Key statistics

Excludes ADIs that are not banks, building societies or credit unions. See ‘Explanatory Notes’ of the Quarterly authorised deposit-taking institution property exposures statistics (excel file) for details of share calculations.

Key residential mortgage lending statistics for ADIs for the quarter were:

| ADIs' residential property exposures | March 2025 | March 2026 | Year-on-year change |

|---|---|---|---|

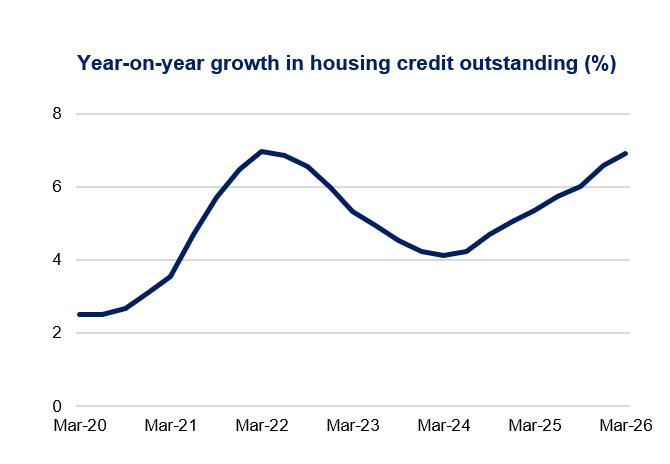

| Total credit outstanding ($bn) | 2,349.7 | 2,512.7 | 6.9% |

| Owner-occupied loans – share | 67.6% | 67.0% | -0.69 points |

| Investment loans – share | 30.4% | 31.0% | 0.61 points |

| Loans with LVR ≥ 80% – share | 17.0% | 16.7% | -0.34 points |

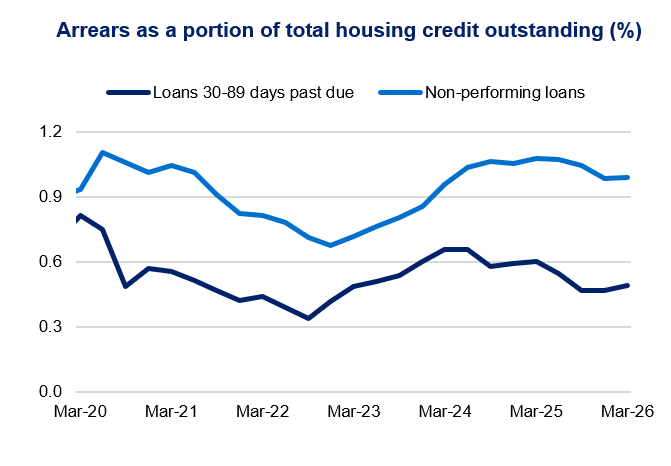

| Loans 30–89 days past due – share | 0.60% | 0.49% | -0.11 points |

| Non-performing loans | 1.08% | 0.99% | -0.09 points |

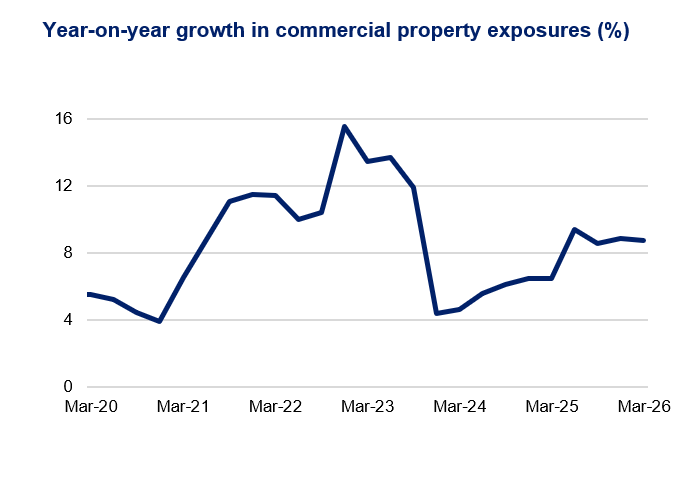

Key commercial property statistics for ADIs for the quarter were:

| ADIs’ new loans funded during the quarter | March 2025 | March 2026 | Year-on-year change |

|---|---|---|---|

| New loans funded ($bn) | 154.7 | 182.1 | 17.7% |

| New owner-occupied loans funded – share | 64.3% | 62.4% | -1.9 points |

| New investment loans funded – share | 33.5% | 35.0% | 1.51 points |

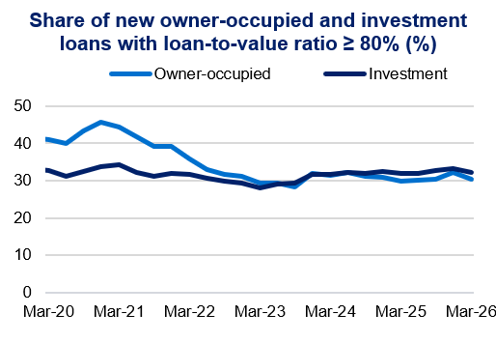

| New loans with LVR ≥ 80% – share | 30.3% | 30.7% | 0.38 points |

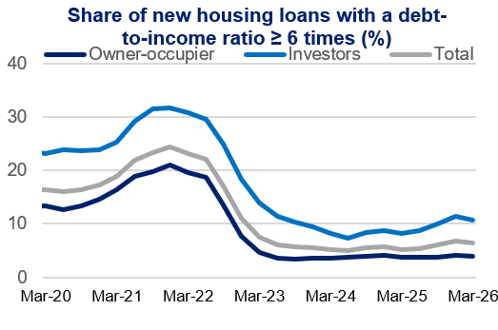

| New loans with DTI ≥ 6x – share | 5.3% | 6.4% | 1.12 points |

| New owner-occupied loans with DTI ≥ 6x – share | 3.7% | 3.9% | 0.19 points |

| New investment loans with DTI ≥ 6x – share | 8.2% | 10.8% | 2.56 points |

| ADIs’ commercial property exposures | March 2025 | March 2026 | Year-on-year change |

|---|---|---|---|

| Commercial property exposure limits ($bn) | 483.7 | 525.8 | 8.7% |

| Commercial property exposures ($bn) | 448.4 | 487.6 | 8.7% |

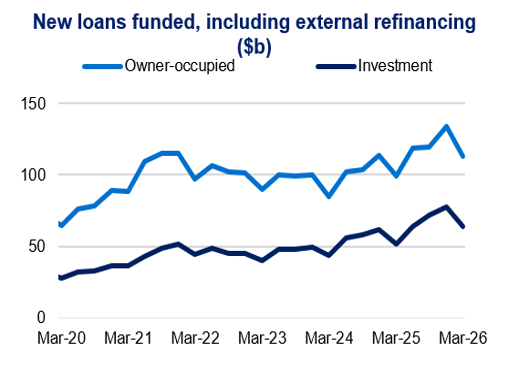

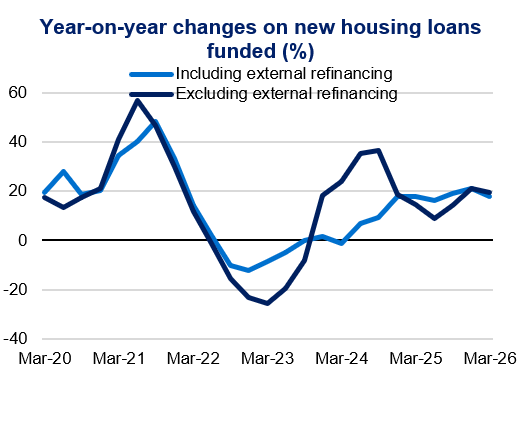

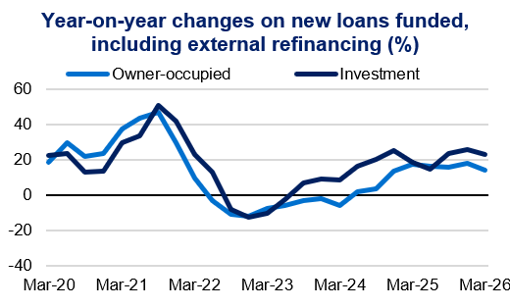

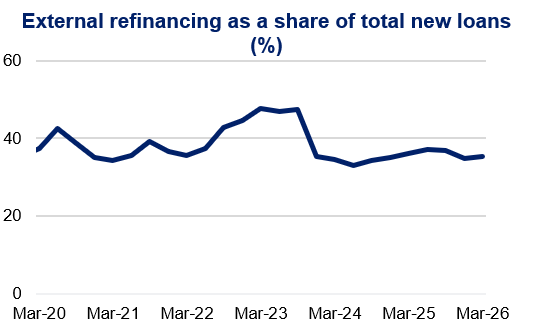

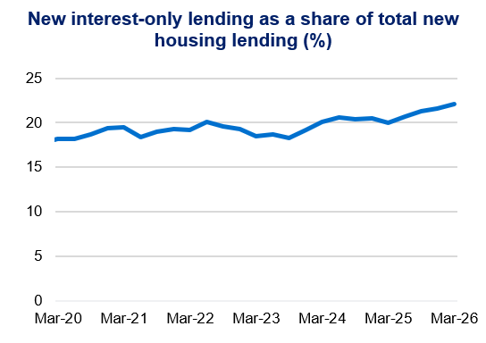

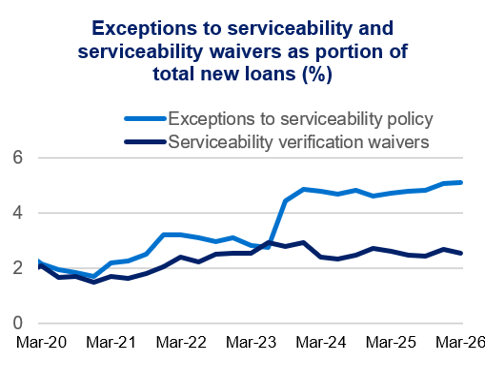

Residential mortgages: new lending

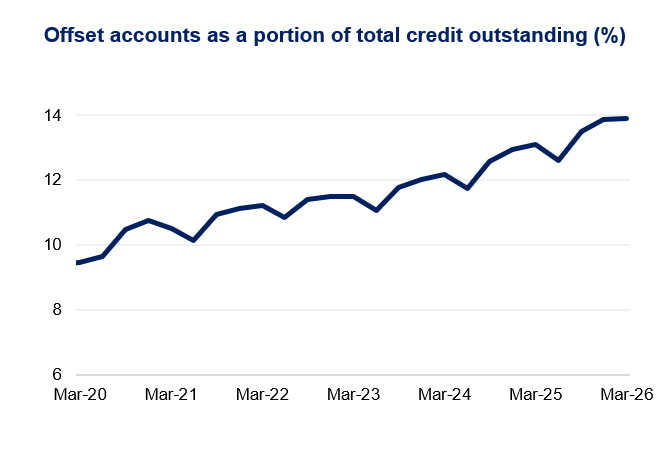

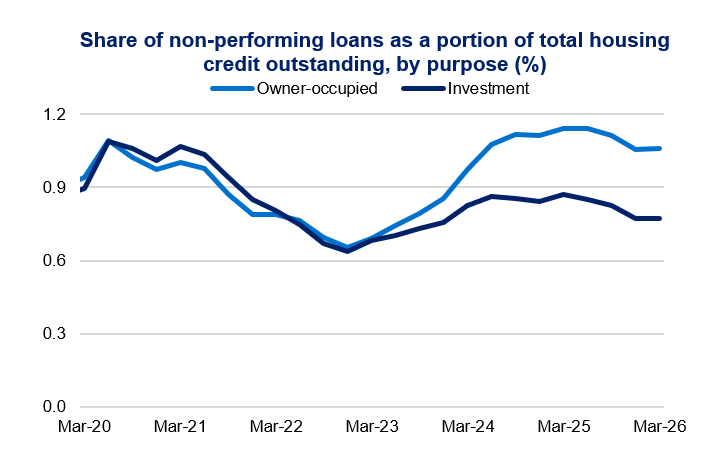

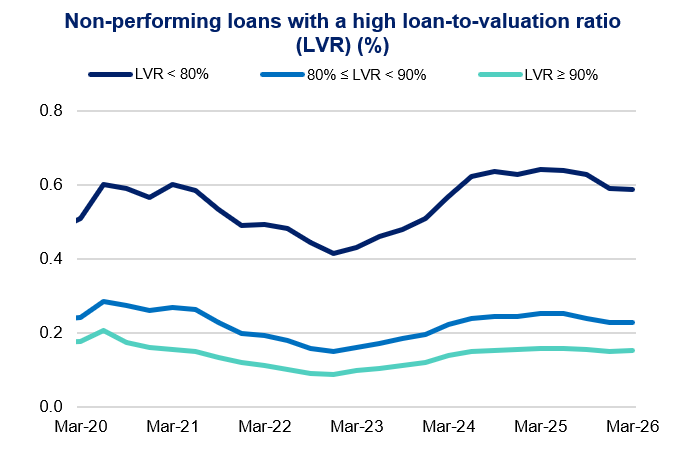

Residential mortgages: outstanding credit

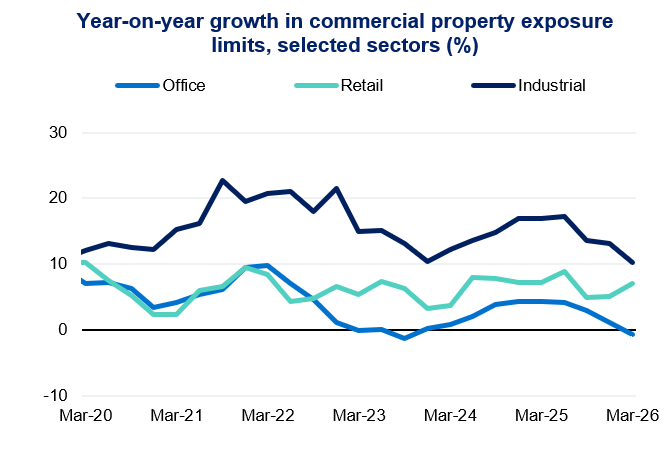

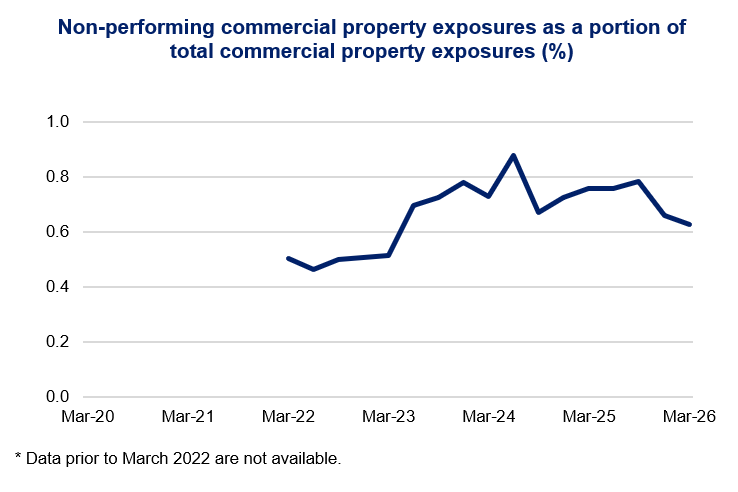

Commercial real estate