Executive Summary

APRA’s mandate is to provide Australians with a safe and stable financial system. This objective is critical to the Australian community’s financial wellbeing and the growth of the Australian economy. A resilient financial system supports economic activity by providing credit, payment, investment and risk-transfer services to households and businesses, even if economic and financial conditions deteriorate.

Stress testing helps assess how shocks can spread, and the effects of both the shocks and entities’ responses. System-wide stress testing can reveal vulnerabilities and amplification mechanisms, including how shocks can transmit across industries, and can deepen understanding of financial system resilience.

System risks and interconnectedness

The Australian financial system has become more interconnected. Banks, superannuation funds, insurers, and financial markets are linked through funding relationships, asset holdings, market participation and shared service providers. These connections underpin efficiency and help build resilience in normal times, but they can also enable stress to transmit across institutions, sectors and markets when conditions deteriorate. In a more connected financial system, the behaviours of financial institutions are an important determinant of how shocks transmit, and can act to either amplify or absorb the initial shock. Decisions are often made with incomplete information, under rapidly changing conditions, and with limited visibility of how other entities and markets will respond.

The external environment has also become increasingly uncertain and globally interconnected, with shocks arising from geopolitical developments, cyber threats, demographic trends and threats to public health. These shocks can have negative impacts on the Australian economy and financial system, including reduced economic activity, financial market dislocation and operational disruptions, and can involve multiple sources of stress occurring simultaneously.

Growing role of superannuation in the Australian financial system

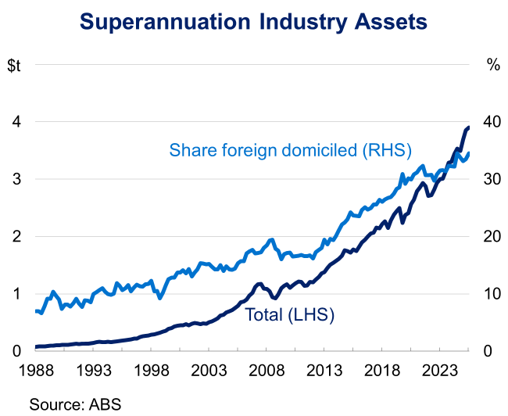

The superannuation industry is increasing in systemic importance due to its growing scale, interconnection, and influence on household wealth and real‑economy outcomes. Assets in APRA-regulated superannuation funds grew from $1.3 trillion in 2015 to $3.2 trillion by the end of 2025. Superannuation now accounts for almost half of the financial assets of households in Australia. By 2060, some forecasts suggest assets managed in the superannuation system could reach almost 250 per cent of GDP. 1The superannuation system is also in the process of changing from one dominated by accumulation accounts, in which members cannot usually access their money, to one with a higher share in the retirement phase, in which superannuation has a heightened influence on household expenditure and financial decisions.

As it has grown, the superannuation sector’s importance to the rest of the financial system, particularly banks, has also grown. Superannuation funds hold around 40 per cent of banks’ domestic short-term debt, and a similar share of their equity.2 There are also very important operational linkages, with superannuation funds relying on banks for payments, foreign exchange, and custodial services. Superannuation also has deep connections with insurers through the insurance benefits provided to members.

The System Risk Stress Test

The System Risk Stress Test (SRST) was the first stress test undertaken by APRA that involved multiple regulated industries, with participation from the four major banks and six large superannuation funds. It explored how a shock could affect the Australian financial system, with a specific focus on linkages between superannuation funds and banks, and on how the growing superannuation industry could amplify or dampen system risk.

The SRST instructed participants to model a severe stress scenario. For banks, this included liquidity pressures exceeding any experienced by large Australian banks over the past 50 years. The stress applied to superannuation funds was similarly severe, with member withdrawals and switching significantly surpassing levels observed during COVID‑19 or other previous periods of financial market stress. Further, the scenario incorporated an additional disruption at a material service provider, consistent with a more complex external environment.

As with other APRA stress tests, the SRST scenarios are not forecasts or predictions. They are severe but plausible hypothetical scenarios used to test financial system resilience.

The insights from the SRST can inform APRA’s supervision and policy priorities. They also help APRA and the broader Council of Financial Regulators to continue to build resilience in the financial system and respond to negative shocks more effectively. APRA’s stress tests are also aimed at encouraging entities to uplift their own capabilities and broaden the range of risks they are prepared for.

This Information Paper sets out the key conclusions and findings from the exercise undertaken in 2025 and early 2026.

Key Findings

Finding 1

The SRST showed the resilience of the Australian financial system to market and liquidity shocks, and the features which underpin it.

All participating banks and superannuation funds were able to withstand the shock resulting from the severe SRST scenario.

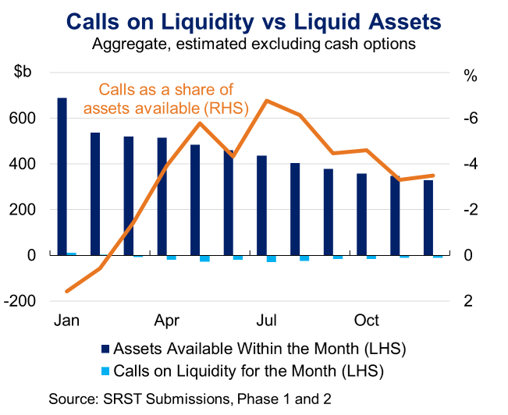

This resilience was underpinned by strong and usable bank liquidity buffers, banks' access to central bank facilities, and superannuation funds’ ability to access liquidity in deep international markets.

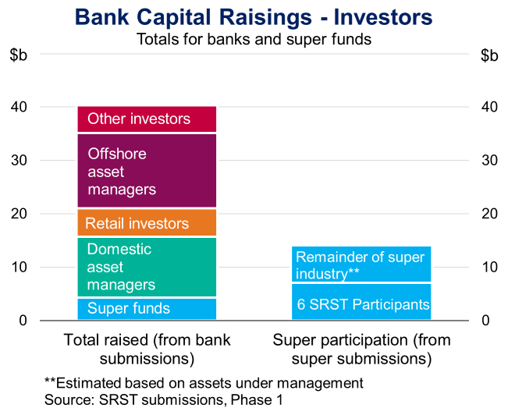

The SRST also reinforced the central role that the superannuation sector can play as a stabilising feature of the Australian financial system. Super funds were able, and willing, to provide new equity capital for the banking system, during a severe economic and financial downturn, despite being under significant stress themselves.

Response

The findings reinforce the value of strong capital, liquidity and prudential safeguards in helping the financial system absorb shocks and continue to provide critical services to households and businesses in stress. APRA will continue to apply a system-wide lens to assessing financial stability, including when setting prudential requirements.

Finding 2

The SRST highlighted system vulnerabilities, such as those related to concentration, mismatched assumptions and common dependencies, that could amplify stress events.

The interconnected nature of the Australian financial system can be a stabilising force, but in periods of severe stress these linkages can also create vulnerabilities.

Banks rely on funding from superannuation funds, and some large banks source more of their funding from this sector than others. This creates funding concentration risk for banks, and the potential for stress events to be more severe for some entities.

In addition to this concentration, participants in the SRST had different views on the likely stability, in a crisis situation, of the funding that superannuation funds provide to banks. This is the case for both short-term wholesale funding and deposits. Different expectations about how funding would hold up in a crisis could make stress harder to manage.

The exercise also highlighted risks inherent in shared material service providers. If a material service provider is disrupted, it could limit how quickly entities can undertake liquidity and risk‑management actions and therefore amplify stress. For superannuation funds, reliance on external managers may limit visibility of underlying positions.

These vulnerabilities increase the potential for shocks like those examined in the SRST to have market and economy‑wide effects. Bank responses to the SRST shocks included reducing credit availability in some segments, alongside a contraction in market lending activity that would transmit stress to other market participants.

Response

This exercise underlines how APRA’s prudential frameworks for liquidity risk management and operational risk management lay the foundation for a stable financial system. Findings from the SRST will inform proposed amendments to bank liquidity rules that will be released for consultation during 2026, and APRA’s core supervisory activities for banks and superannuation funds. The SRST findings also reinforce APRA’s continued focus on the importance of entities managing material service provider arrangements through enterprise operational risk management.

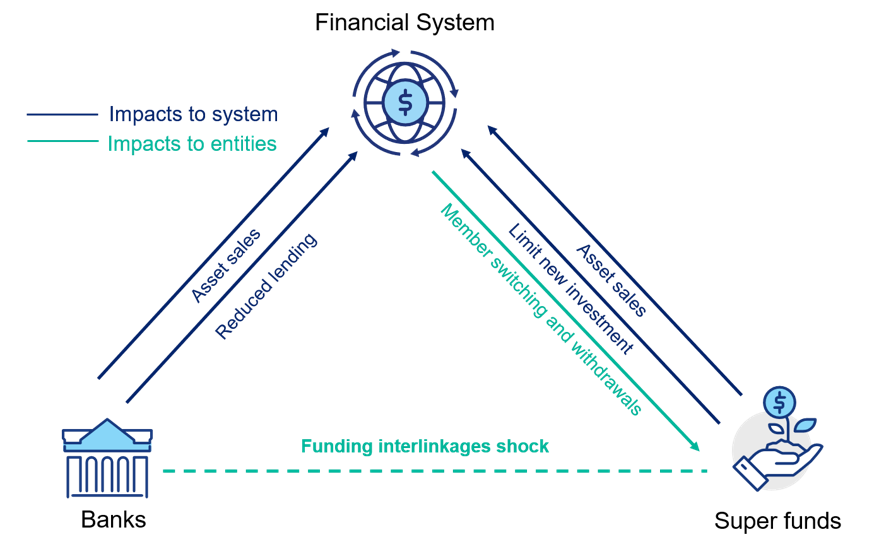

Figure 1 – Financial system risk transmissions in stress

Finding 3

Superannuation funds can play a systemic role in the stability of the Australian financial system. How they respond in a stress event can materially affect banks, financial markets and superannuation fund members.

In the SRST scenario, superannuation funds’ withdrawal of funding was a contributor to the idiosyncratic liquidity stress that each participating bank modelled. However, in the subsequent broader downturn and solvency stress, superannuation funds’ willingness to provide equity capital to banks illustrated their ability to dampen risk.

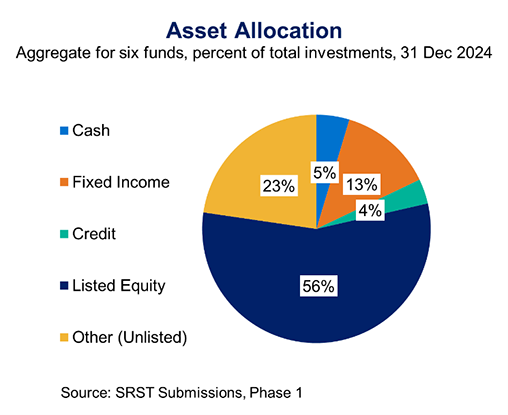

Superannuation funds also provide significant funding across the wider financial system, including to private markets. Some superannuation funds indicated that they may scale back capital injections into existing investments or limit new commitments in some unlisted markets in response to the SRST shock, which could put pressure on those markets.

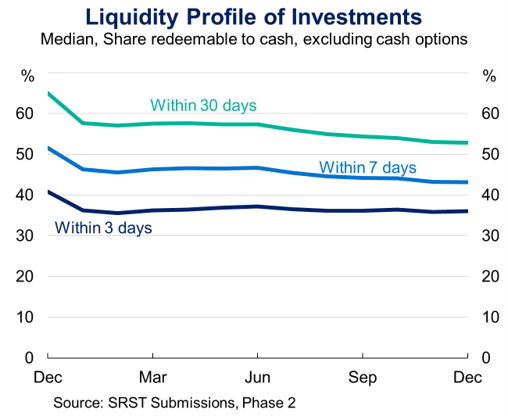

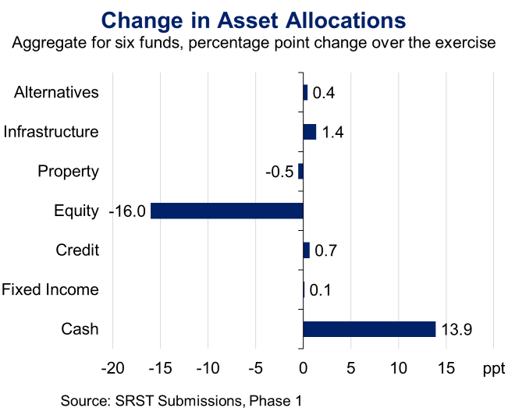

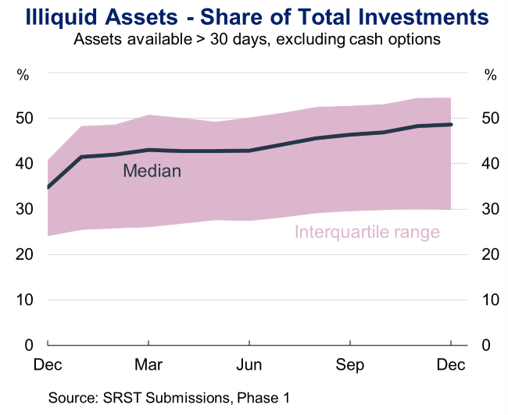

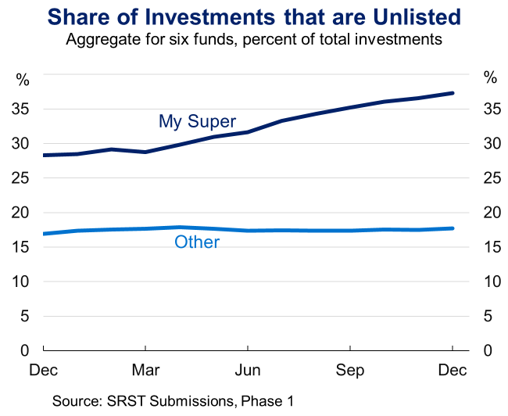

To respond to liquidity stress and raise cash in the exercise, superannuation funds primarily sold listed equities and avoided selling unlisted assets. This response helped them meet short-term needs, but it also left some members – especially members in MySuper options – more exposed to risks tied to unlisted assets, such as liquidity, valuation and sequencing risks.

Response

These findings highlight the importance of strong investment governance, sound liquidity risk management and robust valuation practices by superannuation funds, as publicly communicated by APRA. They also reinforce the need for a continued uplift of practices across the industry, including considering how their actions in stress affect both the financial system and member outcomes.

Finding 4

Some vulnerabilities in the system are likely to increase as the superannuation sector continues to grow and mature.

Superannuation is a large and growing component of the Australian financial system. Decisions by a small number of large funds could have very consequential effects across the system. As more members move into retirement, meeting pension payments and possible member withdrawals from the superannuation system will increase demands on funds’ liquidity and response capabilities.

Moving forward, superannuation funds may need to invest more overseas due to size limitations in domestic markets. Over time, this will increase exposure to currency risk. Managing that risk may become more challenging if existing hedging providers, such as domestic banks, are unable to offset these exposures, leading to greater use of margining to manage these risks.

Response

APRA will continue to focus on how these risks are changing as the superannuation system matures. This includes the risk implications as more members move into the retirement phase, and the evolution of foreign exchange risks with growing overseas investments.

Finding 5

Better entity preparedness for stress events will make the financial system stronger.

The SRST highlighted that stress testing capabilities of superannuation funds need to develop to be commensurate with the sector’s systemic footprint. The growing importance of the superannuation system to the rest of the financial system, and to the wealth of Australians, highlight the importance of these capabilities. The exercise also highlighted areas where banks – who have more experience with stress testing – can further uplift their capabilities.

The SRST also showed a range of expectations across banks and superannuation funds regarding the role of public sector response in severe stress. Public action can help stabilise the system in a crisis, but entities need to be ready to respond on their own rather than overly relying on government intervention.

The exercise illustrated the importance of testing a wider range of shocks, including entity-specific events, and situations that fall outside a standard economic downturn. It also reinforced the need for stress testing that incorporates uncertainty around the behaviour of other market participants and the feasibility of management actions during periods of market disruption. Finally, it showed the benefit of looking at how banks and superannuation funds interact and focusing on impacts to the financial system, rather than assessing entities in isolation.

Response

APRA will continue to undertake exploratory and system stress tests across banks, superannuation funds, and other regulated entities. It expects regulated entities – particularly superannuation funds – to continue to develop their stress testing capabilities and crisis preparedness.

Scenario Design

The Scenario

The SRST applied a common scenario to both banks and superannuation funds. The scenario was intentionally designed to separate the timing of liquidity stress for the two industries, allowing APRA to observe how stresses might transmit between sectors. The exercise applied APRA‑specified scenario shocks and examined participants’ behavioural responses and financial outcomes. The shocks and responses are displayed in Figure 1 below, across both banking and superannuation industries.

Figure 2 – Design of the System Risk Stress Test

Participating entities made two sets of submissions. The first phase explored entities’ assumptions and responses to the scenario, while the second phase tested the robustness of those findings through greater standardisation and additional analysis.

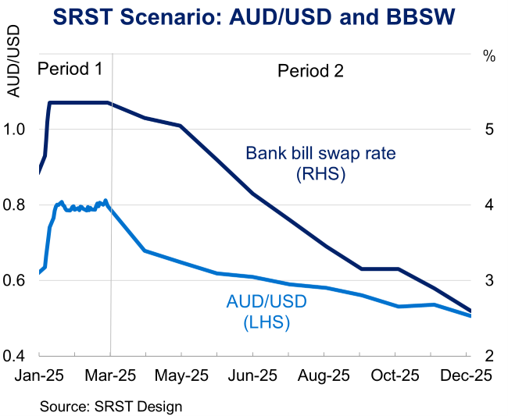

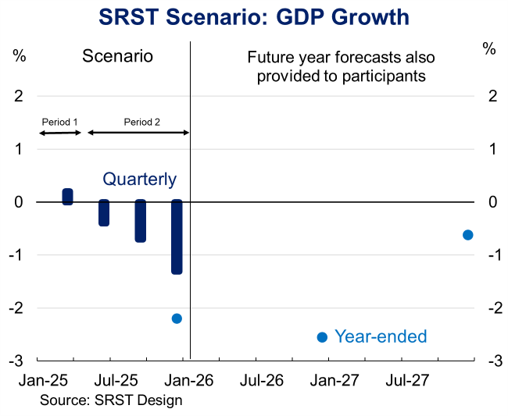

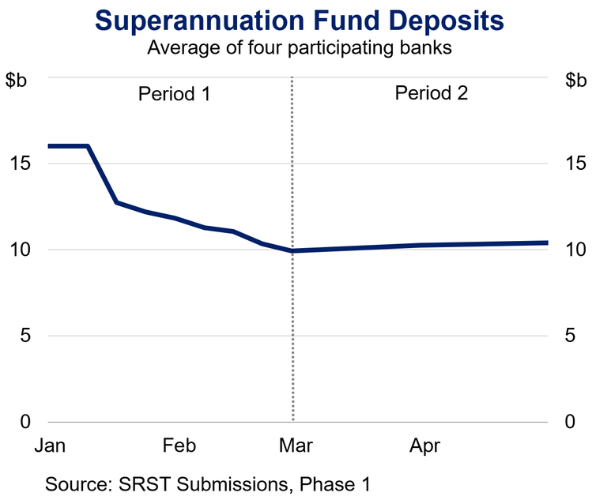

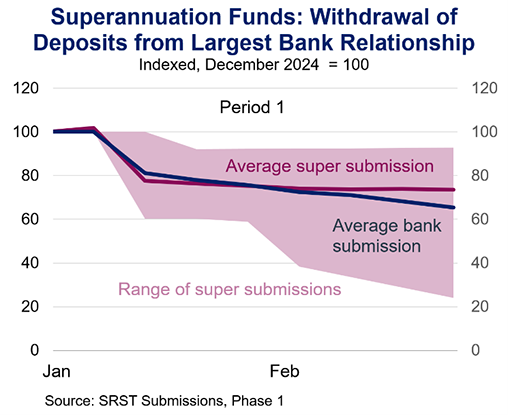

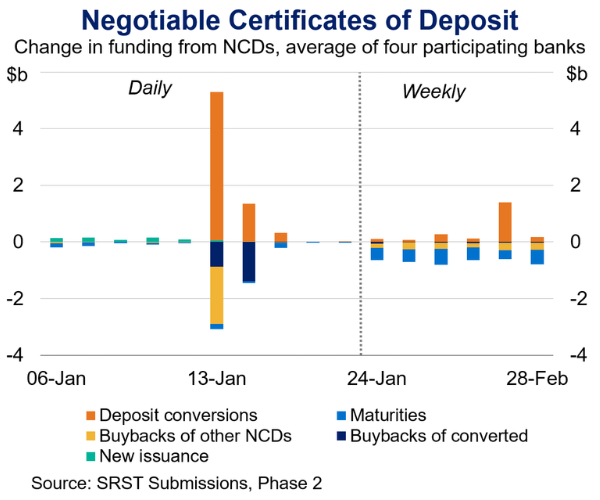

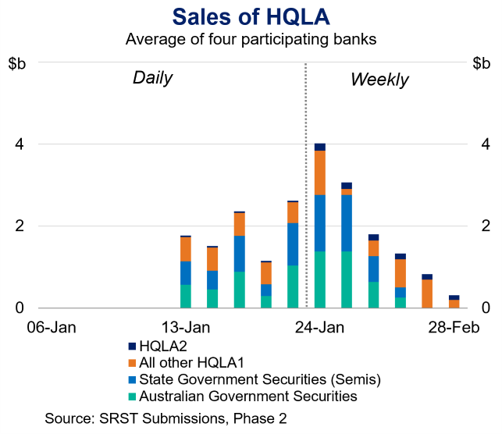

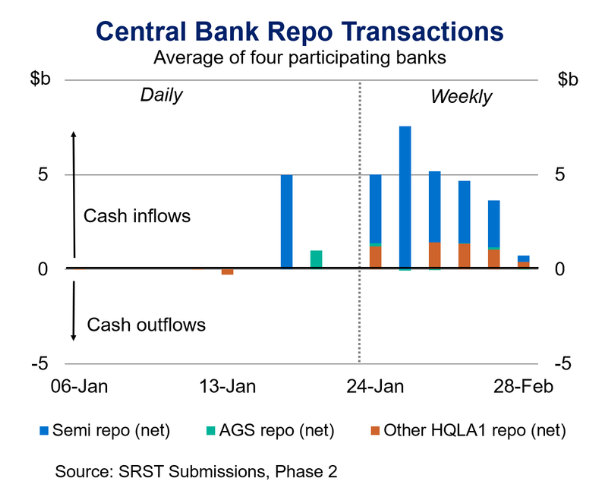

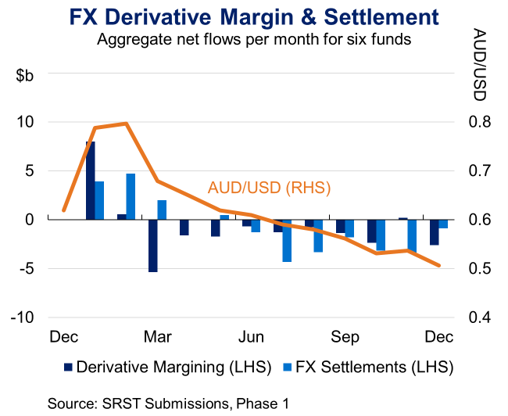

In Period 1 of the exercise, the primary focus was on the liquidity of banks. The Australian economy was assumed to be relatively strong, supported by an improvement in the outlook for a major trading partner. This was accompanied by a sharp appreciation of the Australian dollar. As banks provide foreign‑exchange hedging to other counterparties, the appreciation generated collateral flows from banks to their counterparties, reducing bank liquidity. Early in this period, each participating bank was instructed to assume they alone were each subject to an idiosyncratic funding run, affecting both wholesale and deposit funding from institutional and corporate clients, including superannuation funds. Consistent with this assumption, superannuation fund participants were instructed to model the rapid termination of their largest banking relationship across deposits and wholesale debt exposures.

These conditions persisted for around two months. During this period, banks were required to manage severe liquidity pressure, relying on their existing stock of liquid assets and access to official liquidity facilities, in line with the scenario instructions. While broader liquidity stress was assumed to continue across the banking sector, large funding outflows were assumed to stabilise from around the start of month three.

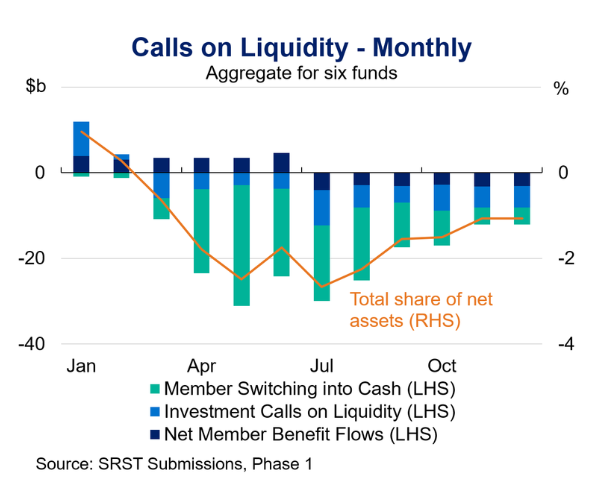

In Period 2 of the exercise (from approximately month four onwards), the primary focus was on the liquidity of superannuation funds. The macroeconomic outlook deteriorated significantly. The Australian dollar depreciated, which shifted the movement of collateral flows from superannuation funds to other counterparties, generating stress for superannuation funds. Superannuation funds experienced increased member switching into cash and lower‑risk investment options, alongside declining contributions and rollovers as economic conditions worsened. Liquidity conditions in private and unlisted markets deteriorated markedly, constraining funds’ investment flexibility. As the downturn progressed, member withdrawals increased, particularly among members above preservation age, and market liquidity remained subdued. Superannuation funds had to manage their liquidity and asset allocation in order to respond to these shocks.

By late in the scenario, the cumulative impact of economic weakness, market stress and funding constraints led to the expectation that banks would need to raise significant new equity to restore capital positions, culminating in large capital raisings toward the end of the scenario horizon. Superannuation funds had to model the extent of their participation in these capital raisings.