tissue products

Service utilisation

Episodes/Services by type

| Episode/Service | March 2026 | Change from December 2025 |

|---|---|---|

| Hospital Episodes | 1,223,507 | -10.4% |

| Hospital Days | 3,037,295 | -8.3% |

| Medical Services | 10,248,137 | -6.9% |

| Medical devices and human tissue products | 797,526 | -21.5% |

| Specialist Orthopaedic | 147,939 | -20.9% |

| Ophthalmic | 88,582 | -23.8% |

| Spinal | 47,699 | -20.7% |

| General Treatment | 28,673,953 | 1.1% |

| Dental | 14,285,141 | -1.8% |

| Chiropractic | 2,363,426 | 17.3% |

| Physiotherapy | 3,244,982 | 14.6% |

| Optical | 3,287,199 | -15.9% |

During the March 2026 quarter, insurers paid benefits for 3.0 million days in hospital, arising from 1.2 million hospital episodes of care.

Hospital utilisation is distributed over four categories of hospital - public, private, day only facilities and hospital-substitute. During the March 2026 quarter, hospital episodes were distributed as follows:

- public hospitals 176,752 episodes

- private hospitals 815,968 episodes

- day hospital facilities 166,350 episodes

- hospital substitute 64,437 episodes.

For the March 2026 quarter, hospital utilisation (measured in episodes) decreased by 10.4% which was mainly driven by hospitals-substitute.

| - | Quarter change | Year change |

|---|---|---|

| Public hospitals | -4.9% | -0.1% |

| Private hospitals | -11.3% | +2.2% |

| Day hospital facilities | -10.1% | +0.5% |

| Hospital-substitute | -13.4% | +6.6% |

Day-only episodes in the four categories of hospital totalled 852,982 with a 11.5% change compared to December 2025.

Hospital treatment services per 1,000 insured persons

General treatment services (ancillary) per 1,000 insured persons

Out-of-pocket payments

Average out-of-pocket per episode/service

| - | March 2026` | Change from December 2025 | Change from March 2025 |

|---|---|---|---|

| Hospital treatment | $511.02 | 8.4% | 8.9% |

| Hospital-substitute treatment | $4.63 | 28.8% | 31.9% |

| General treatment ancillary | $65.02 | 3.4% | 5.5% |

| Medical gap where gap was paid | $245.08 | -11.6% | -9.5% |

The average out-of-pocket (gap) payment for a hospital episode was $511 in the March 2026 quarter. This included out-of-pocket payments for medical services, in addition to any excess or co-payment amounts relating to hospital accommodation.

The out-of-pocket payments for hospital episodes increased by 8.9% compared to the same quarter for the previous year.

Out-of-pocket payments for medical services were $245.08 where an out-of-pocket payment was payable. The amount of gap for medical services varies depending on the specialty group. The specialty group with the largest out-of-pocket payment was Orthopaedic with an average gap of $849.93. Gap incurred for the various medical services is displayed in the first chart. Medical gap also varies by state and territory and these differences are shown in the bottom chart.

Medical benefits and out-of-pocket by specialty group

Proportion of services and average out-of-pocket payments